You bought the car because it meant something. Maybe it's a longhood 911 you spent years sorting out. Maybe it's an early Bronco, a Chevelle, or a survivor pickup that still wears most of its original parts. Then an insurer asks for “value,” and suddenly the conversation gets reduced to a database number that doesn't reflect the car in your garage.

That gap is where owners in Oregon and Washington get hurt.

A classic car isn't valued like an ordinary commuter. It carries originality, restoration decisions, market history, documentation, and claim-specific issues that generic insurance software rarely handles well. If you're dealing with a policy review, a total loss, or a post-repair diminished value dispute, a proper classic car appraisal gives you something far more useful than an opinion. It gives you documented evidence that can hold up in negotiations.

Why Your Classic Car Needs More Than a Guess

A lot of owners call only after the problem starts. The accident already happened. The adjuster already issued a number. The carrier already framed the discussion around depreciation and “comparable vehicles” that are not comparable.

That's usually the first mistake in the claim process. A classic car's value doesn't live in a generic pricing guide.

Where owners get trapped

In Oregon and Washington, I regularly see the same pattern. The owner knows the vehicle is special, but the file on the insurance side treats it like a used car with an age adjustment. That approach misses the reasons collector vehicles trade above or below broad market guides in the first place.

A professional classic car appraisal solves that by tying value to evidence:

- Physical condition: The report documents what the car is now, not what a database assumes it is.

- Originality: Matching numbers, factory-correct components, and period-correct details can change the value materially.

- Documentation: Restoration receipts, ownership history, awards, and build records help explain why your vehicle deserves a different number than a stripped-down comp.

- Claim context: In a total loss or diminished value case, the report addresses the actual dispute instead of producing a casual estimate.

Practical rule: If the insurer can summarize your collector car in one line item, they probably haven't valued it correctly.

Why a number alone isn't enough

The strongest appraisals aren't one-page letters with a figure at the bottom. They tell the vehicle's market story in a way another party can test. That matters when you're challenging a low total loss offer or proving that a repaired classic still carries accident stigma in the resale market.

A defensible appraisal also protects you from your own assumptions. Owners often overvalue restoration cost, while insurers often undervalue originality and provenance. Neither side wins with guesswork.

For classic vehicles, the right question isn't “What's the book say?” It's “How do we prove what this specific car would command in the actual market?” That's the standard that matters when money is on the line.

