You get the call. The adjuster says your car is a total loss. For a moment, you think the hard part is over because you had insurance, you made your payments, and this should be straightforward.

Then the numbers show up.

The insurer values the vehicle lower than you expected. Your lender still wants the full payoff. You start hearing the phrase gap insurance total loss, and now you're trying to figure out whether gap insurance will save you, whether you still owe money, and why the settlement feels wrong in the first place.

That confusion is normal. The part most drivers miss is this: gap insurance is not the main lever. It's a cleanup tool. It exists because the primary insurer pays actual cash value, not your loan balance. If that value is too low, the damage isn't limited to the loan shortfall. A bad valuation can reduce your payout and increase what gap has to absorb.

If you're dealing with a financed or leased vehicle after a wreck, don't just ask whether you have gap coverage. Ask whether the insurer got your ACV right. That's where real money is won or lost.

The Shocking Phone Call After a Total Loss

A lot of drivers have the same first reaction after the adjuster calls. Relief. The vehicle is wrecked, you're dealing with the crash, and at least the claim is moving.

Then the offer lands, and relief turns into anger.

You look at the settlement and realize the insurer isn't paying what you paid for the car. They aren't paying what it would cost to replace it with one you want to drive. They're paying what they say the vehicle was worth immediately before the loss. If you financed the vehicle on a long term, rolled in extras, or bought when prices were high, that number may sit well below what you still owe.

That's negative equity. It means the loan balance is higher than the vehicle's market value. In a total loss, that gap becomes real fast.

Why this hits so hard

The problem isn't just math. It's timing.

You still need transportation. You may still owe the lender. The insurer is talking in valuation language. The lender is talking in payoff language. And nobody is focused on your actual financial position.

Most drivers think total loss means the loan disappears with the car. It doesn't.

That disconnect is where gap insurance enters the conversation. It's supposed to help when the lender payoff is higher than the insurer's settlement. But a lot of people stop thinking there, and that's a mistake.

The trap most people walk into

Drivers often focus on one question only: "Will gap cover the difference?"

That's the wrong first question.

The better question is: "Why is the insurer's value where it is?" If the carrier starts from a weak ACV number, everything that follows gets worse. Your primary payout drops. Your gap exposure grows. Your out-of-pocket risk may still remain.

If your car was clean, low-mileage, well-maintained, hard to comp, or modified, you should assume nothing. Review the valuation before you accept the settlement.

What Gap Insurance Actually Covers

Gap insurance is a financial bridge. It doesn't replace your car. It doesn't pay sentimental value. It doesn't erase every cost tied to the loan. It fills one narrow space: the difference between what the primary insurer pays on a totaled vehicle and what you still owe on the loan or lease.

The bridge between value and debt

Here's the basic structure.

Your auto insurer determines the vehicle's Actual Cash Value, usually called ACV. That's the amount they believe the car was worth right before the crash. The lender, meanwhile, cares about the remaining payoff on the loan or lease. If the payoff is higher than the ACV settlement, the difference is the gap.

If you want a plain-language primer on policy scope, this breakdown of what gap insurance does and doesn't cover is worth reading alongside your own paperwork.

Why this product became common

Gap insurance didn't become common by accident. It became more prominent as finance terms stretched out and borrowers stayed upside down longer. One industry analysis says GAP losses rose above historical norms before the Great Recession, fell when lending tightened, and returned to similar levels starting around 2014 as looser lending and longer loan terms expanded negative-equity exposure. The same report says the global GAP insurance market was over USD 3.9 billion in 2023 and projects about USD 7.5 billion by 2032, reflecting a 7% CAGR from 2024 to 2032 (industry analysis on GAP loss ratios and market growth).

That matters because it tells you this isn't some rare add-on. It's a response to a financing system that often leaves borrowers underwater.

What gap insurance total loss does not mean

A lot of people hear "gap insurance total loss" and assume the product makes them whole. It doesn't.

It addresses the shortfall tied to the loan balance after the primary claim settles. This coverage is straightforward. It is not a replacement-cost policy. It is not a valuation correction tool. It is not a check that wipes out every bad financial decision layered into the loan.

Practical rule: Gap insurance helps with debt exposure. It does not fix a bad ACV settlement.

That's why I tell clients to stop treating gap insurance like the finish line. It's one part of the claim. The ACV number is still the foundation.

