You picked up your car, the body lines look right, the paint looks clean, and the repair invoice says the work is complete. Then the first real-world question hits. What happens when you try to trade it in, sell it, or appraise it?

That repaired vehicle now carries an accident history. Buyers see it. Dealers discount for it. Marketplaces reflect it. Even when the repair shop did solid work, the car is not worth what it was worth before the crash.

That loss is called diminished value, and in Ohio, many drivers miss it for one simple reason. The insurer usually won't volunteer it. A proper diminished value claim in Ohio is a manual claim, not an automatic add-on to the repair check. If you don't raise it, document it, and prove it, the insurer often closes the property damage file without paying for it.

I tell drivers the same thing every week. If the other driver caused the wreck, repairs are only part of the financial loss. The other part is the hit to resale value. Ohio gives you a path to pursue that loss, but the burden sits on you from the start.

Your Repaired Car Is Back But It Is Not the Same

A common Ohio claim starts like this. The vehicle is repaired, the rental is returned, and everyone around you acts like the problem is over. Then you pull a CarFax or discuss trade-in value and learn what the market thinks of an accident history. It doesn't care that the bumper gap looks good or that the body shop followed procedure. It sees a car with a collision on record.

What drivers usually discover too late

The first surprise is emotional. You did everything right. You reported the crash, got the car repaired, saved the invoice, and moved on. Yet the vehicle still lost market appeal because the accident is now part of its history.

The second surprise is procedural. In Ohio, the insurer handling the at-fault driver's property damage claim usually won't calculate this loss for you on its own. You have to make the issue part of the claim.

Practical rule: If you don't specifically assert diminished value, many Ohio insurers will treat the repair payment as the end of the file.

That's the part that frustrates people most. They assume “made whole” includes the value loss. In practice, the carrier often pays for repairs and stops there unless the owner pushes further with proof.

Why the burden matters

Ohio allows diminished value claims, but the system isn't set up to spoon-feed them to drivers. The carrier already has the repair estimate, photos of physical damage, and maybe a supplement. None of that automatically proves what your car is worth on the open market after the repair is finished.

That market loss has to be built. The strongest files usually involve vehicles that are newer, low mileage, or luxury/high-value models because those vehicles tend to suffer the clearest resale stigma after a crash. Ohio also doesn't require a minimum repair amount before you can file. A claim can still exist without some magic damage threshold.

Here's the hard truth. A polite phone call saying “my car must be worth less now” rarely works. A documented claim does.

What a serious claim looks like

A real claim usually starts after the vehicle is fully repaired. That timing matters because diminished value depends on the type of damage, the scope of the repair, and how the repaired car compares to an accident-free version of the same vehicle in the marketplace.

At that stage, your job is to stop thinking like a customer and start thinking like a claimant.

- Save your repair file with estimates, supplements, and final invoices.

- Preserve photos from before and after repairs if you have them.

- Treat resale loss as a separate issue from repair quality.

- Move quickly while the paper trail is easy to gather.

Ohio gives you the right to pursue the loss. It doesn't remove the work needed to prove it.

