You open the claim letter, scroll to the number, and your stomach drops. Your insurer has declared the vehicle a total loss, but the settlement figure doesn't match what it would take to replace your car in the Pacific Northwest market. If you drive a clean Subaru in Portland, a low-mile truck in Spokane, or a customized vehicle with documented upgrades, that gap can feel personal fast.

Most drivers make the same first assumption. They think the carrier's number is final unless they hire a lawyer or accept a long fight. In many auto claims, that isn't true. Your policy may contain an appraisal clause, and that clause can give you a structured way to challenge a low valuation without turning the dispute into a full lawsuit.

That matters most in total loss and diminished value claims, where the insurer often leans heavily on valuation software and standardized adjustments. Software can be useful. It can also flatten the details that determine market value in Oregon and Washington, especially for higher-trim vehicles, older clean examples, and cars with unusual demand in local markets.

The insurance appraisal process isn't magic, and it isn't right for every dispute. But when the disagreement is about what the vehicle is worth, it can shift the conversation from “take our number or leave it” to “show the evidence.” That's a much better place to be.

That Lowball Offer Is Not the Final Word

A common call goes like this: the insurer says the vehicle is a total loss, sends over a valuation report, and the owner notices the comparable vehicles don't really compare. Wrong trim. Higher mileage. Different condition. Missing options. Listings from markets that don't reflect what cars sell for in Seattle, Tacoma, Eugene, or Bend.

The owner pushes back and gets a familiar response. “That's what our system produced.”

That answer sounds official, but it doesn't end the discussion. In auto claims, especially total loss and diminished value matters, the first number is often just the insurer's starting position. If the dispute is about value, the policy may let either side invoke appraisal and move the disagreement into a defined process.

What that looks like in real life

Say your SUV was well maintained, had documented service history, newer tires, and a trim package buyers actively look for in the Northwest. The carrier's valuation might still treat it like an average unit. That's where owners get trapped. They argue emotionally about fairness when the better move is to shift into evidence and procedure.

The insurance appraisal process gives you that lane.

Low offers feel final because they arrive on company letterhead. They aren't final just because they're printed neatly.

For overwhelmed drivers, the biggest change is mental. Stop treating the first offer as a verdict. Treat it as a valuation you may be able to challenge.

Why drivers lose ground early

Individuals often wait too long, send unsupported emails, or argue the wrong issue. They say the offer is “ridiculous” but don't show market support. Or they demand appraisal when the insurer is disputing coverage, which is a different problem entirely.

What works better is simpler:

- Read the policy language: Find the appraisal clause and confirm the dispute is about value.

- Preserve your records: Keep the valuation report, photos, maintenance records, receipts, and any comparable listings.

- Get independent help when needed: A vehicle value dispute is technical. It's usually won with documentation, not outrage.

If your insurer undervalued the car, you may have more advantage than you think. The next step is knowing exactly what the insurance appraisal process is, and just as important, what it is not.