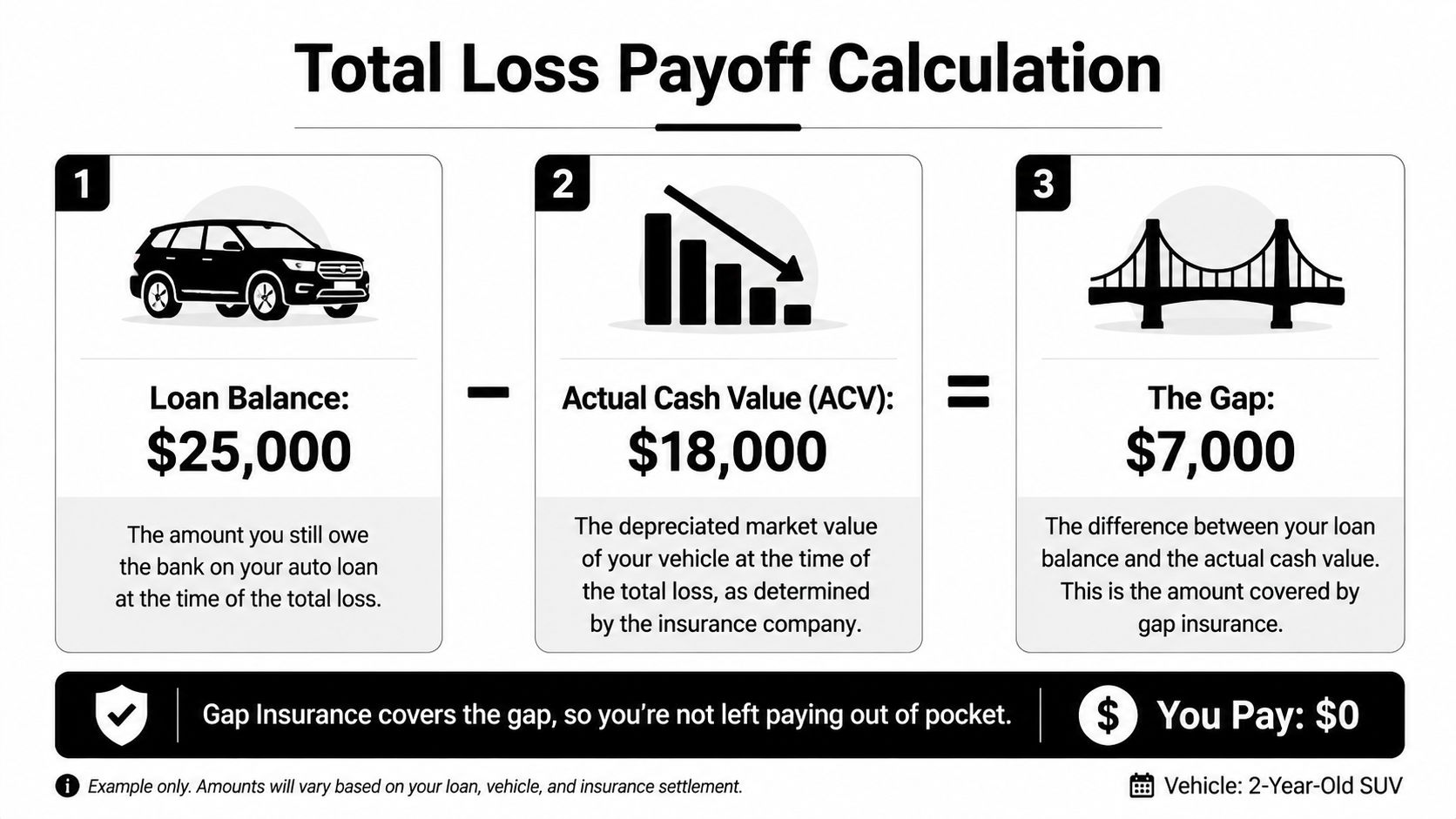

A Real-World Total Loss Payoff Calculation

Most drivers don't need more theory. They need the math.

A vehicle is often declared a total loss when repair costs hit a threshold such as 75% of the car's ACV, and in that situation the insurer typically pays the vehicle's actual cash value minus the deductible rather than the repair bill, as explained in this discussion of how GAP works after a total loss in Virginia.

Start with the numbers that matter

Use this sample:

| Item | Amount |

|---|---|

| Loan balance | $25,000 |

| Insurer ACV | $18,000 |

| Gap before deductible | $7,000 |

Those figures are a simple example of how the shortfall forms. Now layer in the actual claim process.

How the settlement usually flows

The primary insurer doesn't care what you borrowed. It values the car. Then it applies your collision terms. If your deductible applies, that amount gets subtracted from the total-loss settlement before the lender payoff issue is even addressed.

