So, your insurance company has just told you your car is a "total loss." What does that even mean?

It’s less about how bad the car looks and more about the math. An insurer declares a car totaled when the cost to fix it is more than what the car was worth right before the crash. They'll offer to pay you the vehicle's Actual Cash Value (ACV), minus your deductible, and take the car.

It’s a tough spot to be in, but you’re not alone.

Getting a Grip on the Insurance Lingo

Hearing your car is a "total loss" can feel overwhelming. The key to getting through this is to understand the language the insurance adjuster is using. The whole settlement process comes down to a few critical terms that determine the check you receive.

Don't let the jargon throw you off. It’s more straightforward than you might think.

And this is happening more and more often. The average market value for total loss vehicles is currently 8.5% higher than historical averages. Why? Because modern cars are packed with expensive tech, and repair costs are skyrocketing. You can learn more about what makes a car totalled and see how these trends affect drivers like you.

Your Guide to Total Loss Terminology

When your adjuster starts talking, they'll use specific terms that have a direct impact on your payout. Here’s a quick rundown of the vocabulary you'll need to know to hold a confident conversation.

| Term | What It Means for Your Payout |

|---|---|

| Actual Cash Value (ACV) | This is the foundation of your settlement. It’s what your car was worth in the local market one second before the crash, considering its age, mileage, condition, and features. |

| Total Loss Threshold (TLT) | A percentage set by your state. If repair costs exceed this percentage of your car's ACV, the insurer must declare it a total loss. For example, a 75% threshold on a $10,000 car means it's totaled if repairs are over $7,500. |

| Salvage Value | The amount the insurer can get by selling your wrecked car to a salvage yard. If you choose to keep the vehicle, this amount gets deducted from your settlement check. |

Understanding this terminology is your first, best tool for navigating the claim.

It shifts the power dynamic. Instead of just accepting a number, you become an informed participant in the negotiation, ready to advocate for what your vehicle was truly worth.

Knowing these definitions is the key to making sure you're treated fairly. It’s all about understanding the rules of the game so you can stand up for yourself.

Your First Moves After the Total Loss Diagnosis

Hearing the words "your car is totaled" can send your head spinning. It's a jarring piece of news, but the next 48 hours are critical. This isn't just about dealing with the shock; it's about shifting gears and taking control of the claim to protect your wallet.

First things first, get your paperwork in order. Don't wait for the adjuster to ask for it. Dig out your vehicle's title, the details of your auto loan or lease agreement, and any receipts for major recent repairs or upgrades. Did you put a brand-new set of tires on it six months ago? Replace the transmission last year? These aren't just minor details—they're evidence that can significantly boost your car's value.

Protect Your Interests and Property

Before the insurance company tows your car away for good, make it a priority to clean it out completely. I mean, completely. Check the glove box, the center console, under the seats, and in the trunk. It’s amazing what gets left behind, and this is your absolute last chance to retrieve your personal items.

At the same time, start a communication log. Every single time you talk to your adjuster, grab a notebook or open a file and write down the date, time, and a summary of what you discussed. This simple habit can be a lifesaver later, preventing any "he said, she said" confusion and keeping the insurance company accountable.

Crucial Tip: Whatever you do, do not sign over the title or accept a settlement check on the spot. The first offer is almost never the best offer. Just tell the adjuster politely that you need time to review their valuation report and the offer itself.

