You open the valuation report, scan to the settlement number, and feel your stomach drop.

Your car was clean. The mileage was low. You kept the service records. Maybe it had the premium package, upgraded safety tech, factory wheels, or rare trim that took forever to find when you bought it. None of that seems to show up in the insurer's number. Instead, you get a report packed with “comparable vehicles” that don't look much like yours and a tone that suggests the matter is settled.

It isn't.

When an insurer values a total loss or diminished value claim, they want you to treat their report like a final answer. It's not. It's an opening position backed by software, search filters, and comp selection choices that often favor the payer, not the owner. If you want a fair outcome, you need better comparables for appraisal than the ones they used.

That means real market evidence. Not outrage. Not guesswork. Not “I know what my car was worth.” You win this fight by showing that the insurer's comps are weaker than yours, and that your evidence tracks what actual buyers would consider a substitute for your vehicle.

Your Insurer's First Offer Is Just the Beginning

Most drivers make the same mistake at the start. They assume the insurer's report must be objective because it looks formal.

It has a valuation date. It has adjustments. It has a list of vehicles. Sometimes it has pages of fine print that make the number seem untouchable. But a professional-looking report can still be built on weak comparables, bad condition assumptions, missing options, and a search area that was stretched until cheaper vehicles appeared.

I've seen owners accept low offers because they were exhausted, busy, or intimidated by the paperwork. I've also seen owners push back with strong documentation and force a much better conversation. The difference wasn't luck. It was evidence.

