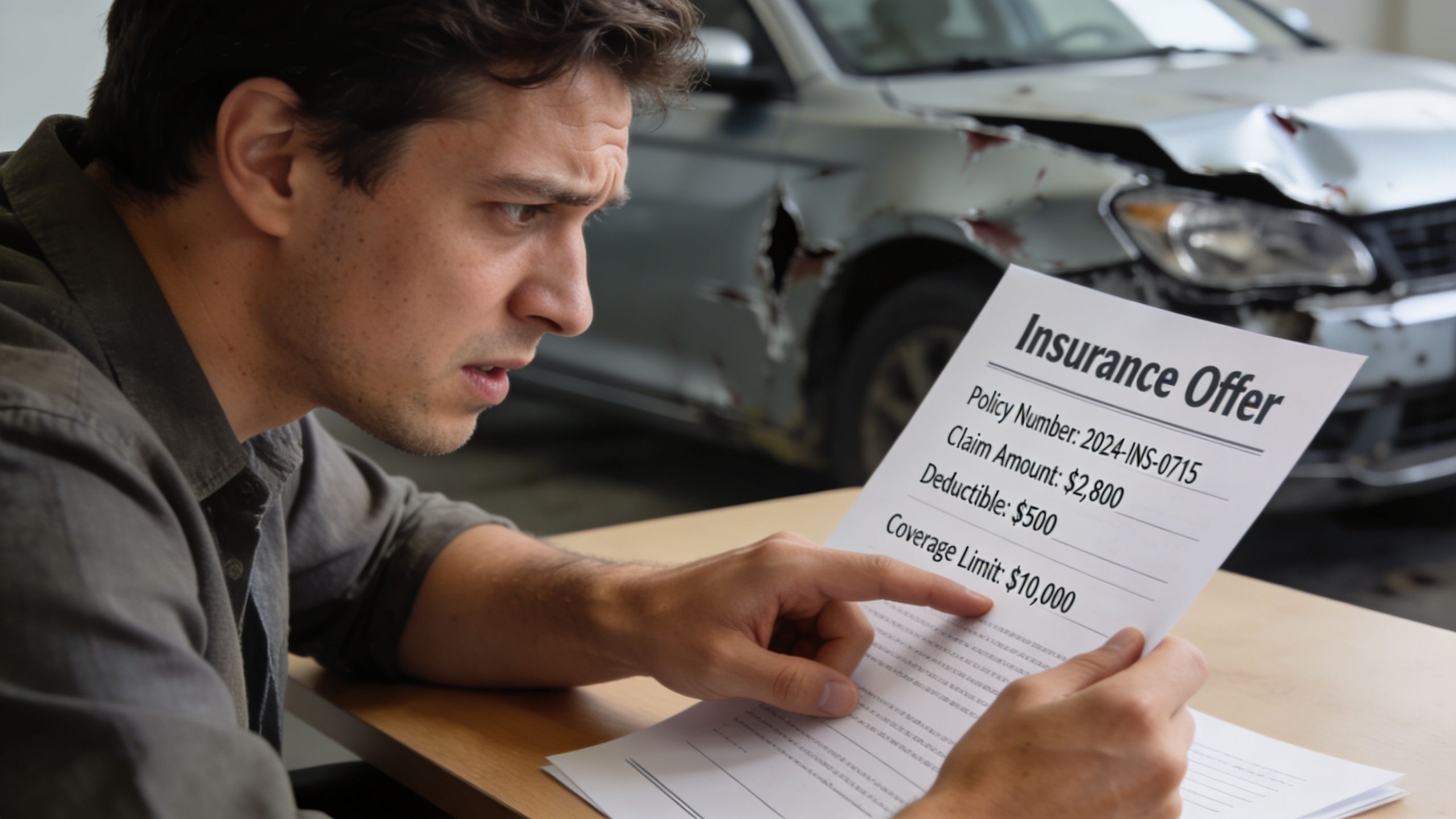

You open the insurer's valuation and the number feels detached from reality. The car was clean, well maintained, properly optioned, and local listings don't look anything like what the carrier is offering. If it's a total loss claim, the settlement may not buy a comparable replacement. If it's a diminished value claim, the offer may act like the accident barely changed the car's market appeal.