That means the sequence looks like this:

- The vehicle is declared a total loss

- The insurer calculates ACV

- The deductible is subtracted if applicable

- The lienholder gets paid from that settlement

- Gap coverage, if you have it, addresses the remaining shortfall under its own terms

This is why owners get blindsided. They focus on the loan, but the claim starts with valuation.

Where the pain shows up

Let's keep using the sample figures from the infographic.

If the lender payoff is $25,000 and the insurer values the vehicle at $18,000, you're already looking at a $7,000 gap before you even ask what the gap contract excludes.

Now think about what happens if the insurer undervalues the ACV. The shortfall grows. Not because you borrowed more overnight, but because the carrier started from a lower number.

The settlement problem in many gap insurance total loss claims isn't the loan balance. It's the ACV used to compare against it.

The claim math in one snapshot

Here is the simplest way to view it:

- Primary auto insurance pays: the ACV, subject to the policy's deductible

- Lender expects: the current payoff amount

- Gap insurance may pay: the remaining covered difference

- You may still owe: any excluded items, deductible impact, or amounts above policy limits

If you're trying to evaluate your own claim, don't just ask for the total offer. Ask for the valuation report, the condition adjustments, the comparable vehicles, and the payoff statement. Without those documents, you're not reviewing the claim. You're just reacting to it.

Navigating the Gap Insurance Claim Process

Once the total loss decision is made, don't sit back and wait for everyone else to coordinate. They won't do it well enough. You need to move the file.

If you need a practical overview of what happens to the financing side after a wreck, this guide on what happens if you total a financed car gives a helpful borrower-level summary.

The right order matters

A lot of claim delays happen because drivers contact the gap provider first and assume that starts the process. Usually it doesn't. The primary insurer has to settle the total loss before the gap side can calculate the shortfall.

Use this order:

Open and push the primary auto claim

Get the total-loss decision in writing and request the valuation documents.Call the lender or leasing company

Ask for a current payoff letter. You need the exact payoff, not a rough balance from your app.Contact the gap provider

Ask what documents they require and where to send them.

The paperwork you should gather

Claims get stuck over missing documents more than anything else. Pull these together early:

- Settlement paperwork that shows the insurer's ACV and any deductible applied

- Payoff letter from the lender or lessor

- Gap contract or declarations page showing you have coverage

- Accident-related documents such as the police report, if requested

- Loan paperwork if the gap administrator wants to verify financed items

Keep every email. Save PDFs. Get names and direct extensions.

What to ask before you submit anything

Don't send forms blindly. Ask these questions first:

- What exact balance do you use for the payoff review?

- What items are excluded from reimbursement?

- Do you need the lender paid first before gap is processed?

- Will you send payment to the lender or to me?

A lot of confusion clears up once those answers are in writing.

For a simple explainer on how the process tends to unfold, this video is useful:

Don't let the file drift

Gap claims often stall when the insurer, lender, and gap administrator each say they're waiting on someone else. Fix that by making yourself the record keeper.

Send one short follow-up email after every phone call. Confirm who owes what document and by when.

That's boring work, but it prevents weeks of delay.

Common Exclusions and Policy Limits

Many drivers discover at this point that they purchased less protection than they expected.

A gap insurance claim is typically triggered only when the vehicle is a total loss and the loan or lease balance exceeds the insurer's ACV settlement, but coverage often excludes add-ons such as finance charges or extended warranty costs, which can shrink the reimbursable gap, as explained in Progressive's summary of how gap insurance claims work.

Gap doesn't cover every dollar on the contract

People tend to assume the lender payoff and the gap reimbursement are the same number. They often aren't.

The financed contract may include items that the gap provider won't pay. That means you can still be left with a balance even though you had gap coverage and filed the claim correctly.

Common problem areas include:

- Finance charges that were part of the loan but not covered by the gap agreement

- Service contracts or extended warranties rolled into the financing

- Other add-ons bundled at the dealership and treated separately by the policy terms

Deductibles and other surprises

Many drivers also learn, too late, that the deductible on the primary policy can still hurt them. The primary insurer settles under the auto policy first. If that settlement is reduced, the remaining exposure doesn't magically disappear.

Read the actual contract language. Don't rely on what you were told in the finance office.

| Common expectation | What often happens |

|---|---|

| Gap pays everything left on the loan | Gap pays only the covered shortfall |

| Rolled-in products are part of the balance, so they must be covered | Contract terms may exclude them |

| The deductible won't matter much | The deductible can reduce the base settlement |

Why borrowers feel cheated

The problem isn't always bad faith. A lot of it is bad understanding.

