When you get into a car accident, your first priority is usually getting your vehicle fixed. But here’s something most people don't realize until it's too late: even with perfect repairs, your car is now worth less than it was just before the crash. This permanent financial hit is called diminished value, and there are laws that allow you to get that money back.

The Hidden Cost of a Repaired Car

Think of it like this: Imagine you own a beautiful, antique ceramic vase. One day, it gets knocked over and shatters. You find the best artisan in the world to piece it back together, using a special golden adhesive that highlights the cracks as part of its history. The vase is whole again, functional, and maybe even uniquely beautiful. But it will never be worth what it was in its original, undamaged condition.

Your car is that vase. Even if the body shop does an amazing job, the accident is now a permanent part of its history, logged forever on reports from services like CARFAX. That accident record is a huge red flag for any savvy buyer. Given the choice between two identical cars, one with a clean history and one that's been in a wreck, they will always pay less for the one that’s been repaired.

Defining Inherent Diminished Value

This immediate loss in resale value, which exists no matter how good the repairs are, is called inherent diminished value. It's the most common type of claim drivers make after an accident. The repairs fixed the dents and scratches, but they couldn't erase the car's past or restore its original market value.

The core idea is simple: A car with an accident history is less desirable, and therefore worth less money. Diminished value law acknowledges this financial reality and gives you a legal pathway to recover that lost value from the at-fault driver's insurance company.

This guide will walk you through everything you need to know to tackle a diminished value claim. We'll break down how the process works, the evidence you'll need to gather, and the specific steps to take to get the money you're owed, with a focus on how things work for drivers in Oregon and Washington. The accident wasn't the end of your car's story—it's just the beginning of a new chapter where you have to fight to reclaim its full value.

Understanding the Three Types of Diminished Value

When you're trying to recover the money you've lost on your car's value, it helps to know that not all value loss is created equal. The term "diminished value" actually breaks down into three specific categories, and figuring out which one applies to your situation is the key to building a solid claim.

Getting these terms right gives you the language you need to negotiate effectively with insurance adjusters and appraisers. Each one pinpoints a different reason your car is now worth less, which makes your argument much harder for them to dismiss.

Let’s dig into the three types you might encounter.

The Three Categories of Diminished Value Explained

When you're dealing with an insurance claim, the specifics matter. The table below breaks down the three distinct types of diminished value, what they really mean for your car, and when each one typically comes into play. Understanding these differences is the first step toward getting the compensation you deserve.

| Type of Diminished Value | What It Means | Who It Applies To |

|---|---|---|

| Inherent Diminished Value | This is the automatic, unavoidable drop in your car's resale value just because it now has an accident on its record. Even with perfect repairs, the stigma of a crash history lowers what a buyer will pay. | Nearly every driver whose vehicle has been in a significant accident and repaired. This is the most common and widely accepted basis for a claim. |

| Repair-Related Diminished Value | This is extra value lost because the repairs themselves were botched. Think mismatched paint, cheap aftermarket parts that don't fit right, or lingering mechanical problems after you get the car back from the shop. | Drivers whose vehicles were not restored to their pre-accident condition due to poor workmanship. This loss is in addition to the inherent value loss. |

| Immediate Diminished Value | This is the difference in value between your car right before the accident and its value as a damaged wreck right after—before any repairs are done. | This is more of a technical or legal concept. It's rarely used in consumer claims, as the focus is almost always on the car's value after it's been fixed. |

In short, while all three types describe a loss, your claim will almost certainly center on Inherent Diminished Value, with a possible additional claim for Repair-Related Diminished Value if the body shop didn't do its job properly.

Inherent Diminished Value: The Stigma of an Accident

Inherent Diminished Value is the most common type of loss and the one that affects nearly everyone. It’s the simple, unavoidable fact that your car is now worth less because it has an accident history tied to its Vehicle Identification Number (VIN).

