You've just been in an accident. Your car is at a body shop, a tow yard, or sitting in your driveway with fresh damage. The adjuster calls quickly, asks a few questions, and starts talking about value, repair scope, or whether the vehicle may be a total loss. Most drivers assume the hard part is proving what happened in the crash.

It usually isn't.

The hard part is proving what your vehicle was worth and what condition it was in right before the crash. That's where most claims get weaker than they should. If you can't show the insurer a solid pre-accident baseline, their system will supply one for you. And that baseline often misses upkeep, options, modifications, and condition details that matter.

A strong pre-loss condition evaluation strengthens your position. It turns your claim from a debate over opinions into a discussion about evidence.

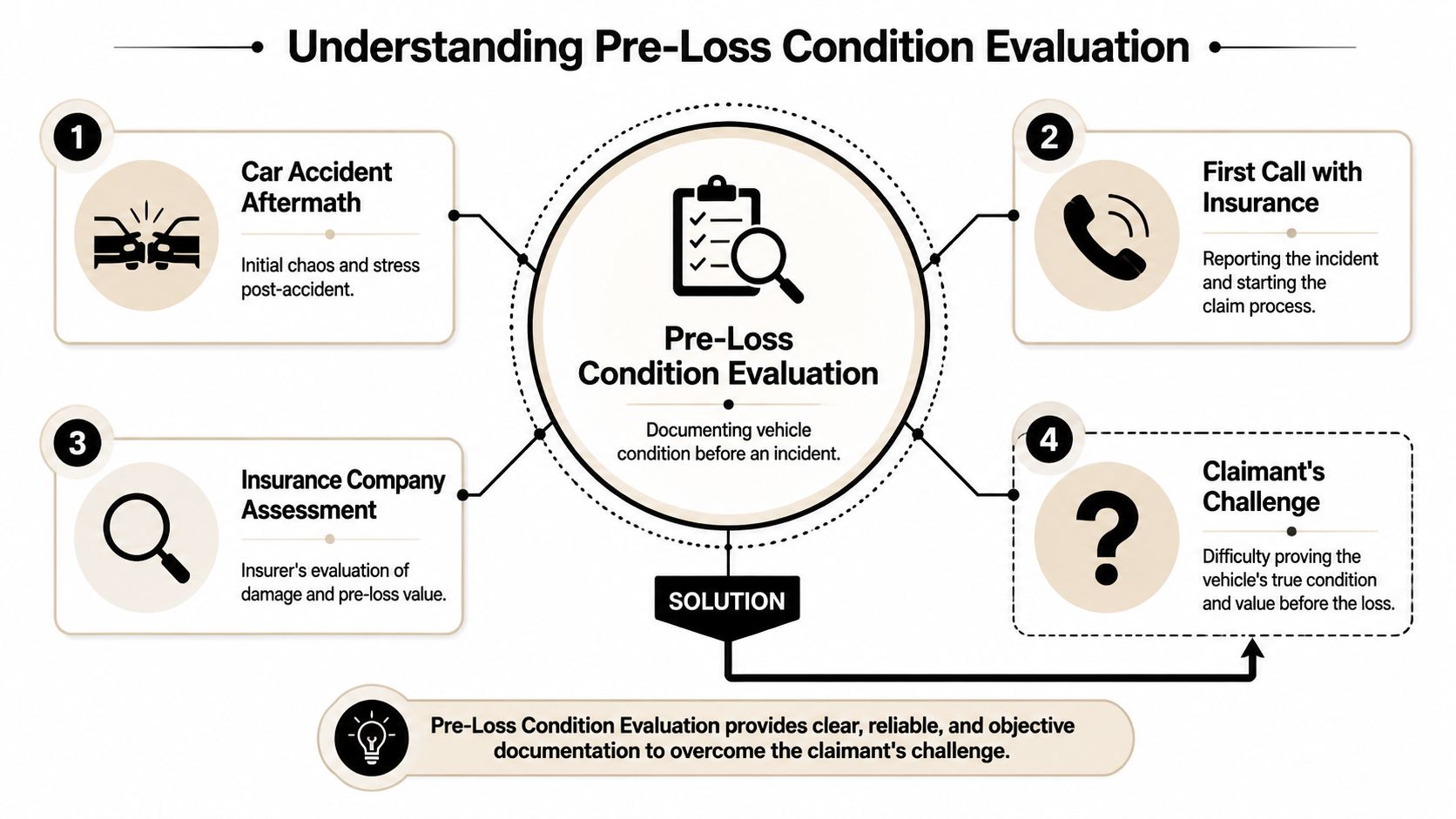

What Is a Pre-Loss Condition Evaluation

The term sounds technical, but the concept is simple. A pre-loss condition evaluation is a documented snapshot of your vehicle's condition immediately before the accident or other loss. Legal guidance describes pre-loss condition as the state of a vehicle before any damage occurs, and notes that photographs, receipts, and maintenance records are used to establish that baseline in insurance claims, as explained in this overview of pre-loss condition documentation.

That snapshot includes more than “it was fine before the crash.” It should show how the vehicle presented in its typical operational environment.

What the snapshot should capture

A proper baseline usually includes:

- Physical condition such as paint quality, panel fit, glass, wheels, trim, upholstery, and any prior cosmetic flaws

- Mechanical condition including service history, drivability, recent repairs, and whether major systems were functioning properly

- Vehicle identity details like mileage, trim level, factory options, VIN-specific equipment, and package content

- Added value items such as aftermarket wheels, suspension work, audio upgrades, wraps, or custom parts

- Ownership care shown through receipts, maintenance logs, inspection records, and dated photos

That's why a post-accident damage estimate isn't enough. A repair estimate tells you what was damaged. It does not fully establish what the vehicle was like before the impact.

Why drivers misunderstand it

It's commonly believed the insurer will naturally account for condition. Sometimes they do, but often only in broad categories inside valuation platforms. Those categories don't always reflect reality. A vehicle with exceptional maintenance, desirable options, or carefully documented upgrades can get treated like an average example if nobody builds the record.

