If another driver hit your car in Washington State, you're legally entitled to get paid for its lost resale value—even if the repairs were flawless. This loss is called inherent diminished value. Getting a professional appraisal is the only real way to prove your claim and get the money you're owed.

Your Right to Diminished Value Compensation in Washington

When an accident isn't your fault, the other driver's insurance pays to fix your car. Simple enough. But what about the permanent hit to its market value? That's where a diminished value claim in Washington State comes into play. No matter how great the body shop is, your vehicle now has an accident on its record, and that makes it harder to sell.

Think about it this way: say your car was worth $30,000 before the crash. After $8,000 in top-notch repairs, it looks perfect. But a CARFAX or AutoCheck report will show the collision history forever. A savvy buyer will use that history to negotiate you down, and its true market value might now be only $25,000.

That $5,000 difference is a very real financial loss, and Washington law is on your side to help you recover it.

Getting a Grip on the Core Concept

The most common type of claim we handle is for inherent diminished value. This has nothing to do with poor repair work. It’s the automatic, unavoidable drop in what someone is willing to pay for a vehicle simply because it's been in a wreck.

This isn't some legal loophole; it's a well-established principle. Washington courts recognize that owners should be compensated for this loss in market value on top of their repair costs. The entire point is to make you financially "whole" again, as if the accident never happened.

Why You Can't Wait for the Insurance Company to Help

Here's a dose of reality: the insurance adjuster's job is to close your claim for the lowest amount possible. They are absolutely not going to bring up diminished value if you don't. I've seen it hundreds of times. They will pay for the repairs and hope you go away, leaving thousands of dollars on the table.

It’s completely on you, the vehicle owner, to build a case, prove your financial loss, and demand fair payment.

To get started, you'll need to understand a bit of the lingo the insurance adjuster will use.

Essential Terms for Your Diminished Value Claim

Navigating your claim is much easier when you speak the language. Here are the key terms you’ll encounter during the process.

| Term | What It Means For You |

|---|---|

| Third-Party Claim | This is the claim you file against the at-fault driver's insurance. In this scenario, you are the "third party." |

| Inherent Diminished Value | The immediate loss of market value just because the vehicle has an accident history, even with perfect repairs. |

| USPAP-Compliant Appraisal | An appraisal following the Uniform Standards of Professional Appraisal Practice. This is the industry gold standard and gives your report the credibility it needs to stand up to scrutiny from the insurance company. |

These terms form the foundation of your claim. Having a solid, USPAP-compliant appraisal is non-negotiable; it's the evidence that transforms your claim from a simple request into a professional demand for what you are legally owed.

The Legal Foundation for Washington Diminished Value

So, you understand you’re owed money for your car's lost value. That’s the first step. But knowing you're right and actually getting the insurance company to pay up are two different things. This is where the law comes in, and thankfully, Washington State law is squarely on your side. Your diminished value claim isn't just a polite request—it’s a right.

Think of it this way: your claim has teeth because it’s backed by the same legal standards used in a courtroom. When you present your case, you're not just quoting an opinion; you're referencing the exact instructions a jury would use to decide how much you're owed. That’s a powerful position to be in.

Translating Washington Law into Your Claim

The key piece of evidence here is the Washington Pattern Jury Instructions – Civil (WPI). Don't let the legal-sounding name intimidate you. These are simply the official guidelines courts give to juries to help them calculate damages in a civil case, including car accidents.

The one you need to care about is WPI 30.10. It lays out two ways to calculate the loss for damaged property. The rule states that damages are either (1) what it costs to fix the car plus the loss in fair market value after it's been fixed, or (2) the difference in value before and after the crash if it's a total loss. You get whichever amount is less. You can dig deeper into these legal precedents for Washington state.

That phrase, "loss in fair market value after repairs," is the magic ticket. That is diminished value, spelled out in black and white within the state's legal framework.

Why This Legal Standard Matters

Now you're armed with something powerful. When an insurance adjuster tries to downplay your claim, you can push back with facts, not feelings. Adjusters have their own playbook, and one of their favorite tricks is a made-up calculation called the "17c Formula." It was created by an insurance company, for insurance companies, with one goal: to pay you as little as possible.