Think of two identical cars on a dealer lot—same year, same model, same mileage. One has a clean history, and the other was in a collision last year. Even if the repairs on the second car are flawless, which one will a buyer choose? And if they do consider the repaired car, they’re going to expect a steep discount.

That discount is your inherent diminished value. It's like a permanent blemish on your car's record that you can’t wipe away, no matter how good the repairs are. This stigma is what drives the vast majority of diminished value claims because it represents a very real financial hit you take when you go to sell or trade in your vehicle.

Repair-Related Diminished Value: When the Fix Is Flawed

Next up is Repair-Related Diminished Value. This happens when the body shop simply doesn't do a good job, and the quality of the repairs is subpar. This isn't about the accident stigma; it's about shoddy workmanship that leaves your car in worse shape than it should be.

This adds insult to injury. Not only was your car damaged, but the attempt to fix it introduced new problems.

Here are a few classic examples that cause this type of value loss:

- Mismatched Paint: The new paint is a slightly different shade, making the repaired area stick out like a sore thumb.

- Uneven Panel Gaps: The hood, doors, or trunk don't line up correctly, signaling that the frame might not be perfectly straight.

- Aftermarket Parts: The shop used cheaper, non-original parts (non-OEM) that don't fit or function as well as the factory ones.

- Lingering Mechanical Gremlins: You get the car back, and now it pulls to one side or makes a weird noise that wasn't there before.

Any decent appraiser or educated buyer will spot these flaws from a mile away, giving them every reason to lowball you on an offer or just walk away completely.

Immediate Diminished Value: The Pre-Repair Loss

Finally, there’s Immediate Diminished Value. This is a more theoretical concept you probably won't use, but it's good to know it exists. It measures the loss in your car's value the moment after the crash but before a single repair has been made.

Basically, it's the difference between your car's pre-accident value and what it's worth as a heap of twisted metal. Insurance companies and courts sometimes use this as a starting point, but for your purposes, the focus should be on the value lost after the repairs are finished. That's where the real, recoverable money is.

First Party vs. Third Party Claims

When it comes to filing a diminished value claim, you’ll hit a critical fork in the road right away. The path you take depends entirely on a single question: who are you filing the claim against? This distinction between a first-party and a third-party claim is one of the most important concepts in diminished value law, and it’s where many drivers make a wrong turn that stops them dead in their tracks.

Simply put, a first-party claim is filed against your own insurance company, usually under your collision coverage. A third-party claim, on the other hand, is filed against the at-fault driver's insurance company. For diminished value, this difference is everything.

Why Your Own Insurer Will Likely Deny Your Claim

In nearly every state, Oregon and Washington included, your own auto insurance policy is almost certainly written to exclude diminished value. It's not a loophole; it's just how the contract is written.

Your policy is a promise to pay for the "repair or replacement" of your damaged car. Insurers—and the courts—interpret this language very literally. Their obligation is to restore your vehicle's physical condition, not its market value.

The Key Takeaway: Think of it this way: your insurance policy promises to fix the dents, not to erase the accident history that now hurts your car's resale price. This is why filing a first-party diminished value claim is almost always a dead end.

This also explains why you can't claim diminished value if you were the one at fault in the accident. Your only option is to use your own collision coverage, which, as we've seen, won't cover this particular type of loss.

The Power of a Third Party Claim

Everything changes when the other driver is at fault. In that situation, you aren't limited by the terms of your own insurance contract. Instead, you're making a claim against the at-fault driver's liability insurance. Their policy is specifically designed to pay for all the damages their insured driver caused, and that includes the drop in your car’s value.

This is where the law is on your side. You have a legal right to be "made whole"—to be put back in the same financial position you were in moments before the crash. Because their driver caused your car to lose value, their insurance company is on the hook to pay for it.

This is why diminished value is almost exclusively a third-party claim. It has nothing to do with what your policy covers and everything to do with their legal duty to cover the full scope of the damage their driver caused. While diminished value is about property, the principles often overlap with those found in personal injury law, especially when sorting out first-party versus third-party responsibilities after an accident.