Practical rule: If it isn't documented, don't assume the insurer will give you credit for it.

This matters even more if your car had specialty value. Collector vehicles, performance cars, luxury trims, EVs, and modified daily drivers all get undervalued when the file is thin.

Routine maintenance records also help because they show the vehicle was cared for before the loss. If you're trying to organize that history, a practical guide to vehicle safety checks can help you think through the kinds of systems and maintenance details worth preserving. And if you're not sure what an independent valuation involves, this explanation of what an appraisal for a car is gives useful context.

A pre-loss condition evaluation is the foundation. Without it, everything that follows in a claim is built on someone else's assumptions.

The Insurance Significance of Your Vehicle's Condition

Insurance is supposed to put you back in the financial position you were in immediately before the loss. For a vehicle claim, that means the carrier has to decide what your car was worth and what condition it was in just before the accident. That sounds straightforward until you see how many claims get resolved on a thin record.

One risk-management source reported that among 5,209 policyholders, 48% of claims assessed received only 54% of their calculated loss, showing how incomplete valuation or documentation can materially reduce recovery, as discussed in this article on why pre-loss inspections matter. The exact context is broader than auto claims alone, but the lesson applies cleanly to vehicles. Weak documentation costs money.

Where the conflict shows up

Insurers usually rely on internal processes and valuation software to set actual cash value or assess condition adjustments. Those systems can be useful, but they are only as accurate as the inputs. If the condition grades are too low, if key options aren't accounted for, or if comparable vehicles aren't comparable, the payout starts from the wrong number.

That doesn't mean every adjuster is acting in bad faith. It means the carrier has its own workflow, its own data sources, and its own interpretation of your car's pre-loss condition. You need your own evidence to challenge that interpretation.

Why maintenance history matters in negotiations

Condition isn't just about glossy paint. A vehicle with consistent care often has a stronger claim to above-average value than one with the same year and mileage but poor upkeep. Records that show recent brakes, tires, fluid service, suspension work, or manufacturer-recommended maintenance can support the argument that the vehicle shouldn't be graded as ordinary.