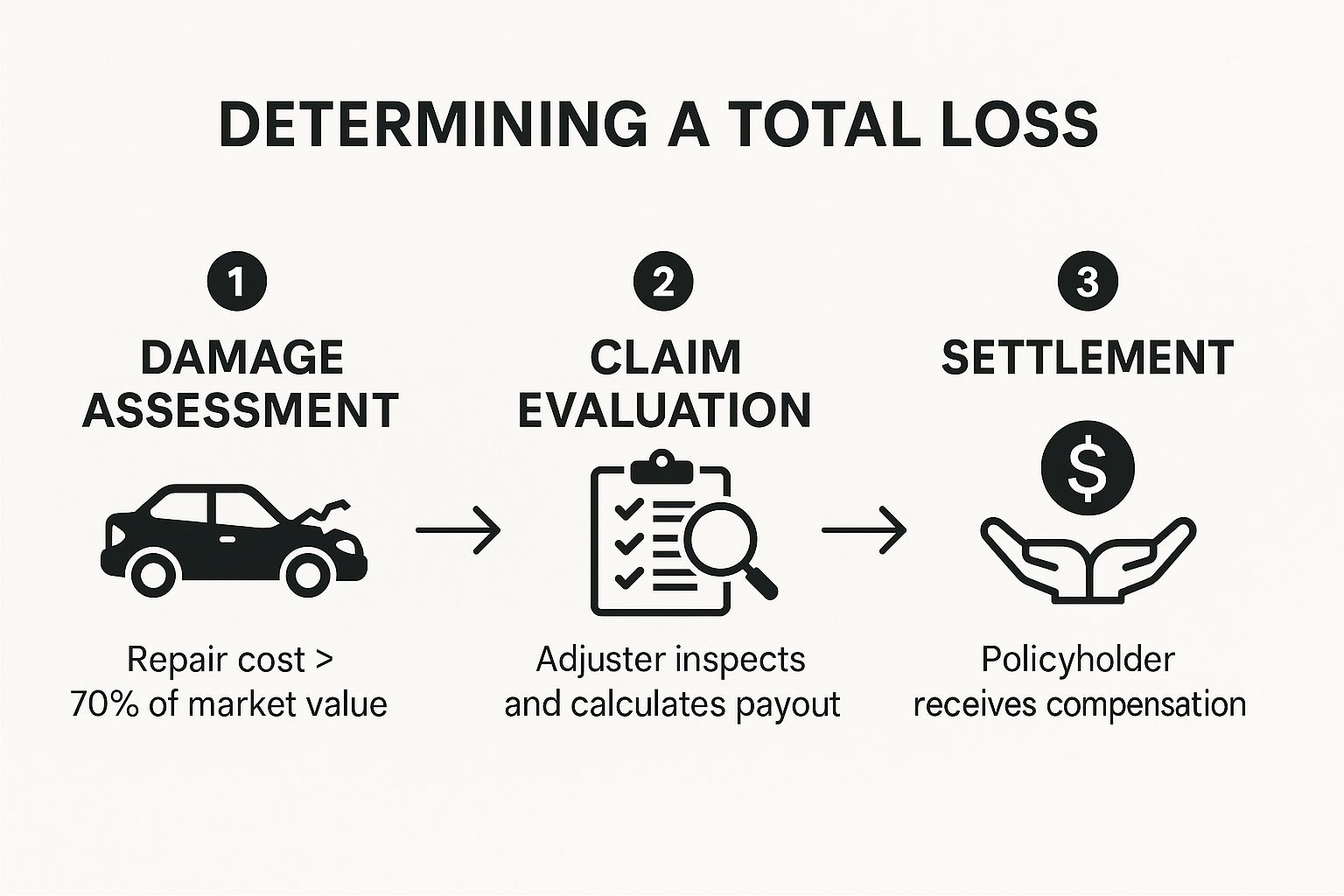

This infographic breaks down the typical total loss process, giving you a bird's-eye view of what's coming.

For the insurer, this process is a checklist. For you, every step is a chance to ensure they're using accurate information and to push for the fair value you're owed.

Prepare for the Negotiation Ahead

With your belongings and documents secured, you can now turn your attention to the main event: the settlement negotiation. The insurance company’s valuation report is their opening bid, not the final word. The groundwork you lay in these first couple of days is what will give you leverage.

While you wait for their official offer, get these items lined up:

- Vehicle Title: Have it ready to go, but don't sign anything yet.

- Loan Information: Find out your exact loan payoff amount if you still owe money on the car.

- Upgrade Receipts: Gather any proof of recent investments that added value.

- Communication Log: Keep this record current after every phone call or email.

Think of these initial actions as building your case. When you approach the "my car is totaled" situation with organization and a clear head, you're sending a strong signal to the insurer that you're an informed policyholder who expects a fair deal.

Analyzing the Insurance Settlement Offer

When the insurance adjuster finally calls with a settlement number, you might feel a wave of relief. But hold on a second. That first offer isn't the final word; it's the opening move in a negotiation. To get what you're truly owed, you need to understand exactly how they came up with that figure.

The breakdown they provide shows how they calculate your vehicle's value, starting with a base price and then making various adjustments. Your job is to go through this document with a fine-tooth comb. Scrutinize every single line item—from the base model they selected to the deductions for condition—and make sure it actually reflects your car.

Most insurance companies rely on third-party valuation services like CCC ONE to determine a car's Actual Cash Value (ACV). This software pulls sales data for similar vehicles in your area to generate a report. It's time to put on your detective hat, because this report is where you’ll find the errors that could be costing you thousands.

Decoding the Valuation Report

Don't be put off by how official the valuation report looks. It’s often riddled with simple mistakes. While these errors aren't always intentional, they almost always work in the insurance company's favor.

Start with the easy stuff: make sure the year, make, and model are correct. Then, you need to dig deeper.

The single biggest mistake I see is the wrong trim level. They might value your fully-loaded Honda CR-V EX-L as a basic LX model, a mistake that could easily be worth thousands of dollars. You also need to look for other features they missed.

- Premium Packages: Did you have a sunroof, leather seats, or that upgraded sound system?

- Factory Upgrades: What about the tow package or advanced tech suite installed at the dealership?