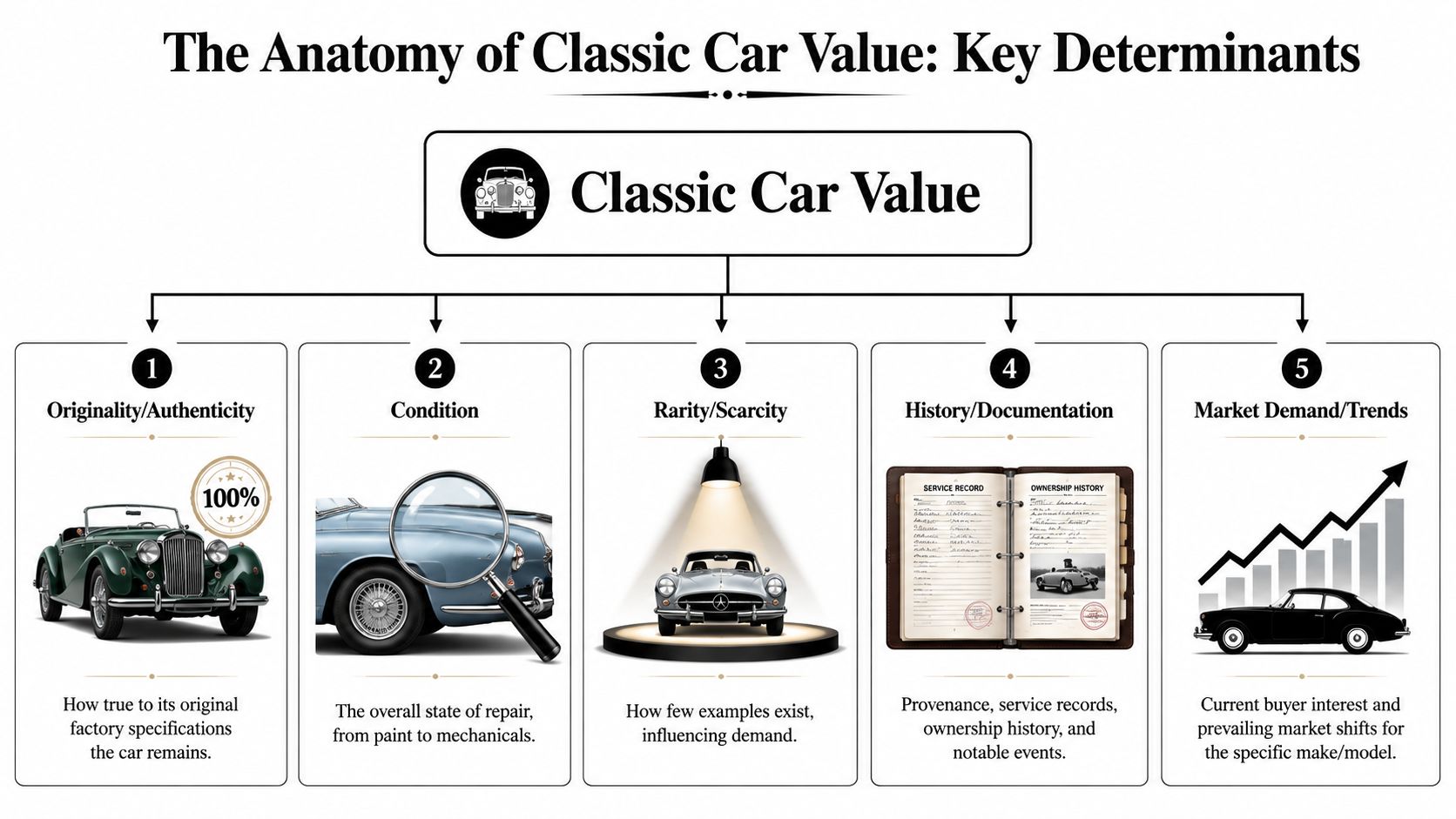

The Anatomy of Classic Car Value

A claim file can treat a 1967 Mustang as just another old Ford. A proper appraisal separates your car from the generic description by showing why buyers in the Oregon and Washington collector market would pay more, or less, for this specific example.

Condition sets the floor and ceiling

Condition still drives the value range. The collector market commonly uses a 1 to 6 condition grading scale, where 6 means unroadable and 1 means a perfect, museum-quality original according to Hagerty Valuation Tools. That gives appraisers and insurers a common reference point, but the core task is deciding where the car fits.

That judgment goes beyond paint gloss. I look at rust repair quality, panel fit, trim condition, glass, interior wear, drivability, undercarriage presentation, and whether prior repairs helped or hurt the car. In total loss and diminished value work, those details matter because insurers often price from photos and broad category labels. Owners pay for that shortcut.

Originality and provenance affect value in different ways

Originality answers a parts question. Provenance answers a proof question.

A car can be highly original and poorly documented. It can also be restored with correct components and backed by excellent records. Both situations can support value, but they do it differently. Original drivetrains, factory colors, date-correct components, and matching numbers usually carry weight with buyers. Service records, restoration invoices, ownership history, judging sheets, and factory paperwork make that claim easier to defend when an insurer pushes back.

If you are sorting out component changes before an appraisal, T1A Auto's guide on vehicle components helps explain why OEM and aftermarket choices can affect how a vehicle is judged.

Rarity only matters if buyers care

Owners hear "rare" and expect a premium. The market is stricter than that.

Limited production, unusual options, regional history, and low survival numbers can help. Demand still decides whether that rarity converts into dollars. A scarce trim with weak buyer interest does not perform like a scarce, highly sought specification. In the Pacific Northwest, local buyer preferences also matter. I see different reactions to trucks, Japanese classics, air-cooled cars, and domestic muscle than you might see in a national price guide.

Comparable sales need adjustments, not copy-and-paste pricing

Serious appraisal work uses comparables, then adjusts for differences in condition, originality, equipment, and documentation. Asking prices alone are weak support because they show seller ambition, not completed transactions.

