You read the claim email, see the number, and know right away it's wrong. The insurer says your car is a total loss, or says the repair payment should be enough, but the offer ignores what made your vehicle worth more than a generic listing in a database. Wrong trim, missing options, weak condition notes, and bad local comparisons can strip real money out of a claim.

Trust that instinct.

In Oregon, an auto appraisal gives you a documented value case you can present to an insurer. A certified appraisal is built to show more than a rough sticker price. It can identify hidden value in equipment, pre-loss condition, local market differences, and settlement add-ons such as taxes, title, and registration-related costs that are often mishandled or left out.

That is where drivers lose money. They focus only on the sale price and miss the rest of the claim.

A strong Oregon appraisal also matters because Oregon policies often contain an Appraisal Clause. Used correctly, that clause can shift the dispute from an adjuster's opinion to a formal valuation process supported by records, comparable sales, and a written report. That changes your position fast.

Do not rush to accept the first offer. Once you sign a release, your negotiating power is usually gone.

If the number feels low, stop. Get the car valued the right way, with Oregon rules, Oregon market data, and every settlement component accounted for.

That Sinking Feeling The Lowball Insurance Offer

You open the estimate, see the number, and your stomach drops. The insurer talks like the case is settled. You know your car was worth more than that, and you are usually right.

Low offers work because they sound official. A valuation report, a few comparable vehicles, a clean-looking summary page. That paperwork can still miss real money tied to your vehicle's actual condition, factory equipment, local Oregon market demand, and claim add-ons such as taxes and fees. The gap is often bigger than drivers expect.

The first job is to identify what the carrier left out.

Common problems include:

- Wrong trim or options: Premium packages, tech features, towing equipment, and other factory add-ons get missed or undervalued.

- Bad condition scoring: The report marks your vehicle down for wear, prior damage, or interior issues that do not match its pre-loss state.

- Poor comparable vehicles: The insurer uses sales that are older, farther away, less equipped, or not a fair match for your car.

- Incomplete settlement math: The offer focuses on vehicle price and shortchanges sales tax, title, registration, or other Oregon-specific costs.

That last point matters more than people think. A certified appraisal does not stop at a sticker-price argument. It builds the full settlement number, including the hidden pieces that often get buried in the carrier's worksheet.

If your car was repaired instead of totaled, you may also be dealing with a post-repair loss in market value. That is a different claim with a different method. If that is your situation, review how an Oregon diminished value claim works after repairs before you answer the adjuster.

In Oregon, a strong appraisal changes the fight. You are no longer arguing from memory or frustration. You are putting a documented value opinion in front of the carrier, backed by inspection notes, comparable market data, vehicle details, and the costs that belong in a proper settlement.

Do not treat the first number like a final answer. Treat it like an opening position, then challenge it with proof.

Total Loss vs Diminished Value Claims in Oregon

A lot of drivers mix these up, and insurers benefit when you do. Keep it simple.

A total loss claim is about the vehicle's pre-loss value. The car is gone, or the carrier is treating it as gone for settlement purposes. The question is what it was worth right before the crash.

A diminished value claim is different. The car gets repaired, but buyers still see a damaged-history vehicle. The issue becomes the loss in market value that remains after the repairs are complete.

Use this simple comparison

Think of a phone.

If the phone is crushed beyond practical recovery, that's a total loss problem. You're arguing over what the phone was worth before it got destroyed.

If the phone gets repaired with a replacement screen, but buyers would still pay less because it has a repair history, that's a diminished value problem.

Cars work the same way, but with much bigger financial consequences.

When each claim comes up in Oregon

For Oregon drivers, total loss disputes come up when the insurer says your vehicle's actual cash value is lower than what the market supports. That's where appraisals focus on sold comparables, vehicle condition, trim, options, mileage, and local market facts.

Diminished value comes up when the car is repairable but still worth less after the crash. This is especially important for high-value, leased, or modified vehicles, where market stigma can hit harder. Oregon-focused guidance points out that the key issue isn't pre-loss value in that situation. It's proving the market's reduced perception of the repaired vehicle, as explained in this guide to an Oregon diminished value claim.

A repaired car can still be a financial loss. Good body work fixes metal and paint. It doesn't erase accident history from the market.

Where people make the wrong call

Drivers often assume a repair check ends the claim. It doesn't. If you weren't at fault and the vehicle's post-repair value dropped, you may still have a diminished value issue worth pursuing.

Watch these categories closely:

- Luxury and performance vehicles: Buyers scrutinize accident history.

- Leased vehicles: Residual value concerns can become a real headache.

- Modified vehicles: Standard valuation systems often miss what owners invested.

- Late-model vehicles: A clean-history premium can disappear after one reported crash.

The point is straightforward. If the car is gone, challenge the pre-loss valuation. If the car is fixed but worth less, challenge the post-repair stigma loss. Don't let the insurer collapse both problems into one generic payment.