That's the point where many vehicle owners get talked into accepting less than they should. The carrier has a process, software, adjusters, and canned language. You have your vehicle, your records, and a strong sense that the number is wrong. An appraiser expert witness helps close that gap by turning your objection into a documented, defensible valuation.

For auto claims, this role matters most when the dispute isn't just about opinion. It's about whether the value can be proven.

Your Guide to Challenging a Lowball Insurance Offer

A common version of this problem looks like this. A driver gets rear-ended, the other carrier accepts liability, repairs are completed, and then the diminished value offer arrives. It's low enough that the owner immediately knows something is off, but the adjuster says the number came from their system and is “what the market supports.”

Or the vehicle is declared a total loss. The insurer sends a valuation packet with comparables from outside the owner's real market, uneven condition assumptions, or option lines that don't match the actual vehicle. The owner pushes back and gets the same answer in different words.

That's where the fight usually changes. A general complaint won't move much. A documented valuation often will. If the claim has started sliding toward formal dispute territory, it also helps to understand the broader claims process, including resources on appealing a Kentucky insurance claim, because many of the same practical issues show up across states: delay, under-valuation, and pressure to settle before the owner has proper support.

What changes when you bring in an expert

An appraiser expert witness is not there to create a bigger number for the sake of it. The job is to create a supportable number using market evidence, clear methodology, and documentation that can hold up if the dispute moves into appraisal, deposition, or court.

Practical rule: If an insurer's number can't be explained in plain language, challenged line by line, and tested against real market data, you shouldn't treat it as the final word.

For many policyholders, the first useful move is learning whether the policy gives you a formal path to dispute value through the insurance appraisal clause process. That process can lessen the influence of insurer-driven valuation systems and force the discussion back onto evidence.

What works and what doesn't

What works:

- Vehicle-specific evidence: Service records, photos, option details, mileage, prior condition, and local market examples.

- Independent analysis: A report built outside the insurer's software ecosystem.

- Clear escalation: A formal dispute path instead of repeated phone calls with no paper trail.

What doesn't:

- Saying the offer feels unfair: That may be true, but it won't carry the dispute.

- Sending random listings: Comparables only help when someone explains why they are relevant.

- Waiting too long: Delay usually makes records harder to gather and weakens your position.

What Is an Appraiser Expert Witness

A standard appraiser can give you a value opinion. An appraiser expert witness gives you a value opinion that is built to survive challenge.

That distinction matters. In auto claims, especially diminished value and total loss disputes, the issue usually isn't whether someone can produce a number. The issue is whether that number can be defended when the insurer, opposing counsel, or another appraiser starts testing every assumption behind it.

Calculator versus professor

The simplest analogy is this: a standard appraiser is like a calculator. You get an answer.

An expert witness is the professor at the board who can show every step, explain why the formula fits the problem, respond when someone says the inputs are wrong, and stay calm while doing it.

That's why the role is bigger than valuation alone. In litigation guidance for appraisal experts, the expert is expected to do more than estimate value. They must prepare a defensible report and, if needed, provide sworn testimony. They're evaluated on whether they can explain complex methods clearly, stay unbiased, and document methodology and data sources. Federal Rule 26 also requires expert disclosures to include a complete statement of opinions, the basis and reasoning, the data considered, qualifications, recent testimony, and compensation details, as outlined in this litigation guidance on appraisal review and expert testimony.

Why legal standards matter to a car owner

You don't need to become a lawyer to benefit from those rules. You just need to understand what they do for you. They force the expert's opinion to be transparent.