For an owner-focused explanation of that method, this article on how to value a classic car gives the basic framework. In claims work, that framework matters because insurers often rely on poor comps, out-of-region sales, or vehicles with different restoration standards. A soft comp set can reduce a settlement offer fast.

The hardest call is original versus restored

Many valuation disputes turn at this point.

An honest, well-preserved original can outrank a fresh restoration if collectors for that model prize authenticity, factory finishes, and untouched details. A restored car can also win if the work is documented, correctly executed, and fixes issues that the market heavily discounts, such as corrosion, collision history, or incorrect mechanicals. There is no automatic rule that restored is better or original is better.

The appraiser's job is to show which story the market rewards for that make, model, and condition level. That point becomes especially important in Oregon and Washington insurance claims, where the difference between "older restored car" and "documented original example" can change both a total loss settlement and a diminished value position after repairs.

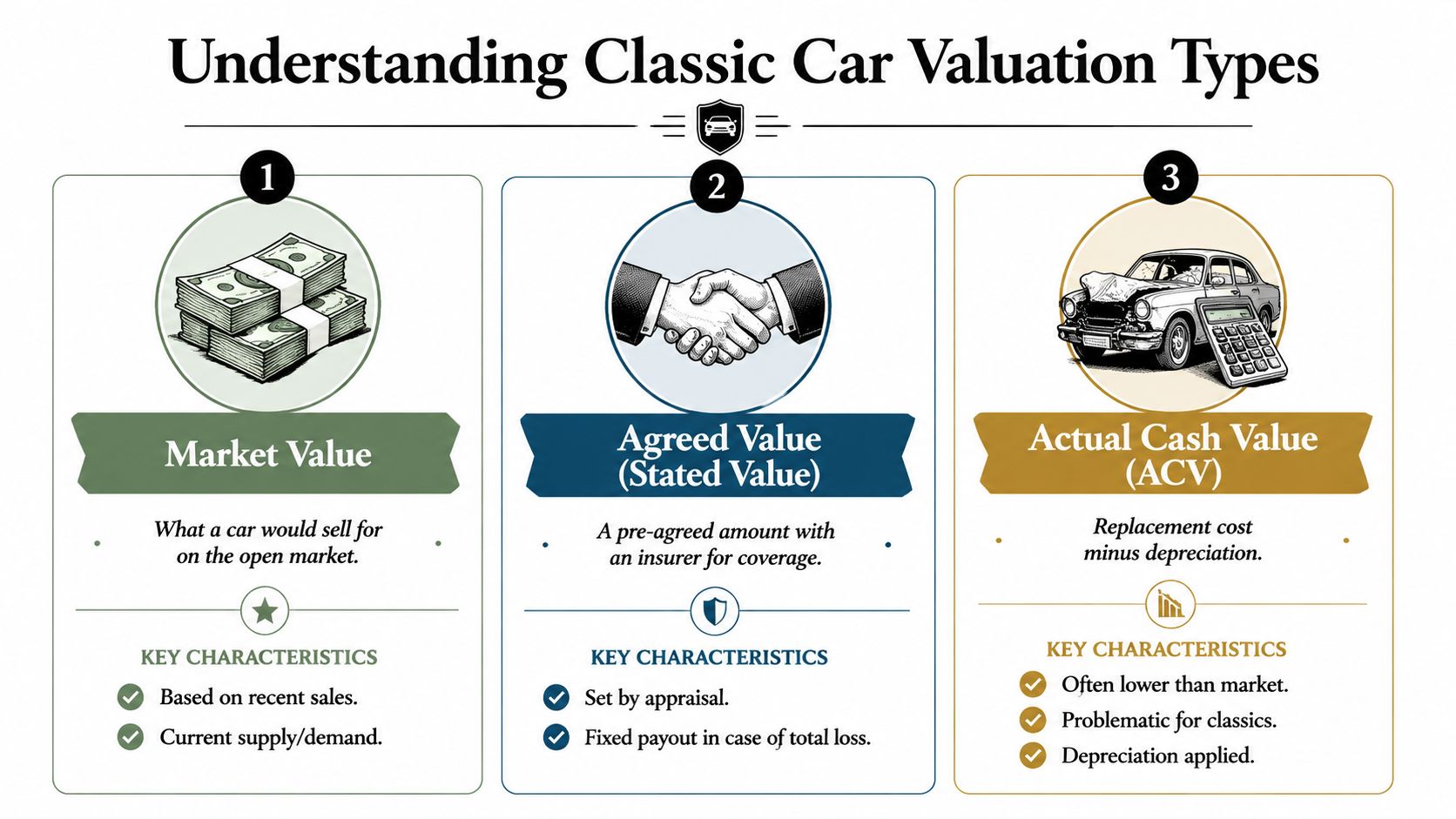

Decoding Appraisal Values Market vs Agreed vs Insurance

Owners get into trouble when they assume every valuation term means the same thing. It doesn't. In claims work, confusion over labels leads directly to underpayment.

Three values that sound similar but aren't

| Value type | What it means in practice | Where owners get burned |

|---|---|---|

| Market value | What the car would sell for in the open market based on comparable vehicles and condition | Weak comps or bad adjustments can drag the number down |

| Agreed value | A pre-set figure accepted by you and the insurer before a loss | If the amount is outdated, it may not reflect the current collector market |