What the number really represents

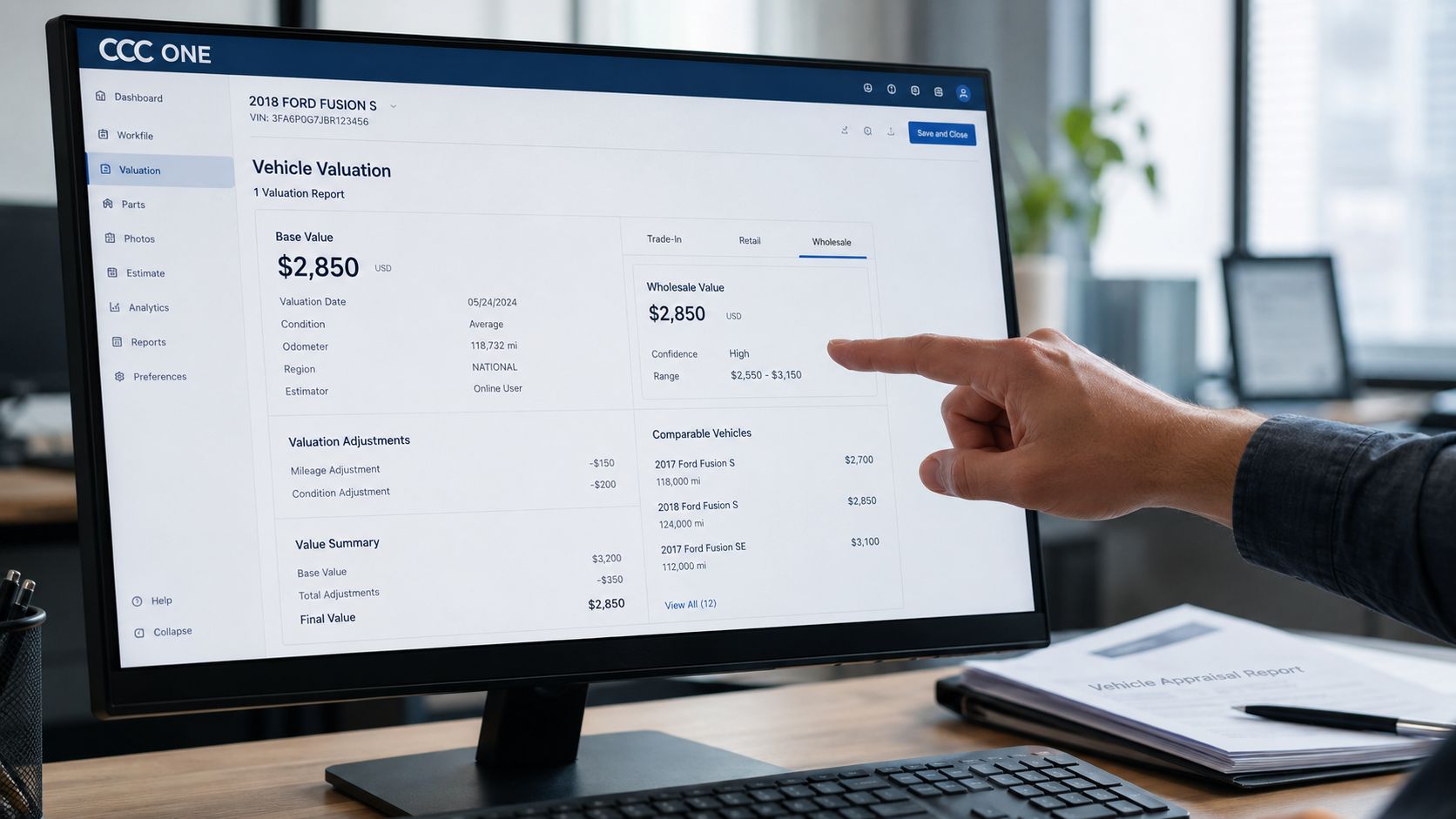

Your vehicle's Actual Cash Value, or ACV, isn't supposed to be a random figure an adjuster picked out of thin air. It's supposed to reflect the market. In plain terms, what would it cost to replace your vehicle with a similar one in your market, in similar condition, with similar mileage, trim, and equipment?

That's where comparables matter. A comparable is just another vehicle used as a benchmark for value. But not all comps deserve equal weight.

The insurer's first number tells you what they're willing to start with, not what your vehicle was actually worth.

A bad comp can drag your value down fast. A strong comp can expose the weakness in the insurer's report just as fast.

What you need to do next

If you're staring at a low offer, stop arguing in general terms. Don't lead with, “That feels too low.” Lead with documentation.

Start with these questions:

- Did they match your exact trim? An SE, SEL, Limited, Touring, Platinum, AMG line, or M Sport difference can matter a lot.

- Did they capture the right equipment? Factory navigation, driver-assist packages, upgraded audio, tow package, performance package, and appearance packages often get missed.

- Did they use the right condition? A well-maintained car with records shouldn't be valued against rough examples.

- Did they search in your actual market? If they reached too far to find cheaper inventory, the report may be tilted from the start.

That's the frame you want. Not emotion. Not frustration. Market evidence.