The 17c Formula is not the law in Washington. It’s an internal, self-serving tool that has no legal standing in your claim. A professional diminished value appraisal Washington state residents get is built on real market data, not some arbitrary insurance company spreadsheet.

You're under no obligation to accept an offer based on their flawed formula. Your claim should be grounded in the legal standard of WPI 30.10, period.

The Clock Is Ticking: Your Statute of Limitations

It's also crucial to remember that you don't have forever to act. The law gives you a specific window to file a claim for property damage.

- Statute of Limitations: In Washington, you have three years from the date of the accident to file a lawsuit for property damage.

While you'll want to get your claim moving long before that deadline, it acts as your ultimate leverage. If the insurance company is dragging its feet or lowballing you, the fact that you can take them to court within that three-year window gives your demands real weight. It signals to the adjuster that you’re serious and you know your rights.

When you build your claim on the solid ground of Washington's legal standards, the entire conversation changes. You're no longer just a claimant asking for a handout. You're an informed vehicle owner demanding the compensation you are legally and rightfully owed.

Building an Unbeatable Evidence File for Your Claim

A successful diminished value claim isn't about making demands; it's about proving a loss. You need to build a case file so solid and well-documented that the insurance adjuster has very little room to push back. Think of it less like asking for money and more like presenting an undeniable, fact-based argument for why you're owed it.

Your evidence file is your greatest asset in this process. Every piece of paper, every photo, and every note you take strengthens your position. From my experience, adjusters respond to well-organized proof, not just emotional appeals.

Your Essential Documentation Checklist

The best time to start gathering documents is right after the accident. If you wait, paperwork gets lost, details get fuzzy, and your claim gets weaker.

Here’s the core of what you'll need to create an ironclad file:

- The Official Police Report: This is your starting point. It's the official record that establishes who was at fault, a critical requirement for any third-party diminished value claim in Washington.

- High-Quality Photographs: Before a single repair is made, go to town with your camera. Get photos of the damage from every conceivable angle—up close to show broken parts, and from a distance to show the overall impact.

- The Final Itemized Repair Bill: This document is pure gold. It lists every single part that was replaced and details every hour of labor, providing concrete proof of how severe the damage truly was.

- Vehicle History Report: Pull a recent Carfax or AutoCheck report. This is how you prove your vehicle had a clean bill of health and a higher value before the collision.

When you put these documents together, you're not just collecting papers; you're telling a story that an insurance adjuster can't easily ignore. Each item backs up the others.

Pro Tip: Comb through that final repair bill. Did the shop use non-OEM (Original Equipment Manufacturer) parts? If they used aftermarket or even used parts to fix your car, that’s a powerful point in your favor. It’s a clear sign your vehicle was not, and could not be, returned to its exact pre-accident condition, which is the entire basis for diminished value.

Keeping Meticulous Records

Beyond the official paperwork, your personal notes are just as important. I always tell clients to keep a detailed log of every single phone call, email, and conversation with the insurance company.

Write down the date, time, the adjuster's name, and a quick summary of what was discussed. This creates a "paper trail" that can be incredibly useful if the adjuster starts dragging their feet, changing their story, or acting in bad faith. It shows you’re organized and holds them accountable. For more pointers on keeping your claim on track, you can find some great info among our other diminished value claim resources.

At the end of the day, a complete, organized evidence file is the foundation of any successful diminished value appraisal Washington state claim. When you pair this file with a professional appraisal report, you shift the dynamic. You're no longer just asking for a fair settlement—you're demanding it with a mountain of proof.

Finding a Credible Washington Diminished Value Appraiser

After a wreck, you’ll find that proving your car’s lost value is an uphill battle. Those free online calculators? They won't cut it with an insurance adjuster. Your most powerful tool is a detailed report from a qualified, independent appraiser. Honestly, finding the right professional is the single most important decision you'll make in your diminished value appraisal Washington state claim.

Think of it this way: the insurance adjuster's job is to close your claim for the least amount of money possible, and they often rely on questionable in-house formulas to justify a low offer. A credible appraiser’s report is your counter-punch—a valuation grounded in real-world market facts that they can't easily ignore. It becomes the bedrock of your entire negotiation.