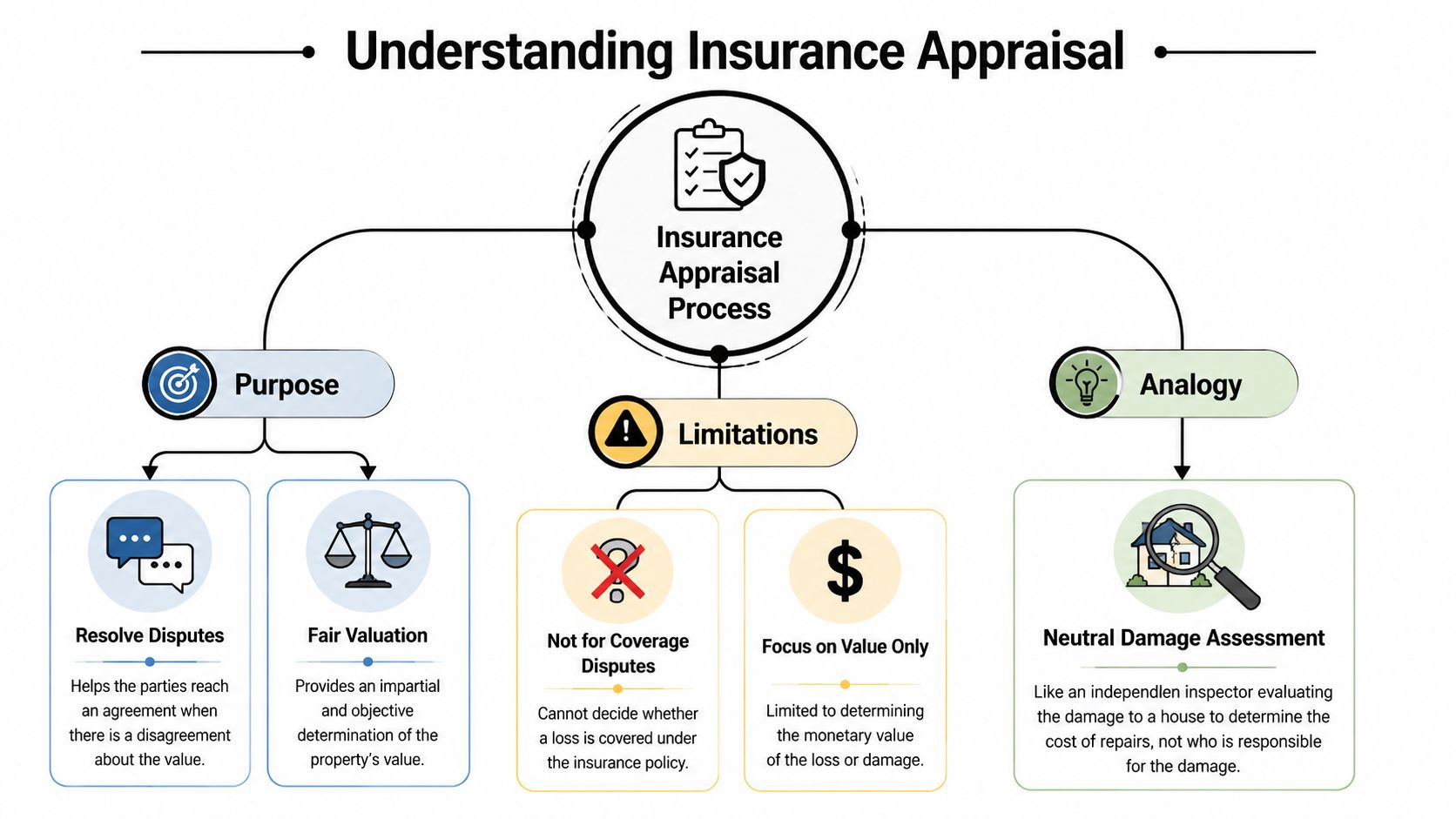

What Is the Insurance Appraisal Process

The easiest way to understand the insurance appraisal process is to think of it as a price referee built into the policy. It exists for one job only. It resolves a disagreement over the amount of loss.

In auto claims, that usually means a fight over the vehicle's actual cash value in a total loss claim, or the amount of post-repair value loss in a diminished value claim. It is not a general-purpose tool for every claim dispute.

What appraisal does

When the insurer and policyholder both agree there's a covered loss but disagree on the dollar amount, appraisal can move the dispute out of ordinary back-and-forth claims handling. Each side selects an appraiser, and those appraisers try to reach an agreed value. If they can't, an umpire may decide the issue.

That's the practical use. It narrows the argument to valuation.

If you want a broader primer on how auto valuation works after a wreck, this guide on what a car appraisal is after an accident is a helpful companion to the policy-driven appraisal process.

What appraisal does not do

At this stage, many drivers burn time and money. A critical misunderstanding is that appraisal resolves coverage disputes. It does not. The process strictly determines the amount of loss only and excludes coverage questions, policy interpretation, or legal liability, as explained in this discussion of the insurance appraisal clause and appraisals.

If the insurer says your damage wasn't caused by the crash, or says the claim is barred by policy language, appraisal won't force payment. It can set a number, but it can't create coverage where the carrier says none exists.

Practical rule: If the real fight is “Is this covered?” appraisal is usually the wrong tool. If the fight is “What is this worth?” appraisal may be exactly the right tool.

That distinction matters in auto claims because carriers sometimes mix the issues. They may discuss value before clearly resolving whether they accept all aspects of the loss. That can confuse owners into thinking a binding value award guarantees a check. It doesn't if coverage remains contested.

Why this matters beyond auto claims

The same amount-of-loss limitation shows up in property insurance more broadly. If you're also comparing how valuation disputes work in other policies, this overview of securing fire insurance for your home is useful background because it helps separate valuation issues from coverage issues in a different insurance context.

For your car claim, keep the purpose narrow. Appraisal is a valuation mechanism. Used correctly, it can be powerful. Used on the wrong dispute, it becomes an expensive detour.