Insurers Face Consequences for Ignoring Valid Claims

Insurance companies are well aware of their obligation to pay valid third-party diminished value claims. Still, they often deny or lowball them, banking on the hope that you'll just get frustrated and give up. But when people know their rights, that strategy can backfire—big time.

Look no further than a major class-action lawsuit filed right here in Washington against State Farm. A group of accident victims banded together, accusing the insurance giant of systematically underpaying diminished value claims on repairs over $1,000. State Farm lost and was hit with a $2.09 million settlement. The outcome? Eligible drivers each received a check for $550—real compensation for the value their cars had lost.

This case is a powerful reminder that diminished value isn't some made-up concept. It's a real, legally recognized financial loss. More importantly, it shows that when insurers ignore their duty to pay what's fair, they can be held accountable. For you, it highlights just how crucial it is to understand your rights and fight for the full amount you're owed.

How to Build an Ironclad Diminished Value Claim

Knowing your car lost value after an accident is one thing. Proving it to an insurance company is another challenge entirely. When you file a diminished value claim, the burden of proof is on you, and you need to build a case so solid that the at-fault driver's insurer has no choice but to pay what you're rightfully owed.

This isn’t about your gut feeling; it’s about concrete evidence. Building a compelling case means systematically gathering the right documents, understanding the insurance company's playbook, and presenting your loss in a language they can't simply dismiss. Success comes from being organized and proactive right from the start.

To get started on the right foot, it helps to understand the specifics of your state's laws, like how to file a diminished value claim in Oregon.

Start with Foundational Documentation

Before you can even begin to calculate the loss, you need to collect all the paperwork from the accident and the subsequent repairs. Think of yourself as a detective building a case file—every single document adds another layer of proof that validates your claim.

Your evidence checklist should absolutely include:

- The Police Report: This is your foundational document. It officially establishes that the other driver was at fault, which is the cornerstone of any third-party claim.

- Photos and Videos: Gather any pictures you took at the accident scene showing the initial damage, and be sure to take more photos after the repairs are done.

- The Body Shop's Final Invoice: This document is critical. It gives a line-by-line breakdown of every part replaced and every hour of labor, proving the true severity of the collision.

- Proof of Your Vehicle's Pre-Accident Value: This could be the original bill of sale or market data from trusted sources like Kelley Blue Book or NADA Guides.