What to Look for in an Appraiser

Not all appraisers are created equal, and you need someone whose work can withstand the heat an insurance company will bring. The absolute most critical credential to look for is USPAP compliance.

USPAP stands for the Uniform Standards of Professional Appraisal Practice, which is the quality control standard for the industry adopted by the U.S. Congress. A USPAP-compliant report isn't just someone's opinion; it's a rigorously researched document built on proven methods. This makes it incredibly difficult for an insurer to just brush it aside.

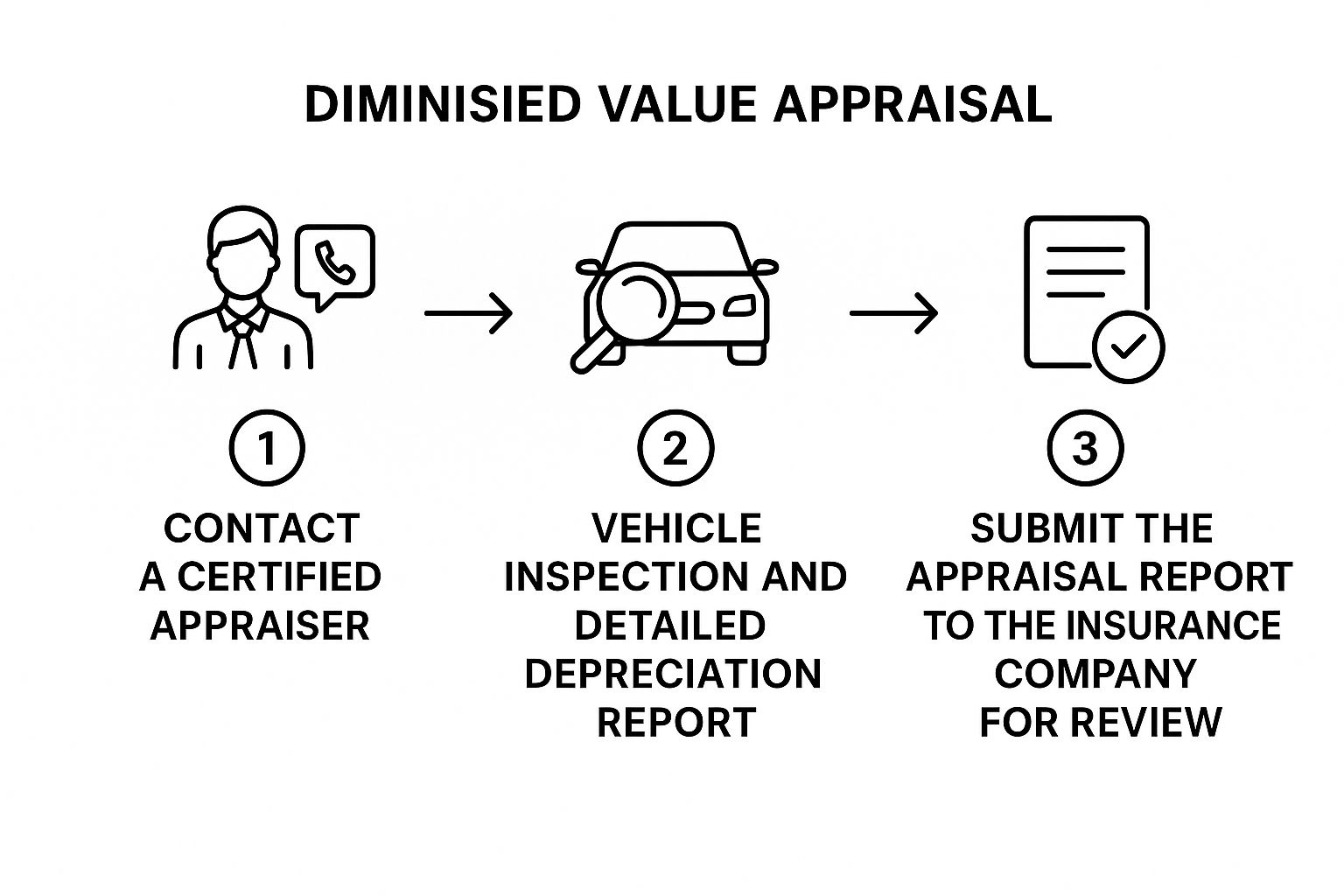

The process of working with a certified appraiser is actually quite straightforward.