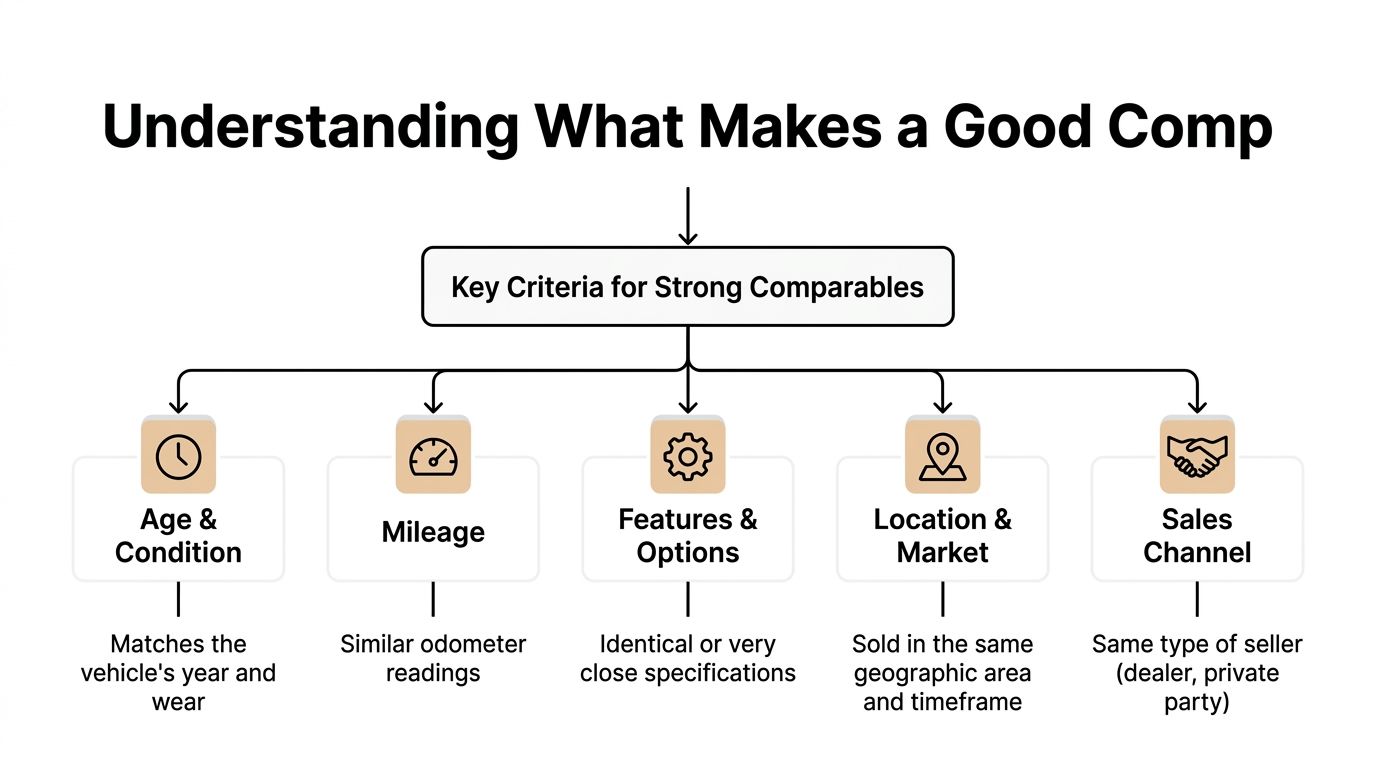

Understanding What Makes a Good Comp

A good comparable works the same way in auto claims as it does in real estate. If someone tried to value your house by using a smaller home in a different neighborhood with fewer upgrades, you'd reject it immediately. You should apply the same standard to your car.

The best comp is the vehicle a real buyer would have considered instead of yours.

Match the vehicle before you match the price

People often get sloppy. They see the same make and model and stop there. That's not enough.

A proper comp should line up as closely as possible on the details that drive replacement cost:

- Year, make, model, and trim: A base trim and an upper trim are not interchangeable. The badge matters because the market prices equipment, not just body shape.

- Mileage: Lower mileage generally places a vehicle in a different market position than a higher-mileage unit.

- Options and packages: Premium wheels, leather, technology packages, safety packages, factory towing, panoramic roof, upgraded suspension, and special appearance packages all matter if they're part of how buyers compare cars.

- Condition: Service history, cosmetic condition, tire condition, interior wear, prior repairs, and overall upkeep influence value.

- Location: The closer the market match, the better. A vehicle listed far away may reflect a different buyer pool and pricing environment.

The closer the substitute, the stronger the argument

If you want the short version, here it is:

A strong comp looks like your vehicle, is equipped like your vehicle, is worn like your vehicle, and is offered in the same market your vehicle would have sold in.

That's the standard.

If the insurer used vehicles with different trim levels, noticeably higher mileage, stripped-down equipment, or listings from far outside your market, they didn't build a strong valuation. They built a convenient one.

Don't ignore sales channel and listing quality

Where the comp appears also matters. A dealer retail listing usually doesn't tell the same story as a rough private-party listing with weak photos and no VIN detail. If you're trying to establish replacement value, look closely at how the vehicle is being offered and whether the listing is complete enough to confirm trim and equipment.

A useful habit is to review a detailed vehicle market valuation guide while you gather your comps so you stay focused on market-based replacement evidence instead of broad pricing guesses.

Here's a quick screening checklist:

| Comp quality check | What to verify |

|---|---|

| Vehicle identity | Exact year, make, model, trim |

| Equipment | Factory packages and standout options |

| Odometer | Similar mileage range |

| Condition clues | Photos, service records mention, clean presentation |

| Market fit | Same or competing local market |

| Listing detail | VIN, seller type, enough info to confirm match |

Good comps aren't just “same model.” They're credible substitutes.

The Insurer's Playbook for Low Valuations

Insurers rarely say, “We're trying to pay less.” They don't need to. The report does the work for them.

They rely on valuation software and comp selection rules that can make a low number look neutral. To most drivers, that report feels technical and final. To someone who reads these every day, the patterns jump off the page.

They expand the search until cheaper cars appear

This is one of the most common tactics.

In total loss valuation cases involving well-optioned vehicles, low-mileage units, or markets where insurers artificially expand geographic search radii to locate cheaper inventory, the difference between the insurer's offered ACV and documented market value can exceed $3,000 to $5,000 per vehicle, and independent appraisers often find comp datasets showing values 10%, 15%, or even 20% higher than the insurer's algorithmic offer, according to Appraisal Engine's discussion of comparable vehicle insurance valuation.

That's not a rounding error. That's a comp problem.

If your local market is tight and your vehicle is desirable, the insurer has every incentive to cast a wider net until they find cheaper substitutes from weaker markets. The report may still call them “comparable.” That label doesn't make it true.