The Parties Involved in Your Appraisal Team

Once appraisal is invoked, three people shape the outcome. Your appraiser. The insurer's appraiser. The umpire.

Those titles sound balanced on paper. In practice, each role carries different incentives, different habits, and different levels of independence. If you understand that early, you make better decisions.

Your appraiser

Your appraiser's job is to develop and defend a credible vehicle valuation. In a total loss claim, that means examining condition, mileage, options, market comps, maintenance history, prior damage history, and local demand. In a diminished value claim, it means showing the measurable market impact of accident history after proper repairs.

A good independent appraiser does more than “argue high.” They build a file that can survive scrutiny. That includes checking whether the insurer's comps are comparable and whether software adjustments make sense for your specific vehicle.

The insurer's appraiser

The insurer's appraiser may be competent and professional. But don't confuse that with neutral. Their role is usually to support the carrier's valuation position within the framework the company uses.

That matters because auto insurers often rely on standardized tools and internal processes. If the underlying report is built around software outputs, the insurer's appraiser may spend most of their effort defending those outputs rather than reworking the valuation from the ground up.

The umpire

The umpire is the tie-breaker. If the two appraisers can't agree, the umpire reviews the dispute points and helps produce a binding result under the policy terms.

The best umpires stay disciplined. They don't rewrite the claim. They focus on the valuation issue presented. In auto claims, though, the umpire's background matters. An umpire who mainly sees property losses may miss the importance of trim-level premiums, enthusiast markets, custom parts, or Pacific Northwest regional pricing patterns.

A simple view of the team

| Role | What they should do | Where problems show up |

|---|---|---|

| Policyholder appraiser | Build independent market support | Thin documentation or weak comps |

| Insurer appraiser | Defend or revise the carrier valuation | Overreliance on software assumptions |

| Umpire | Break deadlock on value | Limited auto-market depth or process shortcuts |

The appraisal clause gives both sides a seat at the table. It does not guarantee both sides bring equal preparation.

That's why hiring an independent appraiser isn't a luxury in a meaningful dispute. It's how you make sure someone is actively testing the insurer's valuation instead of just reacting to it.