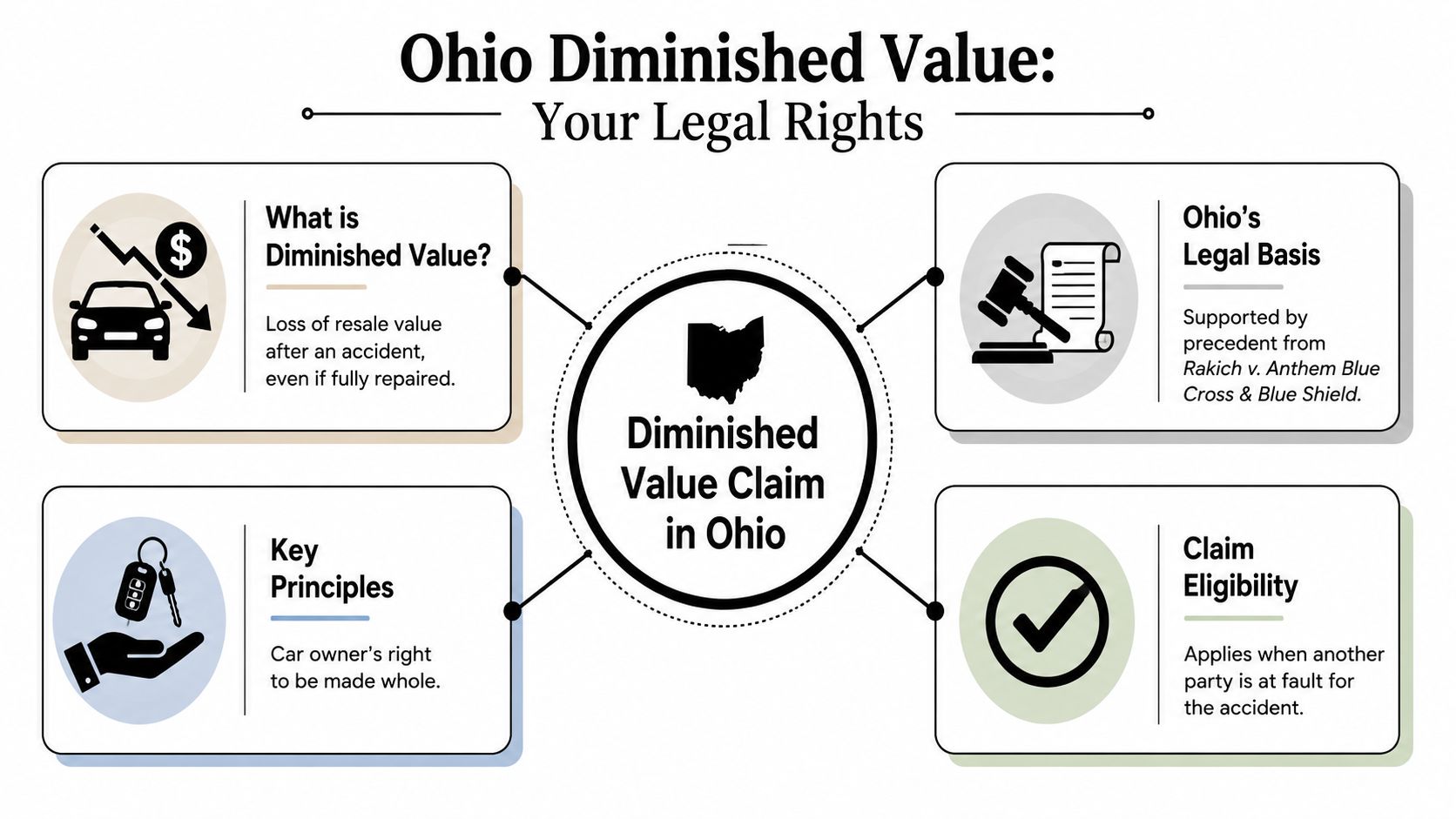

Understanding Your Right to Diminished Value in Ohio

Your car is repaired, the panels line up, and the shop says it is ready. Then you start thinking about trade-in value, a future private sale, or what a buyer will see on a history report. That is where many Ohio drivers hit the same wall. The insurer paid to fix the damage, but it does not volunteer to pay for the value that disappeared after the crash.

Ohio does allow a diminished value claim. The problem is that Ohio carriers usually treat it as a claim you must raise and prove, not a payment they offer on their own. As noted in AutoInsurance.com's diminished value guide, third-party claimants in Ohio have to document and argue the loss. If you do not make that case directly, the file often closes with repairs paid and nothing more.