| Actual cash value | The insurer's default claim framework, often tied to depreciation logic | It often fails to reflect collector status, originality, and niche demand |

What each one is good for

Market value is usually the right target in an appraisal dispute after a loss. It asks what this specific vehicle was worth just before the incident.

Agreed value works best before there's a claim. It can prevent the insurer from arguing ordinary depreciation later, but only if the agreed amount was set with solid support and revisited when the market changed.

Actual cash value, or ACV, is where classic owners usually are at a disadvantage. ACV frameworks tend to fit daily drivers better than collector cars. They can overlook originality, documentation, and the way specialty buyers behave.

If your classic is insured like a routine used vehicle, the claim often starts from the wrong premise.

Which number matters in an Oregon or Washington claim

For a total loss, the insurer may present its number as if it's objective and final. It isn't. An independent appraisal challenges the assumptions behind that figure and replaces them with vehicle-specific evidence.

For diminished value, the issue changes slightly. The car may be repaired, but the market may still discount it because an accident is now part of its history. That's a separate valuation problem, and it needs its own analysis.

The key is to know whether you're trying to set coverage ahead of time, challenge a post-loss market value, or prove value loss after repair. Those are different jobs, and each requires a different kind of valuation support.

The Classic Car Appraisal Process Step by Step

A claim gets harder the moment the insurer starts with the wrong car on paper. I see that in Oregon and Washington when a classic with real documentation, correct parts, or a high-quality restoration gets treated like an ordinary old used vehicle. A proper appraisal fixes that by creating a record the carrier has to answer, not wave aside.