- Recent Investments: Don't forget those brand-new tires you bought three months ago or the recent engine work you have receipts for.

Think of the adjuster's report as a data-driven opinion, not an undisputed fact. Every error or omission you uncover is a legitimate point for negotiation, especially when you have the proof to back it up.

Remember, the adjuster working on your claim has probably never seen your car. They're just punching a VIN into a system and working off a standard checklist. It's on you to fill in the gaps and paint an accurate picture of the vehicle they're trying to value. To get a better handle on all the factors that go into this number, take a look at our guide on understanding the actual cash value of your car.

Scrutinizing the Condition and "Comps"

Once you’ve confirmed all your car’s features are listed, check how they rated its condition. Reports often default to "average" or "fair" without any real justification. If you were meticulous about maintenance and have the service records to prove it, you should argue for an "excellent" or "above average" rating. That higher grade will directly increase the ACV.

Finally, take a hard look at the "comparable vehicles" (or "comps") they used in the report. Are they genuinely comparable to your car?

Make sure they are from your local market, have similar mileage, and—this is a big one—are the exact same trim level. If the insurer is using a base model from 200 miles away to value your premium model, that's a red flag you can and absolutely should challenge.

This level of detail is more critical now than ever. The percentage of newer cars being totaled is on the rise, jumping from 64.7% of total losses in 2020 to a projected 74% by 2025 for vehicles under seven years old. This trend is largely driven by the high cost of repairing advanced tech like driver-assistance systems (ADAS), which valuation reports often overlook. You can read more about these total loss trends and their causes on Repairer Driven News.

Building Your Case for a Higher Payout

Think of the insurance company’s first offer for what it is: an opening bid. It's almost never their final, best number. Now it’s your turn to stop reacting to their valuation report and start building your own argument.

Your mission is to present a calm, logical, fact-based case that clearly shows why your vehicle is worth more than their initial calculation. This isn't about getting emotional; it's about presenting solid evidence. An adjuster can brush off a complaint, but they can't easily dismiss a well-researched counteroffer backed by proof.

Find Your Own Comparable Vehicles

The single most effective tool you have is a list of comparable vehicles, or "comps." These are real cars, just like yours, for sale right now in your area. You can't rely on the comps the insurer gives you—they often have a funny way of finding the lowest-priced examples that just so happen to support their valuation.

Your job is to find listings for cars that are a mirror image of your vehicle right before the accident.

- Year, Make, and Model: This is the non-negotiable starting point. It has to be an exact match.

- Trim Level: This is a big one. An EX-L or a Limited trim can be worth thousands more than a base model, and adjusters sometimes overlook this.

- Mileage: Try to find vehicles with mileage within 10-15% of what your car had.

- Condition: Look for listings that match the great condition you kept your car in. Photos showing a clean interior and exterior are a huge plus.

- Location: The comps have to be local. A car's value in rural Ohio is different from its value in Los Angeles, so stick to your immediate market.

Fire up sites like AutoTrader and Cars.com, and don't forget to check the inventories of local dealerships. When you find a good match, take a screenshot. Make sure the asking price, VIN, mileage, and all the key features are clearly visible. Your goal is to find at least three to five solid examples.

An adjuster can argue with your opinion all day long, but they have a much harder time arguing with real-world market data. When you show them three local cars just like yours selling for more money, it forces them to justify their lower number.

Compile Your Evidence and Write the Counteroffer

Once you have your comps, it's time to gather everything else that proves your car’s value. This is where being a meticulous owner really pays off. You want to create a clean, organized package of documents to send to the adjuster.

Here’s what that documentation should include:

- Receipts for recent major work: Did you just drop $1,200 on new tires and brakes? That adds real value.

- Proof of upgrades: That new sound system, tow package, or custom wheels aren't just for looks—they increase the car’s worth. Have the receipts ready.

- Service records: A complete maintenance history from a reputable shop shows the vehicle was well-cared-for, which directly impacts its value.

With all your proof organized, you can draft your counteroffer. This should be a professional and concise email. Leave emotion out of it and stick to the facts.

A Simple Counteroffer Email Structure

- Acknowledge and Reject: Begin by thanking the adjuster for their offer, but state clearly that you can't accept it as it doesn't reflect your vehicle's fair market value.

- Present Your Value: State the settlement amount you believe is fair, based on the evidence you've collected.

- Provide the Proof: Attach your screenshots of the comparable vehicles and copies of all your receipts. In the email, briefly explain why your comps are a more accurate picture of your car's value than the ones in their report.

- Request a Response: Politely end by asking them to review your documentation and provide a revised offer based on the new information.

This completely changes the dynamic. You're no longer just saying, "My totaled car is worth more!" Instead, you're delivering a detailed, evidence-based argument that gives the adjuster the ammunition they often need to go back and justify a higher payout to their manager.