Why Insurance Company Valuations Often Fall Short

You get the valuation report, scan the number, and your stomach drops. The insurer says it is based on market data. Fine. That does not mean it reflects your car's real Oregon value.

Insurance company valuations are built to process claims quickly. Certified appraisals are built to prove value. Those are different jobs, and drivers pay for that difference when a report skips factory packages, misstates condition, ignores local demand, or leaves out Oregon-specific items that affect what a proper settlement should include.

A carrier's report usually starts with valuation software and a standard workflow. That workflow often pulls broad comparables, applies generic condition adjustments, and moves on. A certified Oregon appraisal does more. It checks the exact trim, verifies installed options, uses actual market evidence, and accounts for the taxes and fees that can matter in a total loss settlement here.

The software problem

Bad inputs produce bad numbers. If the report misses a premium audio package, tow package, upgraded wheels, driver-assist package, or unusually clean condition, the value drops. If it pulls comparables from the wrong area, the number gets worse.

That happens a lot with:

- Higher trims coded as base models

- Option packages omitted or undervalued

- Strong-condition vehicles treated like average used inventory

- Enthusiast or specialty vehicles compared to ordinary examples

- Oregon market demand flattened into a generic regional average

Adjusters also tend to defend the first report in the file. That is why arguing by phone rarely fixes the problem. You need a documented appraisal that forces the file back to the facts.

Where hidden value gets lost

Hidden value is usually hiding in plain sight. Trim level. Cab configuration. Factory technology package. Newer tires. Clean interior. Service history. Local scarcity. None of that is flashy, but all of it can affect what your vehicle was worth one minute before the loss.

Oregon drivers also get hurt when the insurer treats the settlement like a simple sticker-price exercise. It is not. A proper review looks at the vehicle's market value and the related Oregon costs that may apply to replacing it, including taxes and fees when supported by the claim and policy. That is one reason a certified appraisal can move a settlement more than owners expect. It finds value the software never bothered to price correctly.

If you are protecting a newer vehicle before any loss happens, condition still matters to resale. That is why guides on choosing between ceramic coating and PPF get attention from owners who care about preserving finish and buyer appeal.

The insurer's valuation is a production report. Your appraisal should be a case file.

Why an independent review changes the result

An independent appraiser is not there to defend the carrier's process. The job is to support a number that holds up under scrutiny. That means inspecting the vehicle records, checking comparable sales carefully, correcting missed options, and spelling out why the insurer's number is wrong.

That matters even more if your policy gives you a formal way to challenge value through the auto insurance appraisal clause process. A certified appraisal does not just argue that the offer feels low. It gives you the evidence to prove it.

If the offer came in light, treat that as a warning. Get the report reviewed. Lowball valuations usually are not mysterious. They are incomplete.

Using the Appraisal Clause to Get a Fair Settlement

If your offer is low and the carrier won't move, the most important document in the file is usually your policy. Specifically, the Appraisal Clause.

This clause gives you a contractual way to dispute value. In Oregon practice, each side selects an independent appraiser. Those appraisers try to reconcile the number. If they can't agree, an umpire decides the gap. For many drivers, that's the point where the claim stops being a one-sided negotiation and becomes a formal valuation dispute.

How the process works

The flow is simple, even if insurers sometimes act like it's exotic. A practical overview of the process appears in this guide to the appraisal clause in auto insurance.

Review the policy language

Confirm the clause exists and check how the policy says to invoke it.Invoke the clause in writing

Don't make this a phone-only dispute. Send a clear written notice.Choose your appraiser

Pick someone who knows Oregon valuation disputes and can document the file correctly.Let the insurer appoint its appraiser

They get their side. You get yours.Push for agreement or go to umpire

If the appraisers can't reconcile value, the umpire resolves the difference.

A quick visual helps if you want to see the steps laid out:

Why Oregon drivers should use it more often

Oregon gives you a long runway on diminished value claims. One Oregon-focused source states the statute of limitations is 6 years from the date of the accident under ORS 746.280-295, and it also notes that if the appraisers don't agree and an umpire decision comes back higher than the insurer's last offer, the insurance company is typically required to pay for the insured's appraiser and half of the umpire's fee, according to this Oregon diminished value and appraisal clause guide.

That changes the risk calculation. A lot of people assume appraisal is expensive and not worth the trouble. In many Oregon cases, that assumption is wrong.

The right way to invoke it

Keep your approach tight:

- Be formal: Send written notice, not a casual complaint.

- Be specific: State that you dispute value, not coverage.

- Attach support: Include the carrier's valuation and any obvious errors you've identified.

- Stop arguing in circles: Once the file stalls, use the clause instead of repeating the same phone call.