The three forms of diminished value

Ohio drivers usually deal with one category more than the others, but the distinctions matter because adjusters often blur them together.

| Type | What it means | When it matters most |

|---|---|---|

| Inherent diminished value | Loss caused by the accident history itself, even after proper repairs | This is the claim most owners pursue |

| Repair-related diminished value | Extra loss caused by poor repairs, mismatched paint, or lingering defects | Important when workmanship affects market value |

| Immediate diminished value | Loss in value right after the collision before repairs happen | More theoretical for most post-repair claims |

For most Ohio claims, the primary dispute is inherent diminished value. A properly repaired vehicle can still bring less money because buyers, dealers, and appraisers discount accident history. That is a market reaction, not a repair invoice issue.

Repair-related diminished value is different. If the finish is off, welds are visible, warning lights remain, or parts fit poorly, the resale problem may be larger, but you are now arguing both market stigma and repair quality. That can increase the claim value, but it also creates more room for the insurer to argue.

Ohio is a prove-it state

This is the part drivers miss.

Ohio does not operate like a state where diminished value is routinely added behind the scenes. A fair settlement usually depends on whether the owner presents a file that shows the loss in a way an adjuster can evaluate. If you want a practical checklist for organizing that file, start with this guide to insurance claim documentation after a vehicle loss.

I tell Ohio owners the same thing in appraisal work. The legal right to pursue diminished value matters, but the claim rises or falls on proof. A clean demand with support behind it gets attention. A vague request gets denied or ignored.

For comparison, legal rules and claim handling can differ sharply from state to state. If you want to see how another state frames the issue, this guide on recovering diminished value after a Texas crash is useful as a contrast.

Later in the process, some owners find it helpful to hear the issue explained visually. This video does a good job of putting the claim concept into plain language.

Which Ohio vehicles usually have the strongest claims

Claim strength depends on how clearly the post-repair market penalty can be shown.

- Newer vehicles usually have less depreciation noise, so the crash-related loss is easier to isolate.

- Low-mileage cars often have more value to lose, and buyers tend to scrutinize their history more closely.

- Luxury and high-value models can suffer a sharper resale discount after structural or significant body damage.

- Well-maintained vehicles are easier to compare against cleaner market comps because their pre-loss condition is easier to support.

A weaker claim can still be valid. It just needs realistic expectations and better documentation.

Ohio gives drivers the right to seek diminished value. It does not give them a shortcut.

Building an Undeniable Case for Your Claim

Your car may look repaired and drive straight, yet the claim still fails if the file does not prove a market loss.

That is the step Ohio drivers miss. In Ohio, insurers do not automatically write a diminished value check after repairs. They usually wait for the owner to prove the loss with documents they can evaluate, challenge, and, if the file is well built, pay. A fair result usually comes from preparation, not from asking twice.

The independent appraisal carries the claim

If you pay for one outside item, pay for a credible diminished value appraisal.

Published benchmarks from Ohio diminished value claim benchmarks from MyDVAC report higher claim outcomes and better acceptance rates for owners who submit certified, independent appraisals rather than unsupported estimates. The same source also notes that insurers often expect comparative market analysis built from a meaningful set of relevant listings comparing clean-history vehicles against similar vehicles with prior damage.

That matches what happens in real files. Adjusters may dispute an appraisal, but they can process it. A personal opinion, an online calculator printout, or a number pulled from a forum post is much easier for them to dismiss.

What a credible appraisal should show

A useful report connects your specific damage history to a measurable resale penalty. It should not read like a form filled in with a final number at the bottom.

Look for these parts:

- Full vehicle details including year, make, model, trim, options, mileage, and pre-loss condition

- Damage and repair analysis identifying what areas were hit and whether structural, frame, weld, or major panel work occurred

- Pre-loss value support based on the market for your vehicle before the collision

- Post-repair market reaction explaining why buyers and dealers discount a repaired vehicle with this history

- Comparable market data using relevant listings, dealer data, and valuation support

- A final opinion of diminished value that follows from the evidence in the report

A report should hold up even if a supervisor or magistrate reads it with no context from you.