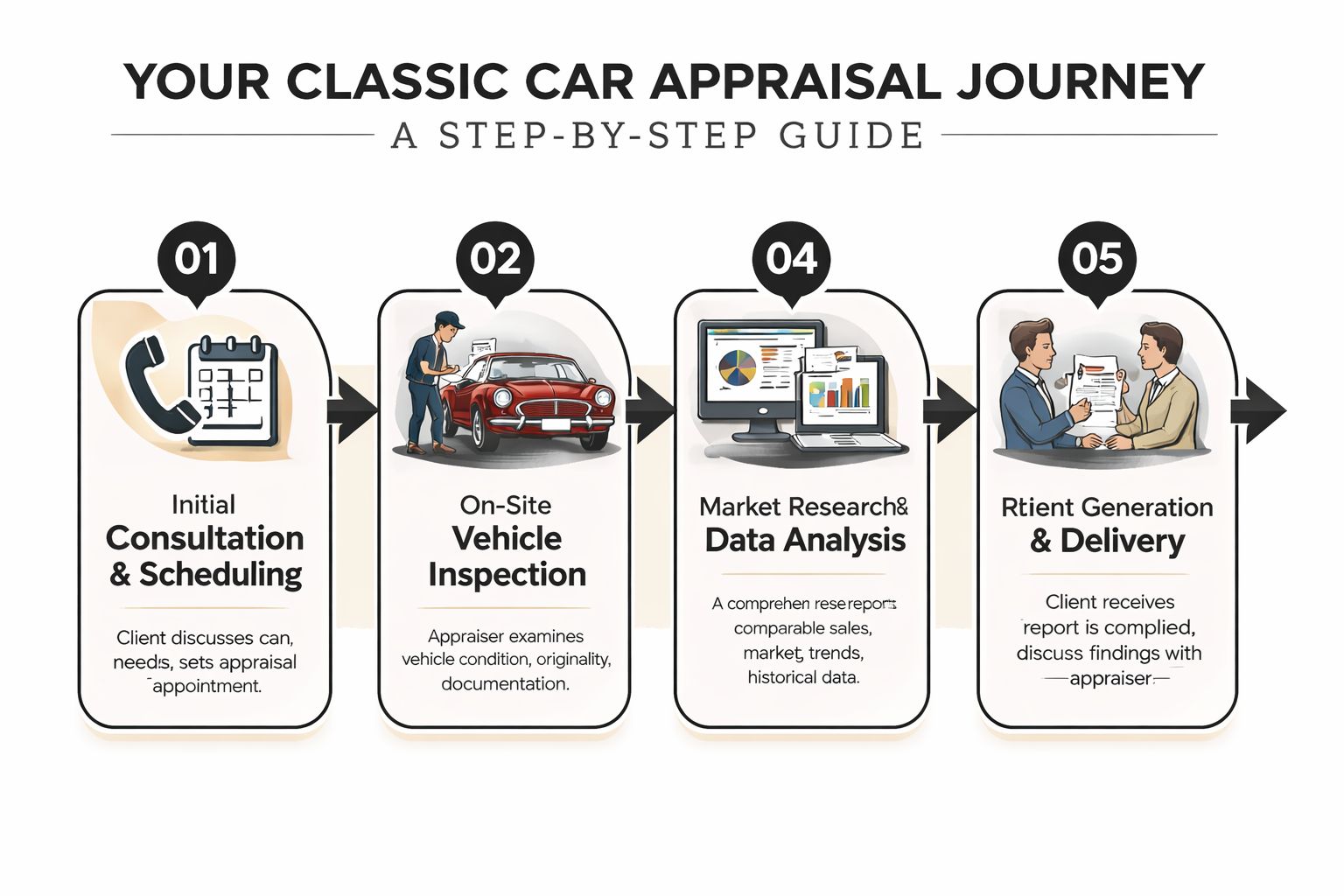

Step one and step two

The first step is defining the assignment correctly. A total loss appraisal asks what the vehicle was worth immediately before the loss. A diminished value appraisal asks how much market stigma remains after proper repair. A policy appraisal for agreed value is different again. If that question is framed poorly at the start, the report can miss the mark even if the inspection itself is solid.

The second step is the physical inspection. Formal appraisal workflows often involve an on-site inspection lasting about an hour or more, followed by a written report with photographs, as noted in iDrive Certified's appraisal overview. For owners dealing with a claim, this stage matters because it preserves details that disappear fast in an insurance file. Once a carrier labels a car as average, it takes evidence to pull the discussion back to the actual vehicle.

What gets inspected

A credible inspection records the details buyers, collectors, and adjusters dispute later:

- Body and alignment: Panel fit, rust, prior repair work, paint consistency, and signs of filler or structural correction.

- Interior and trim: Material quality, wear, missing pieces, correct finishes, and how original or accurately restored the cabin appears.

- Engine and driveline: Originality, replacement components, casting numbers or identifying marks when available, and overall presentation.

- Frame and structure: Corrosion, damage history, straightness, and repair quality.

- Documentation: Receipts, restoration photos, ownership history, build records, prior appraisals, and marque-specific paperwork.

Original versus restored condition needs careful handling here. An original car with honest age, matching components, and strong provenance can deserve a premium over a cleaner restored example. A restored car can also outrank an original one if the work is accurate, well documented, and done to a standard the market respects. The point is not to reward shinier paint automatically. The point is to measure what informed buyers in the Pacific Northwest market pay for.