One more thing. Don't wait until frustration makes you sloppy. Invoke the clause when it becomes clear the insurer is defending a bad number instead of correcting it.

Anatomy of a Certified Oregon Auto Appraisal Report

You open the insurer's valuation and see a number. You still do not know how they got there, whether they used the right trim, or whether they included the money Oregon drivers are entitled to recover beyond the vehicle's base price. A certified appraisal report fixes that problem by showing the math, the market support, and the missing line items.

A thin insurer worksheet is built to justify an offer. A certified Oregon appraisal report is built to survive scrutiny. That difference matters when you are challenging a low total loss figure or proving diminished value after repairs.

If you want the short version first, this explanation of what an appraisal for a car is gives the basic framework. What matters in practice is what the report contains.

What a solid report should include

A report worth paying for should document the vehicle so clearly that nobody can pretend it was a different car.

Look for these core parts:

- Vehicle identification and configuration: VIN, year, make, model, exact trim, drivetrain, factory packages, and major options.

- Condition inspection: Photos and written notes showing pre-loss condition, post-repair condition, mileage, prior damage, and overall presentation.

- Comparable vehicle analysis: Real market comps that match your vehicle closely, with adjustments explained instead of guessed.

- Valuation method: A written explanation showing why each comp was used, why each adjustment was made, and how the final number was reached.

- Oregon settlement line items: Taxes, title-related charges, registration or licensing-related amounts, and other costs that can change the final settlement.

- Supporting exhibits: Carrier valuation errors, repair records, option lists, build data, receipts, and photos that back up the appraiser's conclusions.

That last point gets missed all the time.

Hidden value is usually not hidden at all

The money is often sitting in plain view. It is just left out of the insurer's first pass.

In Oregon, a strong appraisal report does more than argue over sticker price or a generic market average. It identifies missed options, corrects bad comparable choices, accounts for condition with evidence, and addresses taxes and fees that affect what a fair settlement looks like. That is where many low offers start to crack.

A weak report says your car is worth more. A strong report shows why, line by line.

What separates a useful report from a weak one

Ask direct questions before you rely on any appraisal:

- Did the appraiser confirm the exact trim and option package?

- Are the comparable vehicles similar in mileage, condition, and equipment?

- Are the adjustments explained in writing?

- Does the report deal with Oregon-specific taxes and fees, or does it stop at base value?

- Are the photos and records strong enough to defend the condition rating?

- Could this report hold up if the dispute goes to appraisal review?

If the answer to any of those is vague, the report has a hole in it.

Sample Valuation Comparison

| Valuation Line Item | Insurance Co. Offer | Independent Appraisal |

|---|---|---|

| Base vehicle value | Generic market number from carrier report | Market-supported value built from matched comparables |

| Trim and options | May be incomplete or simplified | Specific trim, packages, and equipment documented |

| Vehicle condition | Standardized deductions | Condition supported by inspection notes and evidence |

| Comparable vehicles | Limited or weak matches | Better-matched vehicles with reasoned adjustments |

| Tax, title, licensing | Sometimes minimized or unclear | Explicitly documented and justified where applicable |

| Final settlement position | One offer number | A supported valuation file for negotiation or appraisal |

That is the whole point. You do not need a prettier number. You need a report that finds the hidden value, documents it, and gives you something solid to put in front of the carrier.