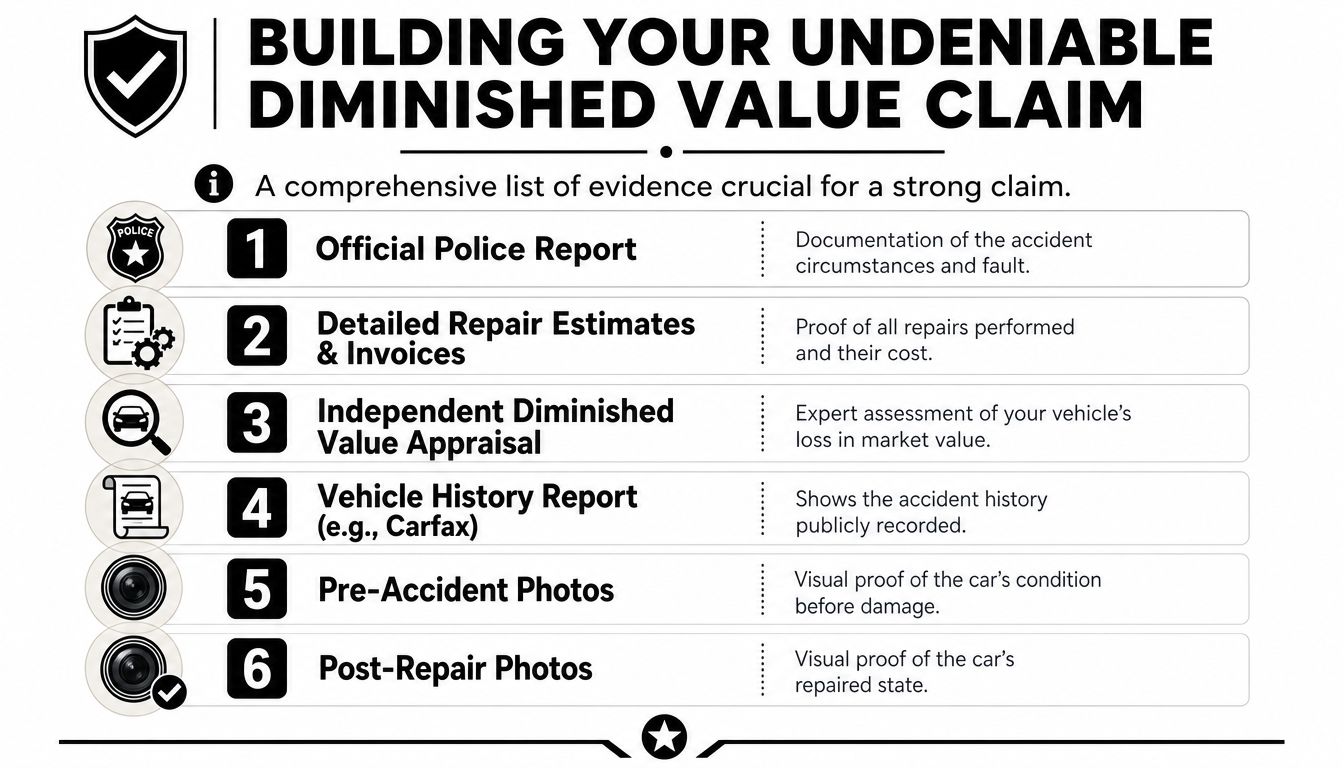

Build a file that closes the usual insurer objections

The appraisal is the anchor. The rest of the file keeps the carrier from attacking gaps around it.

Use this checklist:

- Police report showing the loss date, parties, and fault background

- Repair estimate and final paid invoice showing the scope of repairs completed

- Clear photos before the accident, if available, to support prior condition

- Clear photos after repairs to document final condition

- Maintenance records that show the vehicle was cared for before the crash

- Vehicle history report showing the accident entry now attached to the VIN

- Comparable listings for similar vehicles with and without accident history

- Any dealer trade-in or purchase comments referencing accident history, if you already tried to sell or trade the car

For help assembling those items into a clean package, review this guide to insurance claim documentation.