Behind the report

After inspection, the appraiser studies the market and selects comparable sales or listings that match the subject vehicle closely enough to support real adjustments. Good reports use comparable vehicles with similar year, model, trim, equipment, condition level, and degree of originality or restoration. Regional context matters too. Oregon and Washington buyers do not always price cars the same way buyers in Arizona, Texas, or Florida do, especially where rust history, emissions-related equipment, and collector demand affect desirability.

Weak appraisals usually fail here. They use broad comps, skip adjustment logic, or mix restored cars with survivor-grade cars as if those differences do not matter. In claim work, that gives the insurer room to argue down the number. A defensible report explains why each comparable was chosen, what was adjusted, and how the final value was reached. Owners looking for classic auto appraisers for Oregon and Washington claim work should expect that level of explanation before they hire anyone.

A classic car appraisal should show the path to value clearly enough that an adjuster, attorney, or arbitrator can follow it.

What you should receive

The finished report should be written, signed, and supported by photographs. It should identify the vehicle by VIN and configuration, describe the inspection, list the records reviewed, discuss the comparable vehicles, and explain the final opinion of value in plain terms.

For insurance disputes, I also want the report to address the issues the carrier is likely to press. Was the car unusually original. Was the restoration older but still marketable. Did prior damage affect value before the current loss. Are there regional sales that support a stronger number than the insurer's generic database produced.

That is the difference between a file note and usable evidence.

Choosing Your Appraiser in Oregon and Washington

The person doing the appraisal matters almost as much as the report itself. In claim work, independence is not a small detail. It's the whole point.

Independence first

If the appraiser depends on insurer volume or promises to “work with” the carrier before even seeing the car, ask harder questions. Your appraiser should work for the valuation problem, not for the company trying to close the file cheaply.

Collector markets have moved too much over time for casual shortcuts to be safe. Between 2000 and 2020, the average value of top-tier collector cars increased by approximately 250%, which is one reason appraisals need regular updates and multi-source market analysis, as noted in Barrett-Jackson market analysis. Volatility like that rewards experience and punishes stale assumptions.

What to ask before you hire

Use direct questions. Don't settle for vague assurances.

- Ask about similar vehicles: Has the appraiser handled your make, era, and type of collector vehicle before?

- Ask about claim work: Do they appraise for total loss and diminished value disputes, or only for insurance policy setup and resale?

- Ask about methodology: Will they inspect the car physically and explain the comparable selection?

- Ask about disputes: Can they support the report if the insurer challenges the value?

- Ask about local familiarity: Oregon and Washington buyers don't always behave like national averages. Regional awareness matters.

If you're comparing independent options, this directory of classic auto appraisers in Oregon and Washington can help you start your search.

Red flags that should end the conversation

An appraiser shouldn't guarantee a number before inspection. They also shouldn't skip the vehicle exam, rely on one listing, or act annoyed when you ask how they handle insurer pushback.

The best reports aren't built from confidence alone. They're built from inspection discipline, market discipline, and documentation.