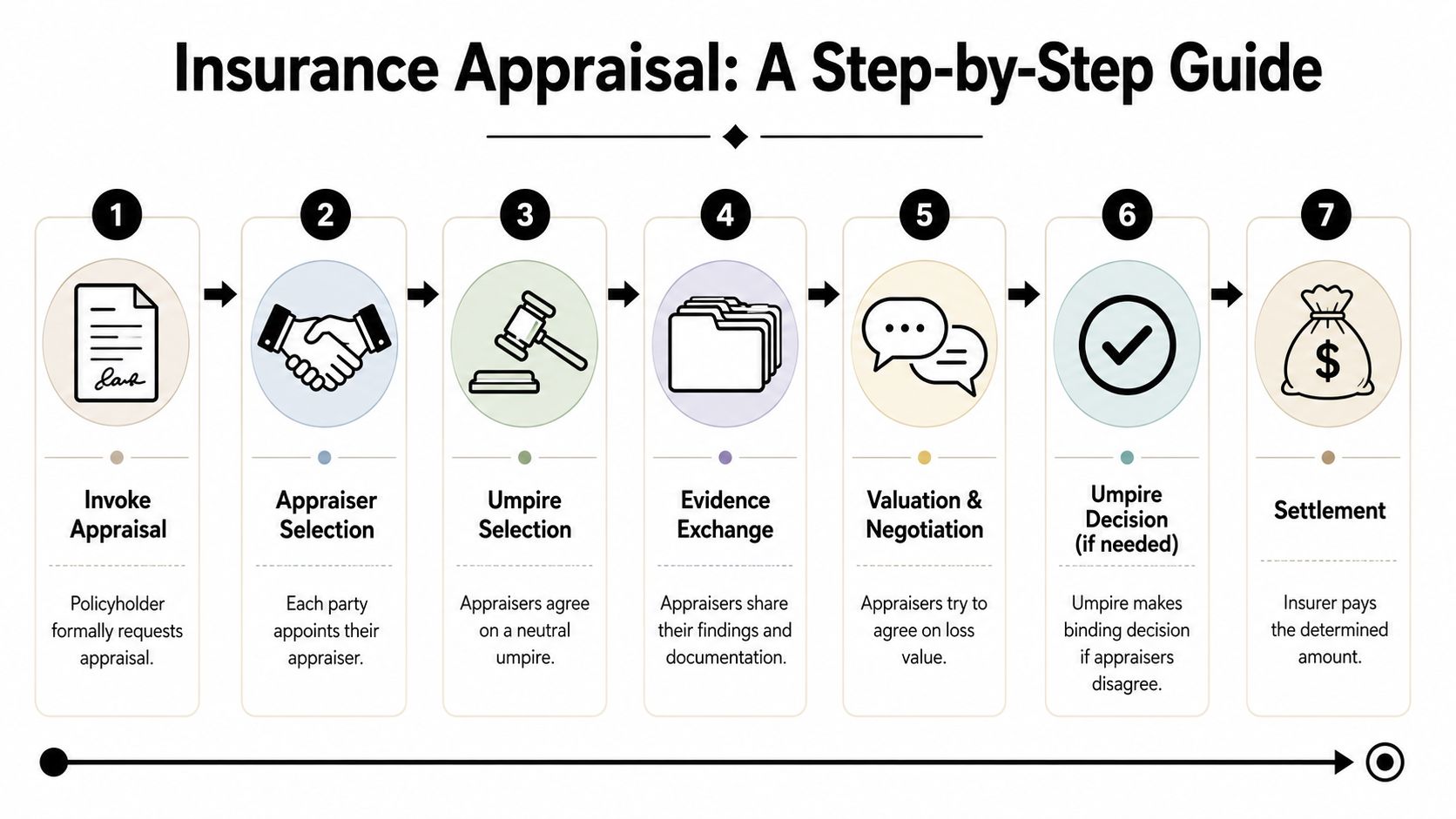

Your Step-by-Step Walkthrough of the Process

The insurance appraisal process feels intimidating until you break it into a sequence. In most policies, the steps are straightforward even if the valuation work inside them is technical.

Start with the policy itself. The clause controls the timeline and the mechanics.

Step one through three

The process begins with a written demand for appraisal. Once that demand is made, each party must select a competent, independent appraiser and notify the other within 20 days, and if the appraisers can't agree on an umpire within 15 days, a judge may be asked to select one. The final award is binding if agreed to by any two of the three parties, as outlined by the Insurance Appraisal and Umpire Association.

That timeline is short. Waiting around usually hurts the policyholder more than the insurer because the carrier already has a valuation system in motion.

If you need a clearer sense of the neutral third-party role, this explanation of the appraisal clause umpire process helps drivers understand what happens when the appraisers reach an impasse.

Here's the practical flow:

Invoke appraisal in writing

Keep it clear and direct. Identify the claim, the policy, and that you're invoking the appraisal clause based on a dispute over value.Name your appraiser promptly

Don't treat this as a clerical step. The appraiser you choose shapes the evidence, the negotiation posture, and the presentation to any umpire.Work out umpire selection if needed

Some appraisers agree on an umpire quickly. Others don't. When that process stalls, the file slows down and costs can rise.

A lot of policyholders now send formal claim documents electronically. If you're handling signatures and records that way, this overview of digital signatures in insurance is useful for keeping your paperwork organized and enforceable.

Step four and five

After the appraisers are appointed, the case usually turns into an evidence contest.

Your appraiser gathers vehicle-specific support, reviews the insurer's valuation report, and identifies weak spots. In a total loss file, that can include bad comparable choices, improper condition adjustments, omitted options, poor local market matching, or unsupported deductions. In a diminished value case, it often comes down to proving market stigma after repair with solid, vehicle-specific analysis.

Then the appraisers negotiate. Sometimes that phase resolves the claim without the umpire ever needing to step in. When both appraisers are serious and the evidence is strong, a negotiated number is often possible.

Keep every document in one place before appraisal starts. The process moves faster when your records are ready before your appraiser asks for them.

Helpful documents often include:

- Vehicle records: Title history, VIN details, factory options, and service documentation

- Condition proof: Pre-loss photos, detailing records, tire receipts, upgrade receipts, and inspection reports

- Market support: Local listings, dealer offers, and examples that reflect your trim, mileage, and condition

Step six and seven

If the appraisers still disagree, the umpire reviews the disputed valuation points. Depending on the case, that may involve written submissions, competing reports, file review, or direct inspection. The policy usually doesn't turn this into a courtroom. It remains a targeted valuation process.

Once any two of the three decision-makers agree, that becomes the award under the appraisal clause.