Weak proof usually fails for predictable reasons

I see the same mistakes over and over in Ohio diminished value files.

- Calculator-only claims produce numbers with no market support

- Owner estimates do not carry expert weight

- Missing final invoices leave room to argue the repair scope is unclear

- No comparable sales or listings make the loss hard to measure

- Claims filed before repairs are complete often rely on assumptions instead of final facts

Repair cost also gets confused with value loss. They are related, but they are not the same. A costly repair does not always create a large stigma loss. A moderate repair can hurt resale value more if it involves structural areas, multiple panels, airbag deployment, or damage that shows up badly on a history report.

Ohio claims are won by proving the loss before the adjuster has a reason to deny it.

How to Write and Submit Your Formal Demand

Your car is repaired. The claim is not.

This is the point where many Ohio drivers assume the insurer will recognize the remaining loss on its own. In Ohio, that usually does not happen. If you want payment for diminished value, you need to put a clean, documented demand in front of the adjuster and make the issue hard to dismiss.

A strong demand letter gives the carrier what it needs to evaluate the claim without guessing what you want or why you want it. It should read like a business document, not a complaint.

What your letter should include

Start with the file details. Give the adjuster no reason to delay the review because basic information is missing.

Include:

Claim and vehicle information

List your full name, claim number, date of loss, vehicle year, make, model, VIN, and current mileage.A brief liability statement

State that the other driver caused the collision and that the property damage claim is being made against that driver's insurer.A short repair status statement

Confirm that repairs are complete and that you are seeking payment for the vehicle's remaining post-repair loss in market value.The amount demanded

State the specific dollar amount you are requesting.The basis for that amount

Identify the independent diminished value appraisal and any supporting market evidence included with the letter.Your requested response date

Ask for a written response within a reasonable period, usually 10 to 14 business days.

Keep the tone controlled. Angry letters get read defensively. Clear letters get evaluated.

Make the appraisal the center of the demand

In Ohio, this is the step that gets missed. The insurer is not looking for your opinion that the car is worth less. The insurer is looking for a reason to accept, reduce, or deny the claim. A proper appraisal forces that review onto evidence.

State plainly that the vehicle has been repaired but still suffers measurable market stigma because the accident is now part of its history. Then tie your demand amount directly to the appraisal. Do not make the adjuster hunt for the number in a stack of attachments.

A simple statement works:

My vehicle has been fully repaired, but it has not been restored to its pre-loss market value. Based on the enclosed independent diminished value appraisal, I am demanding payment for the documented residual loss caused by this collision.

That is enough. The first letter does not need threats, case citations, or a long story about how frustrating the process has been.

Submit it in a way you can prove later

I tell Ohio owners the same thing every week. Send the demand like you may need to show a judge exactly what was sent and when it was delivered.

Use a method that creates a paper trail:

- Mail the package by certified mail

- Email the same package to the adjuster

- Combine the letter and supporting documents into organized PDFs

- Save your mailing receipt, email confirmation, and file copies

- Write down the date, time, and recipient for each transmission

If you want a practical model for formatting and tone, review this car accident settlement demand letter example.

Common demand letter mistakes

Weak Ohio diminished value demands usually break down in predictable ways.

- No appraisal is attached

- The demand amount appears without any explanation

- The letter focuses on repair cost instead of market value loss

- The packet is disorganized, which makes review slower and denial easier

- The demand is sent to the wrong carrier, department, or adjuster

- The owner asks for payment before the repair file is final

One more point matters. Do not undersell the issue by writing a vague sentence such as, “I believe my car may have lost some value.” That wording invites a soft denial. State the loss directly and support it.

A good formal demand changes the file from an informal request into a documented property damage claim the insurer has to address on the merits.