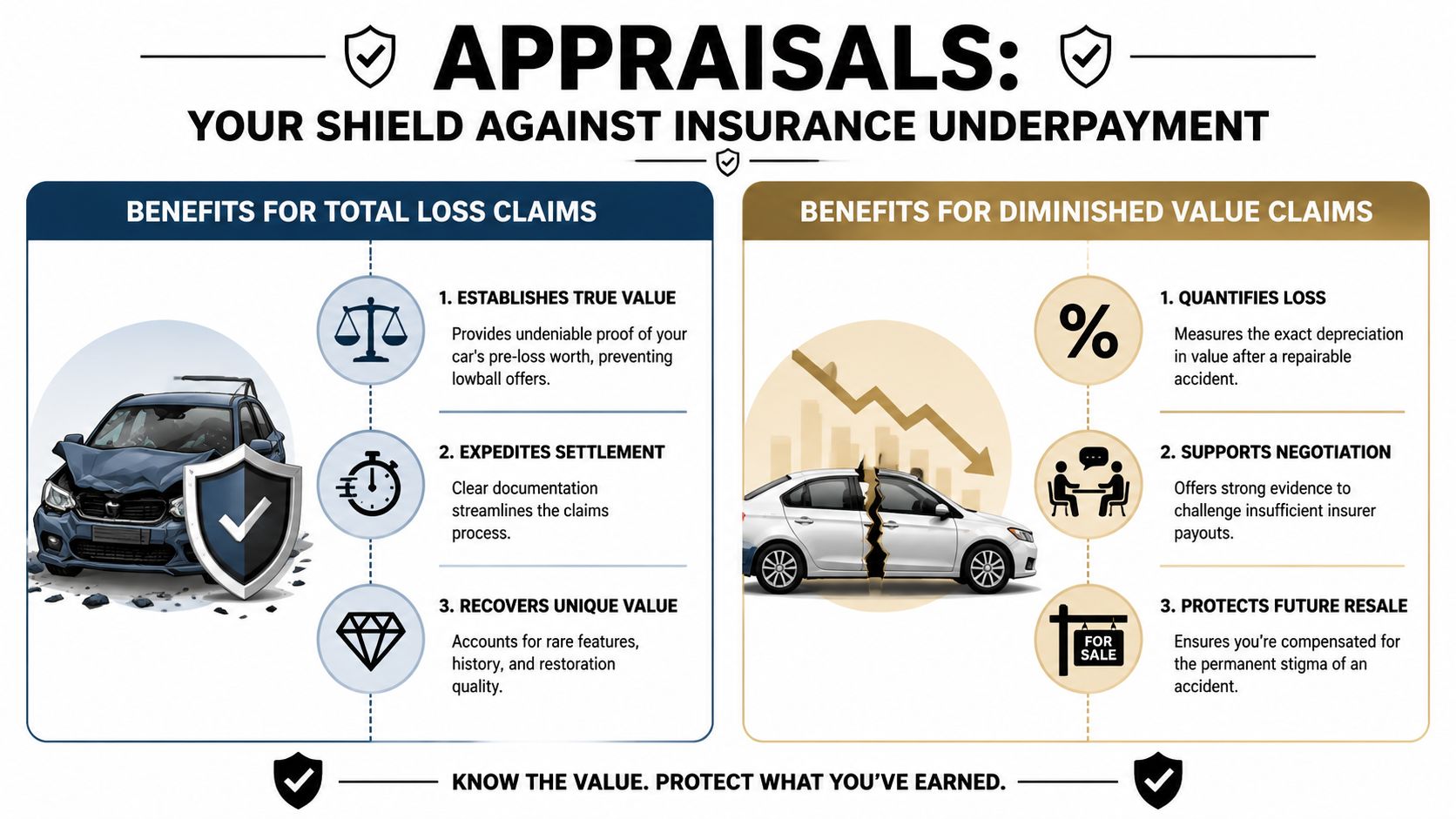

Using Appraisals for Total Loss and Diminished Value Claims

Your classic Mustang gets hit in Portland or Spokane. The body shop repairs it well, the paint matches, and the insurer says the file is resolved. Then the problem shows up. The car now carries an accident history, buyers start discounting it, and the carrier values it like any other old car with the same year and model designation.

That is where a proper appraisal earns its keep.

A collector claim usually turns on one of two disputes. A total loss claim asks what the car was worth one minute before the crash. A diminished value claim asks what the car lost because the crash is now part of its history, even after competent repairs.

Why insurer methods break down on classics

Insurance valuation systems are built for ordinary vehicles with broad, repeatable market behavior. Classic cars do not behave that way. The biggest gap shows up in the original versus restored question.

An original car with honest wear, matching components, and documented history can outrank a freshly restored car that looks sharper but has replacement panels, non-original driveline parts, or a color change. The opposite can also be true. A high-level restoration on the right car can bring more than a tired survivor. The point is not that one category always wins. The point is that value depends on specifics the software usually misses.

That gap matters in Oregon and Washington. Regional demand can favor trucks, air-cooled imports, muscle cars, or certain European restorations differently than national averages suggest. If an adjuster pulls generic comps from outside the Northwest and ignores local buyer behavior, the offer can come in low fast.

How the report helps in each claim type

For a total loss, the appraisal supports pre-loss fair market value with inspection findings, ownership history, condition analysis, and comparable sales that match the car's configuration and status. It gives you a documented basis to challenge an offer that glosses over originality, restoration quality, provenance, or regional demand.