The financial side also matters. Each party pays their own appraiser, and the umpire expense is typically shared equally under the policy framework described by the IAUA. That cost structure is one reason you want to enter appraisal with a real strategy instead of using it as a pressure tactic.

Where drivers get stuck

The process itself is usually not the hard part. The hard part is choosing the right dispute and bringing the right proof.

Common mistakes include:

- Invoking appraisal too early: The carrier hasn't clearly defined whether the dispute is valuation or coverage.

- Hiring for price instead of skill: A cheap appraiser who submits weak comps can cost far more in the final result.

- Letting deadlines slide: Policy timelines don't wait for your schedule.

- Treating it like customer service: This is not the stage for vague complaints. It's the stage for evidence.

For many drivers, appraisal is the first moment the claim starts to feel manageable. There's a timeline. There are defined roles. There's a path to a decision. Once you understand that path, the next job is building a valuation file strong enough to move the number.

Here's a short visual overview before we get into strategy:

Maximizing Your Settlement with Evidence and Strategy

Most appraisal disputes are not won by the person who feels more wronged. They're won by the side with the cleaner valuation file.

That's especially true in Pacific Northwest total loss claims, where local market differences can be meaningful. A vehicle in Bellingham or Medford may not trade the same way as a similar-looking unit pulled into a broad regional software pool. If the insurer's report treats those vehicles as interchangeable, your job is to prove they aren't.

Counter the software with market proof

Policyholders often underestimate the hidden costs of appraisal, which can total $3,000–$6,000, and umpires in auto claims often default to insurer valuation software such as CCC. One of the most useful countermeasures is independent market data from sources like DealerSalk or KBB, especially for high-value or classic vehicles, as discussed in this piece on the pros and cons of the insurance appraisal process.

That gets to the heart of the strategy. Don't argue abstractly that the software is unfair. Show where it's wrong.

Strong rebuttal material often includes:

- Comparable vehicles that match: Similar trim, drivetrain, mileage band, title status, condition, and equipment

- Ownership documentation: Maintenance history, major recent service, upgrades, accessories, and restoration records where relevant

- Local relevance: Pacific Northwest listings and dealer data when local demand supports a stronger number

- Condition support: Photos taken before the loss, not just after it

What works and what doesn't

A lot of owners send in online listings with no explanation. That rarely moves an appraiser or umpire. The better method is to show why each comp belongs in the analysis and why the insurer's comp does not.

Here's the difference:

| Weak approach | Strong approach |

|---|---|

| “These cars online cost more than your offer.” | “These listings match trim, mileage, drivetrain, and condition more closely than the insurer's selected vehicles.” |

| “My car was in great shape.” | “Here are pre-loss photos, service invoices, tire receipts, and option codes that support above-average condition.” |

| “CCC is always wrong.” | “This report omitted documented options and relied on comparables with materially different equipment and condition.” |

If you can't explain why a comparable belongs in the file, it probably won't carry much weight.

Total loss versus diminished value

The evidence overlaps, but the argument changes.

For a total loss claim, you're proving what the vehicle was worth immediately before the loss. That means actual cash value based on real market support.

For a diminished value claim, you're proving that the repaired vehicle now suffers a market penalty because buyers discount accident history. That analysis needs discipline. Generic formulas don't persuade nearly as well as vehicle-specific market reasoning.

When an independent appraiser adds the most value

An independent appraiser is most useful when the claim involves one or more of these issues:

- High-value vehicles: Luxury, performance, collector, or specialty units

- Documented upgrades: Wheels, suspension, paintwork, accessories, or restoration support

- Scarce local inventory: Vehicles that don't fit broad software assumptions well

- Diminished value disputes: Cases where post-repair stigma needs to be documented carefully

One option in this space is Total Loss Northwest, which handles certified independent appraisals for total loss and diminished value claims in Oregon and Washington and can invoke the appraisal clause on behalf of policyholders. The key point isn't the brand name. It's the service model. You want an appraiser who builds a market-based report rather than merely reacting to the insurer's printout.

What doesn't work is hoping the carrier will self-correct because you're persistent. Sometimes adjusters do revise a file. Often, though, the claim only moves when the evidence becomes too specific to ignore.

State-Specific Rules for Oregon and Washington

In Oregon and Washington, the insurance appraisal process generally follows the same core logic found in many property and auto policies. The fight is over value, each side names an appraiser, and the file can move to an umpire if needed. But local practice still matters.