Dealers, lenders, insurers, and gap administrators all talk about the product differently. By the time you file a claim, you're comparing one sales conversation against several contracts written in narrow language.

That said, some exclusions are broad enough to leave a driver with an unpleasant surprise even after paying for the coverage. That's why I tell people not to ask "Do I have gap?" Ask, "What exactly does my gap agreement exclude?"

If you haven't read the contract yourself, you don't know the answer.

When the Insurer's Settlement Offer Is Too Low

This is the part most gap insurance articles miss, and it's the part that matters most.

Gap coverage only applies after the primary insurer sets the ACV. If that ACV is too low, the damage is already done. One insurance source puts it plainly: the actual issue in many claims is not the loan balance, but the starting valuation number, because a lowball ACV is still a financial loss to the owner even if gap addresses part of the deficiency (why low ACV matters more than most gap guides admit).

Why the ACV is the real battleground

To put it plainly, gap insurance serves as a temporary fix for negative equity.

If the insurer undervalues your car, gap may protect the lender relationship, but it doesn't mean you received a fair vehicle valuation. That's especially important if your vehicle was unusually clean, had low mileage, desirable options, recent work, or features that generic valuation software doesn't treat well.

A low ACV can hurt you in several ways:

- It cuts the primary settlement

- It increases the gap shortfall

- It may leave excluded amounts still unpaid

- It affects your ability to move into a replacement vehicle

Who should be most skeptical of the first offer

You should review the valuation closely if your vehicle falls into any of these categories:

- Higher-value models where small comp errors change the number fast

- Customized vehicles with aftermarket parts or upgrades

- Lightly driven cars that don't compare well to average market examples

- Exceptionally clean vehicles where condition adjustments are too weak

If you're trying to understand your broader legal options after accepting or considering an insurance payment, this piece on personal injury claim advice for accident victims can help you think through the claims side beyond property damage alone.

What to review before you argue with the adjuster

Don't call and say the offer feels low. That's not evidence. Review the data.

Use a checklist:

Comparable vehicles Are the comps similar in trim, mileage, condition, and options?

Condition ratings

Did the report understate pre-loss condition?Mileage adjustments

Were they applied correctly?Options and packages

Did the valuation include the equipment your vehicle had?

For a practical reference point, this guide on how to calculate fair market value is useful when you're checking whether the carrier's ACV logic holds up.

If the ACV is wrong, the entire total-loss settlement is built on a bad foundation.

That is why I push clients to focus on valuation first and gap second.

How to Maximize Your Total Loss Settlement

You don't maximize a total loss claim by arguing harder. You maximize it by bringing better valuation evidence.

Actuarial commentary on GAP notes that a low ACV settlement directly increases gap exposure and that independent valuation evidence can materially reduce the residual balance that GAP must cover. The same commentary also notes state-sensitive refund rules, which is another reason the underlying value work matters (actuarial discussion of GAP valuation, rate adequacy, and refunds).

The strongest move most drivers never use

Most auto policies include an Appraisal Clause or similar dispute mechanism for valuation fights. That's the pressure point.

When the insurer's number doesn't reflect the true market, you can use an independent appraiser to build a supported ACV based on the actual vehicle, actual comparables, and documented condition. That changes the conversation from opinion to evidence.

What an independent appraiser actually does

A qualified appraiser should review:

- Vehicle specifics including trim, options, mileage, and condition

- Comparable market data that fits the actual car, not a generic substitute

- Valuation errors in the insurer's report

- Support for an appraisal-clause dispute if the policy allows it

One available option is Total Loss Northwest, which performs independent total-loss appraisals and appraisal-clause support for disputed vehicle values. That's relevant when the ACV itself is the problem, not just the financing shortfall.

The result you're aiming for

The goal isn't to "win" an argument with the adjuster. The goal is to force the claim onto accurate numbers.

If the ACV goes up, several things can improve at once:

- The primary settlement may rise

- The gap claim may shrink

- Your out-of-pocket exposure may drop

- You may be in a much better position to replace the vehicle without carrying old debt into a new loan

This is the part drivers need to understand. Gap insurance total loss coverage can keep a bad loan from getting worse. A fair ACV can stop the loss from spreading in the first place.

If the insurer declared your vehicle a total loss and the offer looks wrong, get the valuation reviewed before you sign anything. Total Loss Northwest provides independent total-loss appraisals and appraisal-clause support for vehicle owners who need evidence to challenge a low ACV settlement.