If you're trying to sort out the basic valuation side before the legal side, it helps to understand what a car appraisal is. But for a disputed claim, the bar is higher. The appraiser's work has to be organized so another side can inspect it.

A good report doesn't hide the judgment calls. It identifies them and supports them.

That's also why broad legal education around how attorneys leverage expert witnesses for personal injury cases can be useful context. The legal system relies on specialists when decision-makers need help understanding technical facts. In an auto valuation dispute, your appraiser expert witness is there to explain market reality in a form that can be used.

The difference clients should care about

When hiring for a disputed auto claim, ask a practical question: can this person defend the valuation if challenged?

If the answer is no, you may be paying for a number without paying for protection.

Anatomy of a Lawsuit-Ready Appraisal Report

A strong report doesn't read like a price guess dressed up in formal language. It reads like a file that was built for scrutiny.

In auto claims, that means every important conclusion should trace back to something visible: the vehicle itself, the market, the valuation date, the comparables, the adjustments, and the reasoning that ties them together.

What the report must establish

The report should first lock down the subject vehicle. That includes pre-loss condition, mileage, trim, options, prior damage history if relevant, and the market area that fits the claim.

Then it needs a valuation method that makes sense for the dispute. In vehicle claims, that often means a sales comparison analysis supported by real comparable vehicles and clear adjustment logic. If the claim involves post-repair stigma or market resistance after an accident, the report should connect the damage history to market impact instead of treating diminished value like an abstract formula.

The most important point is methodological discipline. A litigation-support outline on appraisal review states that a litigation-ready report is a defensible workflow. Experts must verify pre-loss condition, mileage, options, and market data, then justify why selected comparables are more valid than others. Courts scrutinize the method, not just the final number, for bias and reproducibility, as described in this appraisal report analysis outline.

The pieces that carry weight

A lawsuit-ready auto appraisal report usually needs these elements:

- Vehicle identification and inspection basis: What was inspected, when, and through what records or physical review.

- Valuation date: The report has to anchor value to the correct date, not a vague time period.

- Comparable selection logic: Why each comp belongs in the analysis and why weaker comps were excluded.

- Adjustments that can be explained: Mileage, condition, trim, options, prior damage, and market differences should be reasoned out, not dropped in unexplained.

- Source documentation: Listings, market records, photos, repair materials, and other supporting items should be identifiable.

- Certification and signature: The appraiser should stand behind the report in writing.

For readers who want to see what that kind of work product looks like in practice, a diminished value report example helps show how evidence and reasoning are assembled into a claim-ready document.

What weak reports get wrong

Weak reports often fail in ordinary ways. They rely on mismatched comparables. They skip explanation on condition adjustments. They lean too hard on generic software outputs. They assume local market behavior without proving it.

The number is the conclusion. The report is the proof.

That distinction becomes obvious once testimony starts. This overview gives a useful visual sense of how valuation disputes get examined under pressure:

The Expert Witness in Action Deposition and Trial

Most clients worry about the courtroom before they understand the process. In practice, the first pressure test is often the deposition.

A deposition is a formal question-and-answer session taken under oath, usually outside the courtroom. The opposing attorney asks the appraiser about the report, the data, the comparables, the adjustments, and any assumptions that could be attacked. The vehicle owner usually doesn't need to carry that technical burden. That's the expert's job.

What deposition looks like in a vehicle valuation dispute

A capable appraiser expert witness enters the deposition knowing where the weak points will be targeted. On a total loss claim, counsel may ask why a certain comparable was included, why another was excluded, or whether the market area was too narrow or too broad. On diminished value, they may press on whether the accident history changed marketability or whether the reduction claimed is overstated.

The goal isn't to sound clever. The goal is to stay precise. If the report is sound, the testimony should follow the same path as the written analysis.

Opposing counsel usually isn't looking for one dramatic mistake. They're looking for a chain of small weaknesses they can turn into doubt.