Advanced Tactics When Negotiations Stall

So, you've done your homework. You presented solid evidence, made a reasonable counteroffer, and the adjuster just isn't budging. It’s frustrating, and this is exactly where most people throw in the towel. But don't give up. You have powerful tools at your disposal that are actually written into your policy.

When you’ve hit a brick wall, it's time to stop the back-and-forth and escalate your strategy. If the adjuster refuses to negotiate in good faith, your most effective move is to formally invoke the appraisal clause.

Invoking the Appraisal Clause

Think of the appraisal clause as your contractual trump card. It's a provision in most auto policies that takes the valuation process completely out of the insurance company’s hands.

Here’s how it works: you hire your own independent, certified appraiser, and the insurance company hires theirs. These two experts then attempt to agree on your car's actual cash value. If they can’t reach an agreement, they bring in a neutral third appraiser (called an umpire) who makes the final, binding call.

This move forces the insurer to deal with an expert valuation, not just the numbers spit out by their internal software. Yes, you have to cover the cost of your appraiser and half of the umpire’s fee, but when a vehicle is significantly undervalued, it’s often an investment that pays for itself several times over. You can dive deeper into how to use the insurance appraisal clause to break a stalemate and secure a fair settlement.

Key Takeaway: Invoking the appraisal clause is your strongest play when negotiations are deadlocked. It replaces the adjuster's lowball offer with an impartial, market-based valuation that is contractually binding.

Filing a State Insurance Complaint

Is your insurer dragging its feet, being completely unresponsive, or using what feel like unfair tactics? It might be time to file a formal complaint with your state’s Department of Insurance. This isn’t just an angry email—it’s an official grievance that gets a regulator’s attention.

Often, the mere act of filing a complaint lights a fire under the insurance company. They want to avoid regulatory scrutiny at all costs. Just make sure to document every single communication and piece of evidence, then clearly lay out why their offer is unjust. It's a serious step, but it sends a clear message that you won't be intimidated.

It's also worth knowing that adjusters are swamped. The frequency of total loss vehicles recently hit an all-time high of 22.2%, meaning salvage auctions are busier than ever. This sheer volume can lead to rushed, lowball offers, which is why pushing back is more critical than ever.

Finally, sometimes the best move is to call in a professional. A public adjuster is an expert who works for you, not the insurance company. They can take over the entire claim and negotiation process for a percentage of the final settlement. If you're facing a complicated claim or just don't have the time and energy for the fight, their expertise can be a game-changer. When it feels like the answer to "what to do when my car is totaled" is "give up," knowing these advanced options can make all the difference.

Answering Your Biggest Total Loss Questions

When you're in the thick of a total loss claim, a few specific, nagging questions always seem to pop up. You've sent in your proof, you're haggling over the settlement, and now the "what ifs" start to creep in. Let's tackle some of the most common things people worry about during this stage.

Can I Keep My Car?

This is probably the number one question I get. The short answer is: usually, yes. Insurers call this owner retention.

Here’s how it works: the insurance company calculates the car's Actual Cash Value (ACV), then subtracts your deductible and what they would have gotten for the car at a salvage auction. The remaining amount is what they pay you.

But just because you can keep it, doesn't always mean you should.

The Catch with Keeping Your Totaled Car

If you go the owner-retention route, your car's title gets stamped as a "salvage title." This is a huge red flag for future buyers and insurers, making the car incredibly difficult to sell or even get coverage for.

To make it legal to drive again, you have to get it repaired and then pass a pretty intense state inspection. Only then can you get a "rebuilt" title.

Honestly, this path really only makes sense if you're a mechanic, you can do the work yourself, or you have a very specific, non-driving purpose in mind for the vehicle. For most people, the hassle and expense just aren't worth it.

What If I Owe More Than the Car Is Worth?

This is a gut-wrenching, but common, scenario. When you're "upside-down" on your loan, the insurance company will write the settlement check to both you and your lender. The bank gets its money first to pay off as much of the loan as possible.

If the settlement doesn't cover the entire loan balance—and it often doesn't—you are on the hook for the rest. This is exactly why GAP (Guaranteed Asset Protection) insurance exists. It's designed to pay off that remaining loan balance so you aren't stuck making payments on a car that's sitting in a junkyard.

How Long Does This Whole Process Take?

It really depends. A simple, straightforward total loss claim can often be wrapped up in about 30 days. But things can drag on if the accident was complex, if there are delays in getting documents, or if you and the insurer are far apart on the settlement value. The back-and-forth of negotiation can add weeks to the timeline.

When the negotiation hits a wall and you feel like you're being lowballed, it's time to bring in a professional. At Total Loss Northwest, we're certified independent appraisers who know how to use the Appraisal Clause in your policy to your advantage. We fight to get you a settlement based on your car's true market value. Don't let the insurance company dictate the terms—find out how we can help you at https://totallossnw.com.