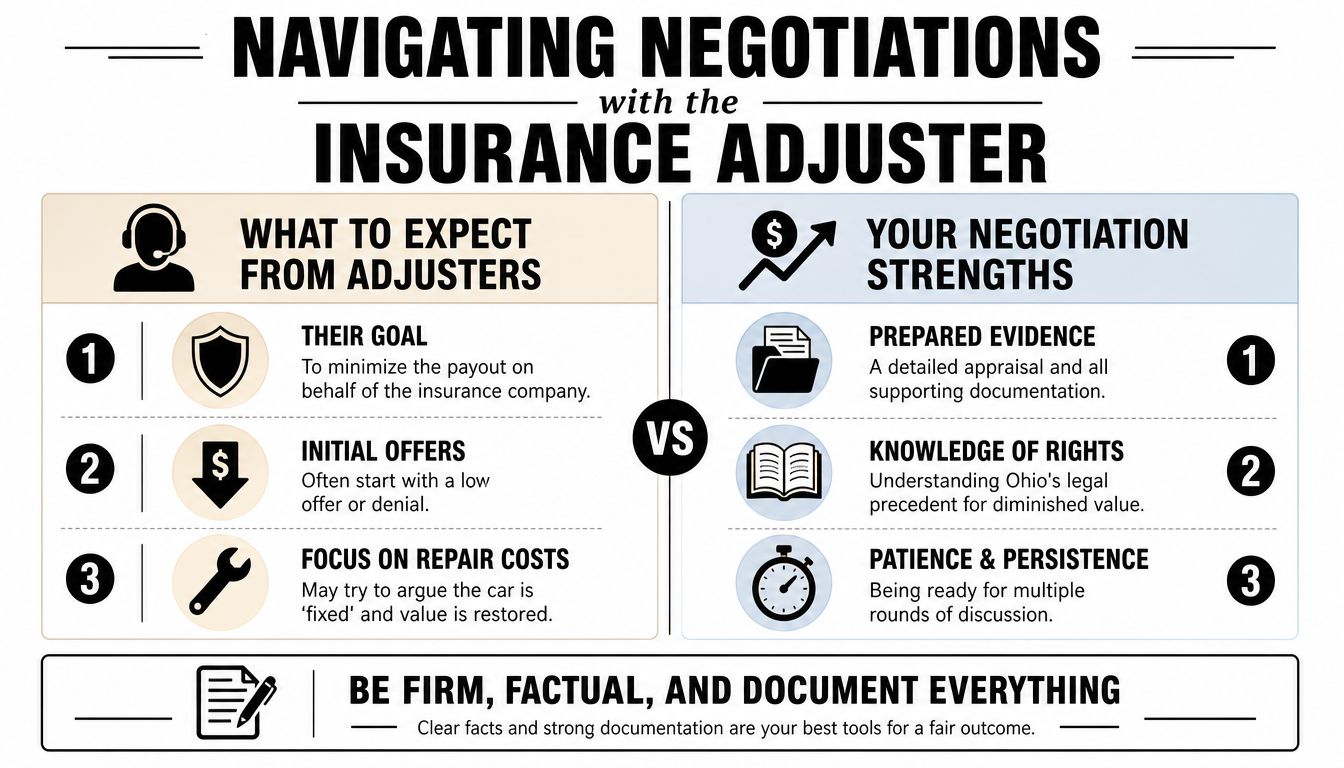

Navigating Negotiations with the Insurance Adjuster

Most diminished value negotiations in Ohio start with resistance. That doesn't automatically mean your claim is weak. It usually means the insurer is doing what insurers do. Test the file, narrow the issue, and try to pay less.

The adjuster's first move may be a denial, a token offer, or a statement that repairs restored the vehicle. Don't panic. Expect pushback and answer it with documentation, not anger.

The lowball formula you should recognize

One of the most common insurer tools is the 17c Formula. It's an industry-standard method often used to reduce claim values. Under the verified data, it caps the claim at 10% of the vehicle's pre-accident value before applying additional multipliers for damage severity and mileage. A vehicle with 30,000 miles may receive a mileage multiplier of 0.80, which further reduces the result.

That formula is easy for insurers to apply. It is not the same thing as a true market-based analysis.