That's why preparation matters so much in thin-comp markets. A practice note on expert witness work points out that a key part of the job is anticipating challenges from the opposing side's own valuation expert and being ready to critique the opposition's appraisal for bias or methodological weakness, especially with classic or modified vehicles, as noted in this expert witness service overview.

What trial changes

Trial is different. The audience is no longer just attorneys building a record. It may be a judge, a jury, or an arbitrator who doesn't live in the valuation world.

The expert's task becomes educational. They have to explain why the vehicle's real market value differs from the insurer's number without drowning the decision-maker in jargon. That means translating valuation work into plain English. Why this comp? Why this adjustment? Why does prior damage matter here but not there? Why does a collector or modified vehicle require special care when the local market is thin?

The strongest testimony is usually simple, organized, and restrained. An expert who acts like an advocate often loses credibility. An expert who explains the method and lets the analysis carry the point usually helps the client more.

How to Hire and Prepare Your Appraiser Expert

You receive a total loss or diminished value offer, compare it to your vehicle, and something is off. The trim is wrong. Options are missing. The condition notes are thin. The insurer acts like the number is settled anyway. That is usually the point where owners need an independent appraiser who can do more than disagree. They need one who can prove why the offer is low.

Hiring the right appraiser expert witness starts with fit. For a vehicle owner, that means finding someone who knows auto valuation disputes, understands how insurers build these numbers, and can explain the difference between a supportable opinion and a hopeful one. A license, certification, or polished website helps. It does not answer the fundamental question. Can this appraiser produce work that holds up if the claim turns into appraisal, arbitration, or litigation?

Start with the claim path

The hiring process gets easier once you know what kind of dispute you have. A first-party claim with your own carrier may involve an appraisal clause. A third-party claim often starts with negotiation and may end in suit if the carrier refuses to correct a weak valuation. The appraiser should understand which lane your claim is in before offering an opinion about scope, timing, or cost.

Pull the file together early. A good appraiser can spot problems faster when the records are complete.

- Policy and claim documents: Keep the declarations page, valuation report, settlement offer, denial letters, adjuster emails, and any claim notes you received.

- Vehicle records: Gather purchase paperwork, service history, prior appraisal reports, window sticker or build data, and repair invoices.

- Loss-related materials: Save pre-loss and post-loss photos, body shop estimates, supplements, storage records, and odometer documentation.

Ask questions that show whether the appraiser is careful

Owners often ask the wrong opening question: “How much more can you get me?” The better question is how the appraiser reaches an opinion. An honest expert will stay with process, evidence, and limits.

Ask directly:

- Do you handle total loss, diminished value, or both?

- How do you define the market area for a vehicle like mine?

- How do you verify options, condition, prior repairs, and pre-loss history?

- What do you do when the insurer used poor comparables or missed key equipment?

- Have you testified before, and are you comfortable defending your report under oath?

- What documents do you need before you can give a reliable opinion?

- Will your report explain why certain comparables were rejected or adjusted?

Short, vague answers are a warning sign.

Hiring an appraiser green flags vs red flags

| Green Flags (Signs of a Pro) | Red Flags (Signs to Avoid) |

|---|---|

| Explains the assignment clearly: They can walk through valuation date, vehicle identification, market selection, and adjustment logic. | Promises a result early: No credible expert can promise a settlement number before reviewing the file. |

| Stays independent: They are there to support a defensible value opinion, not to repeat whatever number the owner wants. | Starts with your target number: That usually means the conclusion came before the analysis. |

| Requests records and photos up front: Careful review starts with documents. | Bare intake process: If they do not need much, they may not be doing much. |

| Understands claim procedure: They can explain whether their work is suited for negotiation, appraisal, arbitration, or court. | Dodges questions about testimony or prior challenges: That often signals weak report discipline. |

| Uses a repeatable method: The file shows where the comps came from and why adjustments were made. | Relies on instinct alone: “I know these cars” is not enough in a disputed claim. |

Prepare your expert with facts, not spin

Once retained, give the appraiser the full story. Owners sometimes worry that prior damage, repaint work, mileage discrepancies, or an old accident will hurt the case. Hiding those facts hurts more. If the other side finds an omission later, they will use it to attack the whole opinion, even if the final value was otherwise sound.