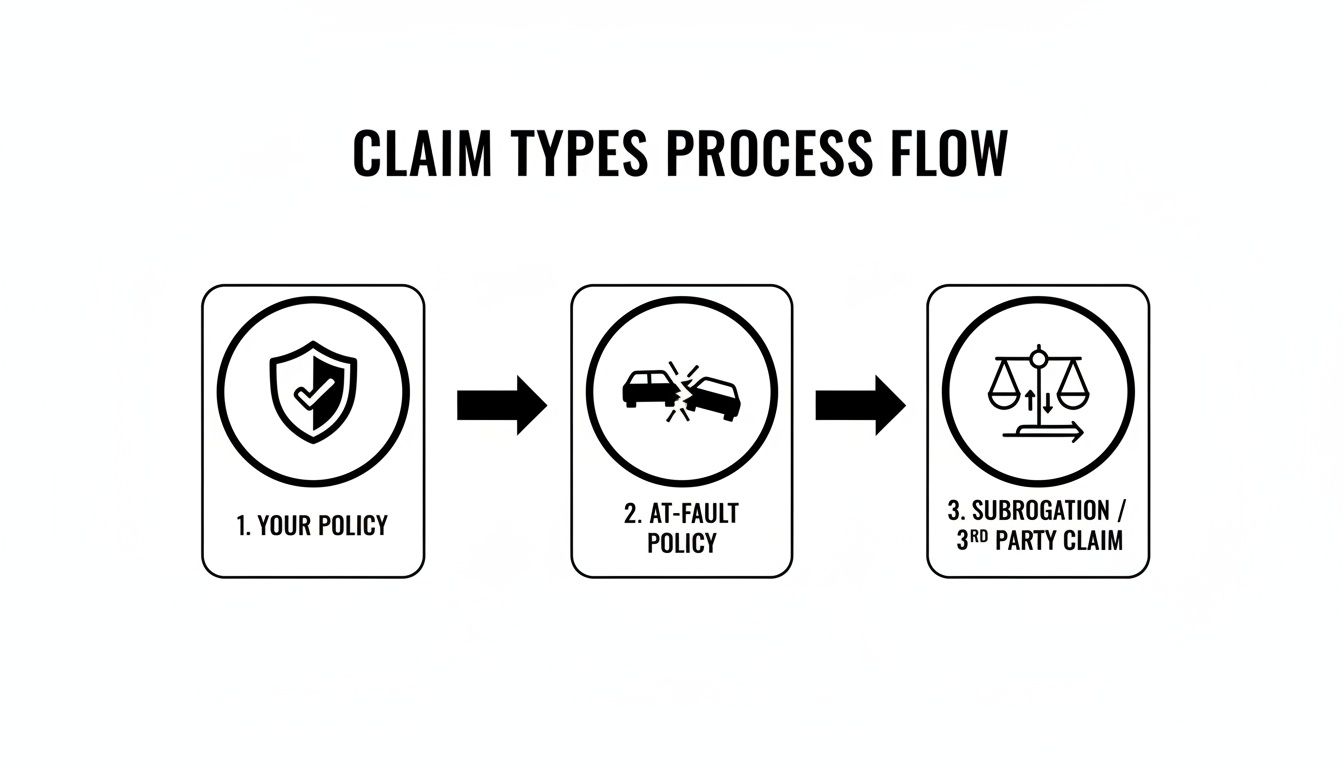

The claims process can get a little confusing, but this flowchart breaks down how the different insurance policies come into play.

As you can see, a diminished value claim is almost always a third-party action you take against the at-fault driver's insurance policy.

Reject the Insurer's Formula: The Problem with 17c

Here’s something to watch out for: the insurance adjuster will often try to "help" you by calculating your diminished value for you. They’ll likely present a formal-looking worksheet, making it seem like an objective, standard assessment. In reality, they're almost always using a flawed, insurer-friendly shortcut known as the 17c formula.

The 17c formula was created by an insurer, for insurers. It is not a law or a standard, but a tool designed to minimize payouts by applying arbitrary multipliers for damage and mileage, systematically undervaluing your true loss.

This formula came out of a single court case and is notoriously simplistic. It starts with just 10% of your car's pre-accident value and then applies harsh, arbitrary deductions for the severity of the damage and your vehicle’s mileage.

For example, a car worth $30,000 might start with a base loss of only $3,000, which is then slashed even further. This often results in a ridiculously low offer that’s just a fraction of your actual loss. The formula completely ignores real-world market data, which is exactly why one driver saw their claim jump from a paltry $417 to $6,000 once they rejected the insurer's math and got a real, independent appraisal.

The Certified Appraisal: Your Most Powerful Tool

The single most important document you can have in your corner is a certified diminished value appraisal from an independent, accredited expert. This is the only piece of evidence that can effectively shut down the insurance company's lowball tactics and truly stand up to scrutiny.

A professional appraisal isn't just someone's opinion; it’s a detailed, defensible report based on:

- Market Analysis: The appraiser conducts a deep dive, comparing your repaired vehicle to identical models currently for sale—both with and without accident histories.

- Expert Inspection: They will physically inspect the quality of the repairs, looking for any lingering issues that might not be obvious to the untrained eye.

- USPAP Compliance: A credible report is built on the Uniform Standards of Professional Appraisal Practice (USPAP), the same rigorous standards used for real estate and other high-value assets.

When you present a USPAP-compliant report from a certified appraiser, you completely change the conversation. It forces the adjuster to set aside their self-serving formula and confront an objective, data-driven analysis of your car's actual lost value in the current market.

Wondering what your vehicle's loss might be? You can use our diminished value claim calculator for a preliminary estimate.