They flatten your trim and options

Software systems are only as good as the data fed into them. If your vehicle had uncommon factory equipment or a premium package, those features may be undervalued, misread, or ignored.

That happens a lot with:

- Luxury trims that share a model name with lower trims

- Special packages bundled under marketing names instead of simple line items

- Performance or appearance upgrades that change market appeal

- Tow, tech, or driver-assist packages that buyers actively shop for

When the software misses those items, your car gets compared to cheaper examples that look similar in broad strokes but aren't equivalent in the market.

They use comps with hidden defects

Read every comp in the report like you're cross-examining it.

Look for red flags:

- Inferior condition: rough paint, torn interiors, obvious wear

- Negative history: prior accidents, branded title concerns, poor listing transparency

- Weak photos: not enough detail to confirm condition or equipment

- Questionable trim match: seller title says one thing, VIN details say another

Insurers count on policyholders not checking.

A comp that can't be verified shouldn't control your settlement.

A quick walkthrough of how these reports are built can help you spot those weak points before you respond:

Treat the report like an argument, not a verdict

Once you see the tactics, the report loses some of its power. It's still important. It's just not sacred.

Your job is to challenge each weak comp on the record. If they reached too far geographically, say so. If they used lower trims, document it. If they missed equipment, identify it clearly. If they relied on rough or unverifiable listings, point that out line by line.

The insurer wants you reacting to the bottom number. You should be attacking the comp selection that created it.

Building Your Own Evidence File

You don't need a giant stack of random listings. You need a clean file that shows the insurer's comps are weaker than yours.

That file should be organized, dated, and easy to follow. If you send an adjuster a messy batch of screenshots with no explanation, you make their job easy. They'll ignore it. If you send a structured evidence package with clear matches and notes, you force a response.

Where to find better comps

Start with active retail inventory and local dealer listings. Then widen carefully if needed. Good sources usually include national marketplaces, local dealership websites, and classified listings when they provide enough detail to verify the vehicle.

Use sources like AutoTrader, Cars.com, CarGurus, dealer inventory pages, eBay Motors, Facebook Marketplace, and Craigslist with caution. For every listing you save, capture the full details while it's still live.

Your evidence file should include:

- Listing screenshots: Save the price, VIN when available, mileage, seller, and location.

- Full-page PDFs: Listings disappear. Archive them early.

- Vehicle notes: Record trim, packages, condition clues, and anything that makes the comp stronger or weaker.

- Your own vehicle records: Window sticker if you have it, service records, purchase documents, photos, and prior listing details.

If you need a structure to keep all of that straight, a practical auto claim documentation checklist helps you keep the evidence usable instead of chaotic.

Don't filter by price

Often, many people accidentally copy the insurer's bad method.

Current resources often miss the point that limiting appraisal searches to a specific price range can exclude the most relevant comparable, and the stronger approach is to prioritize physical, legal, and economic attributes over a narrow price bracket, as explained in Working RE's analysis of search parameters and the best comparables.

That matters because a true substitute doesn't become irrelevant just because it's priced above the insurer's offer. In fact, that's often the entire issue.

Practical rule: Search for the right vehicle first. Let the price tell the story after you've matched the attributes.

Build the file like a professional

A strong evidence file usually works best when you separate it into simple parts:

Subject vehicle page

List your year, make, model, exact trim, mileage, VIN, options, condition summary, and market area.Comparable listings section

Put each comp on its own page or block. Add screenshots, seller details, and short notes about why it matches.Comp critique section

Take the insurer's comps one by one. Note trim mismatch, mileage issues, missing options, poor condition, distance, or unverifiable details.Adjustment notes

If a comp isn't perfect, explain the difference and whether it should move the value up or down relative to your vehicle.

You're not trying to overwhelm the adjuster. You're trying to make it hard for them to pretend your research is weak.

How to Adjust Comps for a True Comparison

You probably won't find your exact vehicle, with your exact mileage, options, and condition, sitting in the exact same market at the exact right moment. That's normal. Appraisal work isn't about perfection. It's about disciplined comparison.

A comp becomes useful when you explain the differences instead of ignoring them.

Adjust the comp, not your expectations

The basic rule is simple. If the comparable is inferior to your vehicle, its price needs to move upward to reflect your vehicle's stronger position. If the comparable is superior, its price needs to move downward.

That logic applies to common differences like:

- Mileage: If the comp has more miles than your car, it may support a higher adjusted value for your car.

- Options: If your car has equipment the comp lacks, the comp may understate replacement value unless you account for that gap.