Good experts work with imperfect vehicles every day. What they need is accuracy. Point out errors in the insurer's report line by line. If the valuation lists cloth seats and your vehicle has leather, show the supporting documents. If it missed a technology package, send the build sheet or original sale paperwork. If the condition was better than the insurer described, provide dated photos and service records that support that position.

One option in this space is Total Loss Northwest, which states that it handles independent total loss and diminished value appraisals and invokes the appraisal clause in qualifying disputes. Whether you hire that firm or another, use the same standard. Choose an appraiser whose work can survive scrutiny and give you a fair shot at correcting a low insurance offer.

Oregon and Washington Auto Claim Specifics

In Oregon and Washington, vehicle owners run into the same core problem seen elsewhere. The insurer's value position often arrives dressed as final, even when the owner hasn't seen a careful, vehicle-specific analysis. That's exactly why local market knowledge matters.

A generic national approach can miss what buyers in the Pacific Northwest prioritize. Condition, drivability history, trim level, regional demand, and scarcity all affect how a vehicle trades on the market. That becomes even more important for trucks, outdoor-use vehicles, enthusiast cars, and specialty models that don't fit neat software assumptions.

Why local context matters

The legal standards don't change just because a claim involves a car instead of real estate. Reliability, documentation, and clarity still matter. But the underlying valuation work must fit local conditions.

In Oregon and Washington disputes, the practical questions are often these:

- Is the market area realistic: Are the comparables drawn from where a buyer would shop?

- Is the vehicle described accurately: Did the insurer miss options, packages, condition points, or prior repairs?

- Does the report reflect the local vehicle mix: Some vehicles are easier to replace in one market than another.

What owners should insist on

Owners in this region should expect an appraiser expert witness to do more than restate disagreement with the carrier. The report should be independent, market-based, and understandable to a non-specialist.

If a valuation can't be explained clearly to a judge, an arbitrator, or opposing counsel, it probably won't carry enough weight when the dispute gets serious.

That's where a regionally grounded appraisal has practical value. It isn't about inflating a claim. It's about making sure the evidence reflects the actual Oregon or Washington market the owner has to re-enter after the loss.

Take Control and Secure Your Fair Settlement

A low insurance offer puts individuals on the defensive. That's understandable. The carrier has already framed the value, and you're left reacting to their paperwork.

The better move is to change the frame. An appraiser expert witness does that by replacing argument with analysis. Instead of saying the insurer is wrong in general terms, you present a documented valuation that can be reviewed, challenged, and defended.

What this process is really for

This process isn't about starting a war with an insurer. It's about ending the dispute on fair terms.

For some claims, a strong independent report is enough to move negotiations. For others, the value of the expert shows up later, when the file is tested in appraisal, deposition, or court. In either setting, the same principle holds. The side with the clearer, more disciplined valuation usually stands on firmer ground.

What to remember before you accept

Keep these points in front of you:

- A settlement offer is not proof of value: It's the insurer's current position.

- Independent analysis matters most when facts are disputed: Mileage, condition, options, market area, and comparable quality can all change the outcome.

- The method has to survive pressure: A number without support won't help much when challenged.

- You don't have to handle the technical fight alone: That's what the expert is for.

If your vehicle was undervalued after an accident, the answer usually isn't more frustration. It's better evidence.

If you're dealing with a diminished value or total loss dispute in Oregon or Washington, Total Loss Northwest can help you understand whether an independent appraisal and expert-backed valuation are the right next step. A short consultation can tell you whether the insurer's number deserves acceptance, negotiation, or a formal challenge.