It really is that simple: you connect with an expert, they inspect the vehicle, and you get a report to submit with your claim. This is the direct path to getting what you're owed.

Key Questions to Ask a Potential Appraiser

Before you hire anyone, you need to do a little vetting. The way an appraiser answers a few pointed questions will tell you everything you need to know about their experience and whether they can truly help your claim.

Here’s what I’d ask:

- Are your appraisals USPAP compliant? If they say no, or even hesitate, walk away. It's a non-negotiable.

- Do you have specific experience with claims in Washington State? Local market knowledge is absolutely essential for an accurate valuation.

- Have you ever testified in court as an expert witness? This is a great sign. It means their work is solid enough to survive a legal challenge.

- How do you counter the "17c Formula"? Any appraiser worth their salt will know this infamous insurer-friendly formula and should have ready-to-go strategies for dismantling it with actual market data.

A top-tier appraisal from an expert, like the ones at Total Loss Northwest, does far more than just spit out a number. It builds a case. It tells the story of your vehicle's lost value using undeniable proof, citing local dealership comparisons and the specific nature of your car's repairs. This level of detail elevates your demand from a simple request to a professional, evidence-backed claim the adjuster has to take seriously.

Getting Paid: How to Submit Your Demand and Negotiate a Fair Settlement

Alright, you've done the hard work. You’ve gathered your evidence and have a professional appraisal report in hand. Now it's time to formally demand what you're owed. This isn't about getting into shouting matches on the phone with an adjuster. The goal is to present a professional, ironclad case that puts the insurance company on the defensive from the get-go.

Your first official step is to draft a demand letter. Think of this as the opening move in a chess match. It needs to be clear, professional, and firm. Along with this letter, you'll send your entire evidence package—the police report, repair invoices, photos, and, most importantly, your USPAP-compliant diminished value appraisal. This packet immediately signals that you're serious and have done your homework.

How to Craft a Powerful Demand Letter

Your letter doesn't need to be a novel, but every sentence must count. It’s all about building an airtight argument.

Here’s what it should include:

- The Basic Facts: Start by briefly outlining the who, what, when, and where of the accident. Include the date, location, the at-fault driver's name, and their policy number.

- A Clear Statement of Fault: Directly state that their insured was at fault for the collision and reference the police report number as proof.

- A Nod to the Law: You can mention that under Washington State law and established legal principles (like those behind WPI 30.10), you are entitled to be compensated for the loss in your vehicle’s fair market value.

- The Expert Proof: State that you've enclosed a comprehensive appraisal from a certified, independent expert that calculates your exact financial loss.

- The Bottom Line: Formally demand payment for the full amount itemized in your appraisal report.

Taking this approach completely changes the dynamic. You're no longer just a claimant asking for a handout; you're presenting a formal, evidence-based claim backed by expert analysis and legal precedent.

Brace for the Inevitable Lowball Offer

I can tell you from experience: the insurance adjuster will almost certainly come back with an initial offer that’s a fraction of your appraised amount. Don't get discouraged. This is a standard opening move in their playbook. They're testing your resolve, hoping you'll take a quick, low payment and go away.

It's a well-known industry pattern. Nationwide, diminished value settlements often fall between 10% to 25% of a vehicle's total repair bill. To see how this plays out in the real world, a 2023 report from Maryland highlighted a case where an insurer first offered a mere $1,300 on a $15,000 repair. After the owner presented an independent appraisal, the final settlement jumped to $3,800.

This gap between their first offer and a fair settlement is exactly why your persistence and professional documentation are so critical. When that low offer lands in your inbox, your job is to respond professionally but without backing down.

Shutting Down Common Adjuster Arguments

The adjuster will have a script of common arguments they use to justify their low offers. If you know them in advance, you can counter them effectively.

Common Argument #1: "The repairs made your car whole again."