Using the Appraisal Clause as Your Secret Weapon

When an insurance adjuster slides a settlement offer across the table that feels like a slap in the face, it's easy to feel cornered. Most people think their only options are to begrudgingly accept the lowball number or prepare for a draining, uphill battle.

But what if I told you there's another way? Tucked away in the fine print of your auto insurance policy is a powerful, often-overlooked tool that can completely level the playing field: the Appraisal Clause.

Think of the Appraisal Clause as a contractual escape hatch from a bad negotiation. It’s your right, written into the policy, to force an impartial valuation process when you and the insurer are at a standstill over the true value of your loss. Invoking this clause is the single best way to break through an adjuster's biased assessment.

When you trigger this process, you take the power out of the hands of the claims adjuster and their profit-driven software. The conversation moves from their home court to neutral ground, where the focus is on real-world market data and expert analysis, not a company-friendly formula designed to pay you as little as possible.

How the Appraisal Clause Works

The process itself is surprisingly straightforward, but it does require you to be decisive. This isn't just another round of casual negotiation; it's a formal procedure baked into your insurance contract. Once you invoke it, both you and your insurer are obligated to follow the steps.

Here’s how it typically unfolds:

- You Invoke the Clause: The first step is to formally notify the insurance company—always in writing—that you are invoking the Appraisal Clause to dispute their valuation of your diminished value.

- You Hire Your Appraiser: Next, you find and hire a competent, independent, and certified auto appraiser to act on your behalf. This expert is your champion, and they will conduct a detailed, thorough analysis of your vehicle’s diminished value.

- The Insurer Hires Their Appraiser: Once you’ve hired your expert, the insurance company is required to hire its own independent appraiser to represent its position.

- The Appraisers Negotiate: With experts on both sides, the two appraisers get to work. They present their findings to each other and work to reach an agreement on the actual amount of your loss.

This structured process is what levels the playing field. It forces the insurer to stop stonewalling and engage with a professional who is working for you, backed by the same standards and data they claim to respect. To see this process broken down even further, check out our in-depth guide on auto insurance appraisals.

What Happens If the Appraisers Disagree?

Most of the time, two competent appraisers can hash out a fair settlement. Their job is to resolve the dispute based on facts and professional ethics, not to "win" for their side. But what happens if they just can't see eye to eye?

The Appraisal Clause has a built-in tie-breaker for this very situation.

If the two appraisers hit a roadblock and can't agree, they will mutually select a third, impartial expert known as an umpire. The umpire acts as a neutral referee, reviewing the evidence and analysis from both sides. A final, binding decision is reached when any two of the three parties—your appraiser, their appraiser, or the umpire—agree on the value.

This three-person panel guarantees a final resolution, preventing your claim from getting stuck in limbo forever. It's a remarkably effective system for achieving a fair outcome without ever setting foot in a courtroom.

Why This Is Your Best Path Forward

Invoking the Appraisal Clause is a serious strategic move. It sends a clear message to the insurance company that you understand your rights under diminished value law and won't be pushed around by their initial low offer. It shows them you have the evidence—and the expert—to prove your case.

This process strips the emotion and frustration out of the fight. It turns a heated argument into a methodical, evidence-based proceeding led by qualified professionals. By using the tool they put in your policy, you aren't just asking for more money. You are demanding the fair process they contractually owe you.

Without a doubt, it's the most effective way to take back control and secure the full compensation you are legally entitled to.

Your Next Steps to Recover What You Are Owed

Alright, you've learned the basics of diminished value law. Now, let's turn that knowledge into action. Think of this as your game plan for getting back the money you're rightfully owed after an accident. The insurance company has their process, but you don't have to just accept what they offer.

The key is to build your case before you even think about settling. The burden of proof is on you, and a well-organized file is your best weapon against a lowball offer.

Confirm You Have a Valid Claim

First things first, let's make sure you're on the right track. The most important hurdle to clear is having a valid third-party claim. In plain English, that means the other driver was at fault, and you're filing against their insurance, not your own.