For a diminished value claim, the assignment changes. The issue is no longer what the car was worth before the loss alone. The issue is the difference between pre-loss value and post-repair market value. On collector vehicles, that difference can remain even when the repairs are technically sound, because buyers pay attention to prior damage, replaced panels, and interruptions to an otherwise clean history. Owners dealing with that post-repair loss can review this guide to automobile diminished value claims for the claim framework.

Here's a short explainer on the role appraisals play in insurance disputes:

What helps your position, and what weakens it

What helps:

- A physical inspection that ties condition findings to photos, records, and market comps

- Comparable sales adjusted for originality, restoration level, options, and claim-related damage history

- A report written to withstand insurer scrutiny, not just to look polished

- An independent appraiser who understands total loss and diminished value disputes in Oregon and Washington

What weakens your position:

- Submitting restoration receipts without connecting them to current market value

- Relying on national listing screenshots with no adjustments for condition or region

- Accepting the insurer's category match when your car has unusual provenance or equipment

- Assuming repaired means the market treats the car as fully restored or fully unaffected

I tell clients the same thing in these cases. The insurance company's first number is an opening position, not the final measure of what the car was worth.

In Oregon and Washington, many owners need an independent appraiser for this specific claim work. Total Loss Northwest is one example of a firm that handles total loss and diminished value disputes and can participate in the Appraisal Clause process when the policy allows it.

Your Pre-Appraisal Checklist and Next Steps

A claim can turn on one missing document.

I see it often with Oregon and Washington owners after a theft recovery, collision, or fire loss. The car may be legitimate, well cared for, and worth more than the carrier's first number suggests, but the file is thin. If you want an appraisal that holds up in a total loss or diminished value dispute, prepare the car and the paper trail before the inspection date.

Good preparation does two jobs. It helps the appraiser verify the vehicle's identity, condition, and history. It also limits the insurer's room to argue that the car was over-restored, incorrectly represented, or unsupported by records. That matters with classics, especially where value depends on the difficult line between highly original and well restored.

What to gather before the appointment

Bring records that prove what the car is, how it was maintained, and what was changed over time.

| Document Type | Why It's Important |

|---|---|

| Title and registration | Confirms ownership and vehicle identity |

| Ownership history | Supports provenance and continuity |

| Restoration receipts | Shows the scope, quality, and timing of work performed |

| Build records or factory documentation | Helps confirm original equipment and options |

| Service and repair invoices | Shows long-term care and mechanical history |

| Awards, certifications, or judging sheets | Adds context for condition and market acceptance |

| Older photographs | Helps establish pre-loss condition and prior presentation |

| Parts documentation | Verifies OEM, period-correct, or replacement component choices |

| Prior appraisal reports | Provides historical context, though current value still requires fresh analysis |

Receipts matter, but they do not settle value by themselves. A $40,000 restoration can still produce a car worth less than an unusually original survivor. The reverse can also be true if the restoration corrected poor prior work and returned the car to proper specifications. The file needs to show which story applies.

How to prepare the vehicle itself

Present the car as it exists today. Clean enough to inspect, not polished to the point that defects are hidden.

Make sure the appraiser can reach and photograph the full vehicle, including the engine bay, trunk, VIN locations, undercarriage access points, and any removed parts that support originality. If the car is packed tightly in a garage, move it first. If paperwork is split across binders, boxes, and email printouts, consolidate it before the appointment.

That saves time, but above all, it reduces avoidable disputes later.

What to review after the report arrives

Read the report closely. Confirm the serial number, trim and option descriptions, drivetrain details, condition notes, and the way the appraiser classified the car. For insurance work, pay attention to whether the report clearly distinguishes original features from restored features, because that distinction often affects negotiations more than owners expect.

If the appraisal is being used for a Washington or Oregon claim, ask one practical question: how will this report hold up when the carrier challenges the comparables, the condition rating, or the effect of prior repairs? A usable report does more than state a number. It gives you support for the number.

If you are already in a claim dispute, an independent appraisal firm focused on total loss and diminished value work may be part of the next step, as noted earlier. The right time to line that up is before deadlines tighten and positions harden.