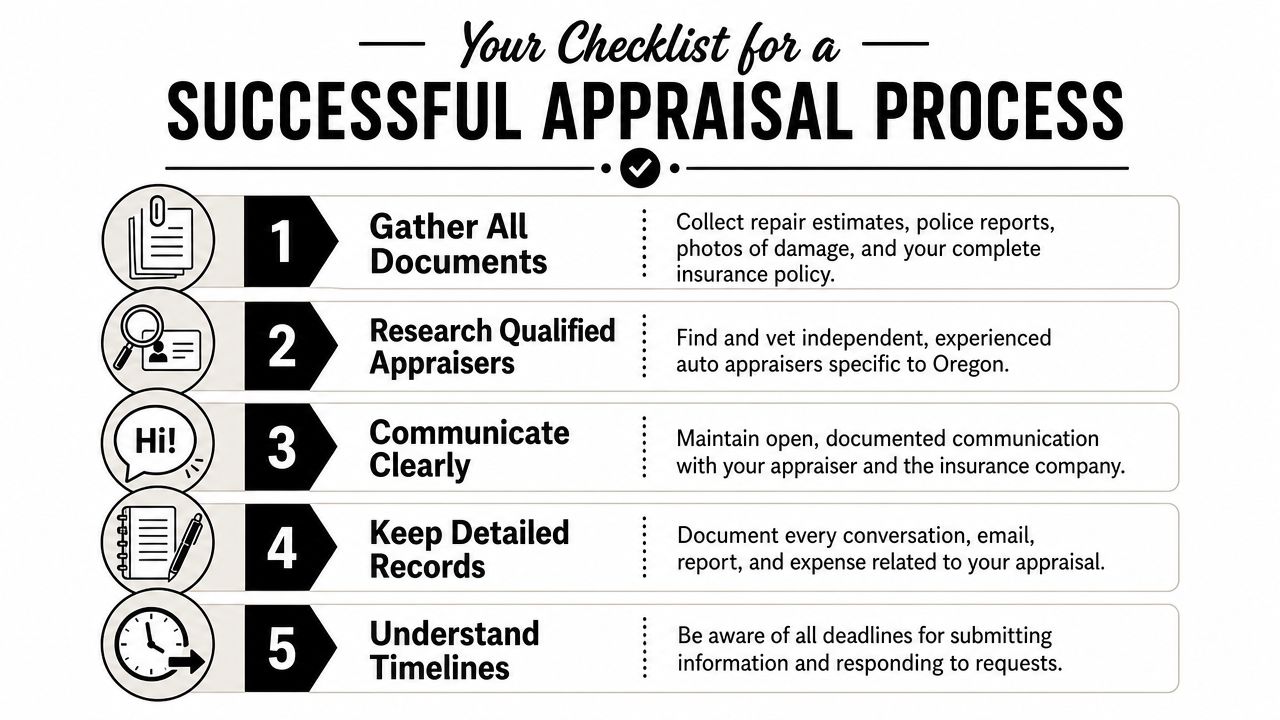

Your Checklist for a Successful Appraisal Process

You got the offer, looked at the number, and knew right away it was short. Good. Trust that instinct, then switch to proof.

A successful appraisal process in Oregon is won with a clean file, a certified report, and a written push for every dollar the carrier left out. Hidden value often sits outside the insurer's base number. Option packages, prior condition, local comparable choices, taxes, title, registration-related costs, and the policy's Appraisal Clause all affect the actual settlement position.

1. Get control of the file

Start by collecting every document tied to the claim. Do this before you argue with the adjuster again.

Pull together:

- The insurer's full valuation report

- Your policy and declarations page

- Photos of the vehicle, including damage, interior, exterior, odometer, and pre-loss condition if you have them

- Repair estimates or invoices

- Maintenance records

- Purchase documents, window sticker, build sheet, finance paperwork, or anything that shows trim and options

- Emails and claim notes that show what the carrier said and when they said it

Then mark the weak spots. Wrong trim. Missing options. Bad mileage adjustments. Poor comparable vehicles. Missing taxes or fees. Unsupported condition deductions. Make your appraiser's job easier.

2. Hire the right appraiser

Choose a certified Oregon appraiser who handles disputed insurance values. General car knowledge is not enough. You need someone who can inspect the vehicle, document condition, explain comparable adjustments, and write a report that stands up when the carrier pushes back.

Ask these questions before you hire anyone:

- Are you certified in Oregon?

- Do you handle total loss claims, diminished value claims, or both?

- Have you worked Appraisal Clause disputes under Oregon policies?

- Do you verify trim, packages, and factory options?

- Will the report address taxes, title, and registration-related costs when they apply?

- Do you inspect the vehicle or work only from photos and paperwork?

As noted earlier, Total Loss Northwest is one Oregon-Washington example in this space. The point is simple. Hire an appraiser whose report is built for a dispute, not just a number on a page.

3. Know what a proper appraisal should cover

A good appraisal does more than restate market price. It should find the money the carrier skipped.

That means the appraiser should verify the exact vehicle configuration, inspect condition closely, review local and relevant comparables, explain every adjustment, and calculate the settlement position the way an Oregon claim should be paid. If the report ignores taxes and fees that belong in the claim, it is incomplete. If it glosses over options or uses weak comps, it is weak.

Keep every email, report, invoice, and text. Sloppy records lead to sloppy outcomes.

4. Use the report. Do not just admire it.

Once the appraisal is finished, send it to the insurer in writing and ask for a written response. Force the dispute onto specifics.

Your message should challenge:

- Incorrect trim, options, or equipment

- Unreliable comparable vehicles

- Condition deductions that are not supported

- Missing taxes, title, licensing, or other settlement components

- Any refusal to apply the Appraisal Clause when the policy allows it

Set your own follow-up deadline. If the carrier stalls or keeps defending a bad number, invoke the appraisal remedy in the policy and move the claim forward.

5. Final send checklist

Before you submit anything, make sure you have:

- The insurer's offer in writing

- The carrier's valuation report

- Your photos and service records organized

- A clear claim type, total loss or diminished value

- An Oregon-certified appraiser

- A report that identifies hidden value beyond base vehicle price

- A written demand that points to the exact errors

- A plan to use the Appraisal Clause if the carrier refuses to correct the offer

Treat this like evidence, not a complaint. That is how you turn a lowball offer into a fair settlement.