This is a critical distinction. Diminished value is almost always recovered from the at-fault party's insurer. If the accident was your fault, your own policy is designed to pay for the repairs, but it won't cover the drop in your car's market value. Nailing this down from the start saves you from chasing a dead end.

Build Your Evidence File

Next up, it’s time to play detective. Gather every single piece of documentation related to the accident and the subsequent repairs. Your claim is only as strong as the evidence you can show.

Here’s a simple checklist of what you'll need:

- The Official Police Report: This is your proof of who was at fault, which is the legal bedrock of your claim.

- The Final Repair Invoice: You need the itemized bill showing exactly what was fixed. This proves the extent and seriousness of the damage.

- Photos and Videos: Gather any pictures you have from the accident scene and take new, detailed photos of the finished repairs.

- Your Vehicle's Title and Registration: These prove you own the car and confirm its specific details.

Get all of these documents organized in one place. It will make the entire process feel less chaotic and show the adjuster you mean business.

The biggest mistake people make is taking the insurance company’s first offer without a fight. This is a negotiation, and showing up with a folder full of proof is your single greatest advantage.

Hire a Certified Appraiser

This is, without a doubt, the most important step. Don't fall for the insurance company's valuation or their flawed "17c" formula. The only way to prove what your car is truly worth now is with a certified, independent appraisal.

A professional appraiser will give you a detailed report that holds up under scrutiny because it follows established industry standards. This report elevates your claim from just your opinion to a data-driven, expert assessment of your financial loss. It’s the tool that forces the insurer to the negotiating table.

Finally, don't drag your feet. Every state has a statute of limitations for property damage claims, which is a hard deadline for taking legal action. In Washington, you have three years from the date of the accident; in Oregon, you have six years. The sooner you start, the better.

Once you have your appraisal report in hand, you’re ready to send a formal demand. To make sure you get it right, check out our guide on writing an effective insurance demand letter that gets results.

Your Diminished Value Questions, Answered

After a car accident, the legal and insurance details can feel overwhelming. Let's clear up some of the most common questions about diminished value law so you can move forward with a clear understanding of your rights.

Can I File a Diminished Value Claim Through My Own Insurance?

This is probably the most frequent question we get, and it's a critical point of confusion. In almost every situation, the answer is no.

Think of it this way: your own auto insurance policy is a contract. That contract promises to repair your vehicle to its pre-accident condition, but it doesn't promise to restore its pre-accident market value. A diminished value claim is almost exclusively a third-party claim. This means you file it against the insurance company of the driver who was at fault, because their responsibility is to cover all the damages their client caused—and that includes the permanent hit to your car's resale price.

Is It Worth Filing a Claim for an Older Car?

It absolutely can be. It’s easy to assume that only new, low-mileage cars lose significant value, but that’s not always the case. While a newer car might see a larger drop in raw dollars, the loss is all relative to the vehicle's pre-accident worth.

A well-kept older vehicle, a classic car, or even a popular model known for holding its value can still lose thousands on the open market after a major collision.

The only way to know for sure is to get a professional assessment. An expert appraiser can determine the real-world market impact, regardless of the vehicle's age.

What If My Car Was Leased When It Was Damaged?

You can, and you definitely should, still pursue a claim. When your lease is up, the leasing company will assess the vehicle for any "excess wear and tear." A documented accident history on the vehicle's record is a huge red flag for them, and it will almost certainly lead to hefty charges.

A successful diminished value claim gives you the funds to cover those end-of-lease penalties. It ensures you’re not left paying out-of-pocket for the other driver's mistake when you turn the car in.

Navigating a diminished value or total loss claim can be challenging, but you don't have to do it alone. The certified experts at Total Loss Northwest fight to get you the fair settlement you deserve. We use data-driven, USPAP-compliant appraisals to prove your vehicle's true value, ensuring you recover what you're rightfully owed. Get the professional help you need by visiting the Total Loss Northwest website.