Here's the practical problem. A formula cap does not automatically reflect how real buyers and dealers discount a vehicle with accident history. A market-supported appraisal often gives a more accurate picture because it looks at comparable vehicles, repair quality, age, mileage, and market demand together.

What to say when the adjuster leans on 17c

You don't need to argue about the formula in abstract terms. Bring the discussion back to your evidence.

Try responses like these:

- “My demand is based on an independent market appraisal, not a generic formula.”

- “Please identify where my appraisal's comparable analysis is incorrect.”

- “The report addresses the repaired condition, accident history stigma, and relevant market comparisons.”

- “If you disagree with the valuation, put your basis in writing.”

That last line matters. Adjusters are often more careful when they know their reasoning may be reviewed later by a supervisor, regulator, or court.

Stay factual. Ask for written explanations. The more specific the adjuster has to be, the harder it is for them to hide behind a script.

Common adjuster tactics and the right response

| Adjuster position | What it usually means | Your best response |

|---|---|---|

| “The car was repaired, so there's no loss” | They want to collapse repair cost and value loss into one issue | Point back to inherent diminished value |

| “Your number is too high” | They want you to negotiate against yourself first | Ask them to address the appraisal specifically |

| “We use our own valuation method” | They want to substitute a lower internal model | Demand a written explanation of their method |

| “This is all we can offer” | They're testing whether you'll stop | Reject politely if the evidence supports more |

How to negotiate without hurting your claim

Don't improvise. Keep every call brief, then follow up by email summarizing what was said. If the adjuster makes an oral offer, ask for it in writing. If they cite a reason for denial, ask them to identify the documents they relied on.

Also, don't confuse patience with passivity. A good negotiator follows up, keeps the file moving, and refuses to let silence become the insurer's strategy.

The drivers who do best aren't always the loudest. They're the ones with a disciplined record and a number backed by proof.

When to Escalate Your Claim in Ohio

Some claims settle after one or two rounds of discussion. Others stall because the adjuster won't move, won't explain the denial, or keeps circling back to a number that ignores the evidence.

At that point, you need to decide whether the claim is worth escalation. In many cases, it is.

The deadline you cannot miss

Ohio gives you two years from the date of the accident to file a diminished value claim under Rule 3901-1-54, and missing that deadline results in automatic dismissal of the claim. This timing rule is stated in the verified Ohio claim data provided for this article.

That means negotiation cannot drift forever. If the insurer is dragging the process out, the calendar becomes a real threat to your recovery.

Don't let a slow adjuster use up a fast deadline.

Your three practical escalation paths

File a complaint with the Ohio Department of Insurance

This is often the first escalation step when the insurer won't explain its handling or appears to be ignoring evidence. If you need help understanding that process, this guide on an insurance commissioner complaint is a practical reference.

Use small claims court when the dispute is manageable

For many drivers, small claims can be a cost-effective way to pressure a fair resolution. Your appraisal, repair invoices, photos, and written communications become critical here.

Hire an attorney when the case is contested or complex

Legal help makes the most sense when liability is disputed, the insurer is entrenched, or the value loss is substantial enough to justify the expense and pressure of formal representation.

A nuance drivers often miss

Ohio also has a partial-fault wrinkle that some consumer guides skip. The verified data indicates Ohio drivers may still recover in partial-fault scenarios up to 49% fault if injury occurred, and that 38% of denied diminished value claims involve partial fault according to the referenced Ohio legal discussion. That doesn't mean every partial-fault property damage case turns into a winning diminished value claim, but it does mean a quick “you were partly at fault, so you get nothing” should not end the analysis if your case fits that fact pattern.

The larger point is simple. A well-documented claim gives you options. A weak file leaves you hoping the adjuster feels generous. Hope isn't a claim strategy.

If you need a professional appraisal to support your diminished value position, Total Loss Northwest provides certified independent appraisals and diminished value support in all 50 states. Their work is built for negotiation, not guesswork, which matters when an Ohio insurer won't pay unless the loss is clearly proven.