- Your Rebuttal: "I understand the repairs restored the vehicle's function, but they can't erase its accident history. That history is now a permanent, negative mark on the vehicle's record. Any informed buyer will pay significantly less for a car with a documented accident history, and my certified appraisal proves this specific market loss."

Common Argument #2: "Our internal formula (like the 17c) shows a much lower value."

- Your Rebuttal: "The 17c formula is an internal tool created by insurance companies for their own benefit and has no legal standing in Washington. My claim, however, is based on a USPAP-compliant appraisal. It uses real-world, local market data, which is the accepted professional standard for determining fair market value."

For a deeper dive into these tactics, check out our guide on how to negotiate your diminished value claim.

My final piece of advice? Keep all communication in writing. This creates a paper trail and holds everyone accountable. By staying firm, professional, and relying on your diminished value appraisal Washington state report, you hold all the cards needed to get the fair settlement you deserve.

Common Questions About Washington Diminished Value Claims

When you're trying to navigate the diminished value process, it's easy to feel like you're lost in a maze. A lot of questions pop up, especially when you're trying to make sense of insurance policies and legal fine print.

Let’s cut through the noise and get straight to the answers for some of the most common questions we hear every day. Getting these cleared up from the start will save you from hitting roadblocks and help you make much smarter decisions as you move forward with your claim.

Can I File a Diminished Value Claim if I Caused the Accident?

Unfortunately, the answer here is almost always no. In Washington, a diminished value claim is what the industry calls a "third-party" claim. That’s just a technical way of saying you can only file against the insurance company of the driver who was at fault for the collision.

Your own collision policy is there to cover the cost of repairs, but it specifically excludes paying for the loss in your car's market value. The legal idea behind this is that the person who caused the damage is responsible for making you financially "whole" again, and that includes compensating you for this very real loss in property value.

How Much Does a Professional Appraisal Cost in Washington?

You should expect a credible, well-researched diminished value appraisal in Washington to cost somewhere between $250 and $500. You’ll definitely come across free online calculators, but be warned: they spit out generic numbers that an insurance adjuster will laugh off without a second thought.

It's better to think of the appraisal fee as an investment. This cost pays for a detailed inspection of your car, a deep dive into local market data, and a professionally prepared, USPAP-compliant report. This isn't just a piece of paper; it's a powerful tool ready for negotiation or even court. A solid appraisal can boost your final settlement by thousands, making that initial cost a very smart move.

What if the Insurance Company Refuses to Pay My Claim?

If the at-fault driver's insurance company denies your claim outright or comes back with a ridiculously low offer, don't throw in the towel. You still have some powerful options.

A good first step can be to file a formal complaint with the Washington State Office of the Insurance Commissioner (OIC). They can investigate the insurer for acting in bad faith.

However, your most direct route to getting paid is often small claims court. Here's how that works:

- In Washington, you can file a lawsuit for up to $10,000 in small claims court without needing to hire an attorney.

- If your claim is for more than that, it's wise to at least consult with a property damage attorney.

Many times, the simple act of filing the court paperwork or having a lawyer send a formal demand letter is enough to make the insurance company suddenly willing to negotiate a much fairer settlement.

Don't let an initial denial stop you. An insurance company's first "no" is often just a negotiating tactic. A well-documented claim, anchored by a professional diminished value appraisal Washington state report, gives you the leverage you need to persist and succeed.

Is It Worth Filing a Claim for an Older or High-Mileage Car?

This is a great question, and the answer really depends on the car itself. Diminished value is definitely most significant on newer, low-mileage vehicles that were pristine before the accident.

For a standard sedan that's over 10 years old or has more than 100,000 miles, the inherent loss in value might be too small to justify the appraisal cost. But there are big exceptions. If your vehicle is a classic, a luxury model, or some other kind of specialty vehicle, its age and mileage don't hurt its value nearly as much. A trustworthy appraiser can give you an honest opinion on whether pursuing a claim makes financial sense for your specific car.

Don't let the insurance company dictate what your vehicle is worth. At Total Loss Northwest, we provide certified, independent appraisals to ensure you get the full and fair compensation you're legally owed. If your car has lost value after an accident, we're here to fight for you. Learn more about our certified appraisal services and get the settlement you deserve.