- Condition: A rough comp shouldn't sit unadjusted beside a clean, well-kept subject vehicle.

- Market position: Dealer-ready inventory and weak private-party listings don't always belong in the same bucket.

The mistake insurers make is pretending small-looking differences don't matter when those differences stack on top of each other.

Comparable Vehicle Analysis Example

| Attribute | Insurer's Comp | Your Comp |

|---|---|---|

| Trim match | Similar model, lower trim | Exact trim match |

| Mileage | Noticeably higher than subject | Close to subject |

| Options | Missing premium package | Includes similar factory package |

| Condition | Limited photos, visible wear | Clean photos, well-presented |

| Location | Distant, cheaper market | Same local market |

| Adjustment logic | Minimal explanation | Differences clearly explained |

That table is simple on purpose. You don't need a flashy spreadsheet. You need logic that holds up under scrutiny.

Unique vehicles need a stronger explanation

This gets harder when the vehicle is uncommon. A collector car, luxury model, performance trim, heavily optioned truck, or customized build may not have true one-to-one comps nearby. That doesn't mean the insurer gets to grab any cheaper example and call it good.

For unique property where true comparables don't exist, the credible approach is to rigorously justify the use of significantly different comparables by describing the differences, analyzing market factors, and providing substantive commentary rather than relying on arbitrary adjustments, as explained in Mueller Reports' discussion of appraising a subject with no comparable sales.

That principle matters in auto claims too. If your vehicle is rare, the answer isn't lazy substitution. The answer is better support.

When exact comps don't exist, the quality of the explanation becomes part of the valuation.

That's why your notes matter. Don't just drop in a listing for a “close enough” vehicle. Explain why a buyer for your vehicle would also consider it, what's different, and whether that difference makes the comp stronger or weaker.

If you need help framing the replacement value side of that analysis, a fair market value calculation guide can help you normalize your comparables instead of just collecting them.

Presenting Your Case for a Higher Settlement

A strong file can still fail if you present it badly.

Adjusters are busy. If your evidence is scattered, emotional, or repetitive, they'll default to the insurer's original report. You need to package your case so the conclusion is obvious before they even finish reading.

What to send

Keep it tight. One PDF is usually better than a chain of emails with loose attachments.

Include these pieces in order:

- Summary letter: State that you dispute the valuation and that your enclosed comparables better reflect the local market.

- Subject vehicle details: VIN, trim, mileage, options, condition, and supporting records.

- Your comparable set: Screenshots, seller details, and short notes on why each comp is relevant.

- Critique of insurer comps: Identify mismatches and weak listings directly.

- Adjustment summary: Show how differences affect the comparison.

Language that works

You don't need legal jargon. You need plain, firm language.

Use wording like this:

I dispute the current valuation because the comparable vehicles used in the report do not reflect my vehicle's trim, equipment, condition, and local market. The enclosed comparables are closer substitutes and provide a more credible basis for value.

Or this:

Several vehicles in the insurer's report appear to be from a broader and less comparable market area, and multiple listings do not match my vehicle's equipment level. I'm requesting a revised valuation based on the enclosed evidence.

That's better than “I feel this is unfair.” Keep the focus on the comps.

Know your leverage

If the adjuster won't meaningfully engage with your evidence, check your policy for the Appraisal Clause. That clause can change the entire dispute.

It allows each side to hire an appraiser and move the valuation fight out of the insurer's internal software process. That matters because once the issue shifts to independent appraisal, the insurer's report stops being the only paper on the table.

Use the clause when:

- the adjuster keeps repeating the original number without addressing your comp critiques

- the report contains clear market or trim problems and they won't revise it

- the vehicle is unusual enough that software valuation was a bad fit from the start

You don't threaten it casually. You invoke it when the informal review has stalled and the evidence justifies escalation.

Common Questions on Finding Appraisal Comps

How many comps do I need

You need enough strong comps to show a consistent market picture. Fewer good comps beat a pile of weak ones. Quality wins.

Do private seller listings count

They can, if the listing gives you enough detail to verify trim, mileage, condition, and location. If the listing is vague or sloppy, it's weak evidence.

Do recent repairs help my claim

They can help support condition and maintenance, especially if they show your vehicle was better kept than the insurer assumed. Keep invoices and pair them with photos when possible.

If you're stuck with a low total loss or diminished value offer, Total Loss Northwest helps drivers challenge bad insurance valuations with independent appraisals, detailed market reports, and Appraisal Clause support. If the insurer built its case with weak comps, they'll help you answer with stronger evidence.