The biggest practical difference isn't usually a dramatic statute drivers have memorized. It's how claims are handled on the ground. Market data, vehicle availability, weather-related wear assumptions, and regional demand all affect valuation in ways national software may not capture well.

Oregon drivers

In Oregon, I tell drivers to pay close attention to local market substitution. A carrier may use broader geographic comparables that look acceptable on paper but don't reflect what it costs to replace the vehicle where you shop. That issue shows up often with trucks, AWD vehicles, hybrids, and clean older cars that hold demand in certain Oregon markets.

If you're in a total loss dispute, keep your evidence local where possible. Dealer listings, regional comps, and condition records are often more persuasive than broad internet screenshots.

Washington drivers

Washington claims often raise the same valuation issues, but I see more disputes over trim-specific premiums, technology packages, and the market effect of accident history on newer vehicles. For drivers dealing with those issues, this guide to auto appraisal in Washington is worth reviewing because it focuses on how Washington vehicle owners can approach valuation disputes more strategically.

What to do in either state

The practical playbook is similar across both states:

- Read the exact policy language: Don't assume your deadlines or appraisal wording match someone else's policy.

- Build regional support: Use Pacific Northwest market evidence whenever it strengthens the valuation case.

- Choose an auto-focused appraiser: Property-oriented experience doesn't always translate well to vehicle valuation.

- Keep the dispute narrow: If the insurer is really raising coverage issues, don't let the file drift into an appraisal fight that misses the actual problem.

Neither Oregon nor Washington rewards vague disagreement. A clean, locally grounded valuation file usually carries more weight than a long complaint letter.

Frequently Asked Questions About Appraisal

Drivers usually reach this point with the same concerns. Can I do this myself? What if I lose? How long will it drag on? Is it worth paying an appraiser at all?

The short answers depend on the size of the valuation gap, the complexity of the vehicle, and how strong your documentation is.

Can I handle the insurance appraisal process myself

You can try, but most drivers underestimate how technical the dispute becomes once appraisal starts. The issue is no longer “I think the offer is low.” The issue becomes whether you can produce better comparables, support condition adjustments, rebut software assumptions, and present a coherent valuation theory.

If the vehicle is ordinary and the gap is small, self-advocacy may be enough. If it's a high-value car, a specialty vehicle, a truck with real local demand, or a diminished value claim, going without an appraiser can leave you badly outgunned.

What if I disagree with the final award

That's one of the hardest parts of appraisal. The process is designed to produce a binding valuation result under the policy once the required agreement is reached. That means you should treat the pre-award stage as the critical battleground.

If the outcome is disappointing, your options depend on the policy language and the facts of the file. In practical terms, that's why preparation matters so much before the umpire is ever involved.

The best time to fix a weak appraisal file is before it becomes an award.

How long does the process take

There's no single universal timeline from start to finish. Some appraisals move quickly because the appraisers are prepared and the valuation gap is narrow. Others slow down because documents are missing, umpire selection gets contested, or the vehicle requires more specialized market analysis.

What you can count on is this: once appraisal is invoked, the early deadlines in the policy move fast. If you wait to get organized until after the demand is sent, you're already behind.

Is paying an appraiser worth it

Sometimes yes. Sometimes no. The right question is whether the likely gain justifies the cost and effort.

Here's a simple way to look at it:

- Often worth it: Large valuation gap, specialty vehicle, documented upgrades, strong local market support, or diminished value dispute

- Maybe not worth it: Small gap, thin records, or a dispute that's really about coverage rather than value

- Definitely worth a closer look: The insurer's report contains obvious mismatches, omitted options, or questionable comparable vehicles

Remember that appraisal itself carries costs, and policyholders often underestimate them. That means you should approach it as an investment decision, not a reflex.

What should I gather before I talk to an appraiser

Bring the materials that help someone value the vehicle as it existed before the loss or after the repair:

- Claim documents: Insurer valuation report, settlement offer, policy language, and claim correspondence

- Vehicle proof: VIN, trim details, option list, mileage, title history if relevant

- Condition evidence: Photos, maintenance records, receipts, and upgrade documentation

- Market support: Listings or dealer data that reflect your vehicle's real market, not just anything with the same badge

The better your file, the easier it is for an appraiser to tell whether the case belongs in negotiation, appraisal, or a different path altogether.

If your insurer's total loss or diminished value offer doesn't reflect the Pacific Northwest market, Total Loss Northwest can review the claim, explain whether appraisal makes sense, and help you challenge a value dispute with independent market-based evidence.