If you need a reminder of the kind of ongoing upkeep that becomes useful evidence later, these essential car care tips are a good reference point.

A claim file gets stronger when it shows what the vehicle was, not just what happened to it.

The Appraisal Clause is leverage

Most drivers don't realize their policy may give them a formal path to dispute value. That path is often the Appraisal Clause. When a total loss offer is low or a value dispute stalls, the clause can move the question out of the insurer's ordinary valuation lane and into an appraisal process built around actual evidence.

That matters because the issue is rarely just “the insurer offered too little.” Instead, the underlying problem is that the insurer may have defined your pre-loss condition too narrowly. Once that happens, every downstream number gets compressed.

A disciplined pre-loss condition evaluation gives you something concrete to put on the table. Without it, you're mostly arguing. With it, you're presenting proof.

How to Document Your Vehicle's Pre-Loss Condition

If you're already in the middle of a claim, start gathering everything now. Don't wait for the insurer to ask. The strongest files are built from ordinary records that owners already have but haven't organized yet.

Industry guidance stresses documenting not only cosmetic condition but also functional systems such as braking, steering, and other safety-related components, because those details affect whether a vehicle is restored to an equivalent pre-loss state, as outlined in this guidance on pre-loss assessment.

Start with what you can prove today

Pull together the records that already exist on your phone, in your email, and in your glovebox. Think like an appraiser. You are trying to show condition, care, originality, and value-relevant features.

| Evidence Category | Specific Items to Collect | Why It Matters |

|---|---|---|

| Photos | Dated exterior photos, interior photos, wheel close-ups, dash and odometer images, engine bay pictures | Shows cosmetic condition, mileage, trim details, and overall presentation before the loss |

| Video | Walkarounds, startup videos, cold start clips, driving clips, feature demonstrations | Helps prove functionality, warning-light status, sound, and operation |

| Service records | Oil changes, inspections, brake service, tire purchase records, alignment, suspension work, dealer maintenance history | Supports mechanical upkeep and can counter assumptions of deferred maintenance |

| Repair invoices | Prior body repairs, glass replacement, mechanical repairs, calibration work | Clarifies what was repaired before the accident and avoids confusion with new damage |

| Upgrade receipts | Wheels, tires, audio, suspension, tint, wrap, performance parts, lighting, accessories | Documents additions that standard valuation tools often miss |

| Purchase documents | Buyer's order, window sticker, financing paperwork, original listing | Helps identify options, packages, and how the vehicle was represented |

| Ownership records | Registration, emissions paperwork, inspection forms, warranty repairs | Builds continuity and confirms the vehicle's history under your ownership |

| Condition notes | Your own written summary of scratches, chips, prior flaws, recent maintenance, and what worked properly | Gives context and keeps minor pre-existing issues from being exaggerated later |

What works and what doesn't

Some evidence carries real weight. Other evidence creates noise.

What works:

- Timestamped photos from normal life such as sale listings, social posts, service visits, or family photos where the car is visible

- Invoices with dates and VIN references because they tie work directly to your vehicle

- Clear notes about prior flaws since honest disclosure increases credibility

- Records of recent big-ticket maintenance including tires, brakes, suspension, battery service, or major scheduled repairs

What doesn't work well:

- Generic statements like “the car was immaculate”

- Undated photos with no clear connection to the pre-loss period

- Screenshots without context that don't identify the vehicle

- Incomplete modification lists where the owner says parts were installed but can't show when or what

Don't hide prior damage

If the car had a scuff on one bumper corner or an old wheel scrape, say so. Minor unrelated flaws do not ruin a claim. Trying to pretend they didn't exist does.

Working standard: Document the vehicle honestly, then document it thoroughly.

A certified appraiser can often do more with a complete and candid file than with a polished but incomplete one. The point isn't to present a fantasy version of the vehicle. The point is to establish its real pre-loss condition in a way the insurer has to take seriously.

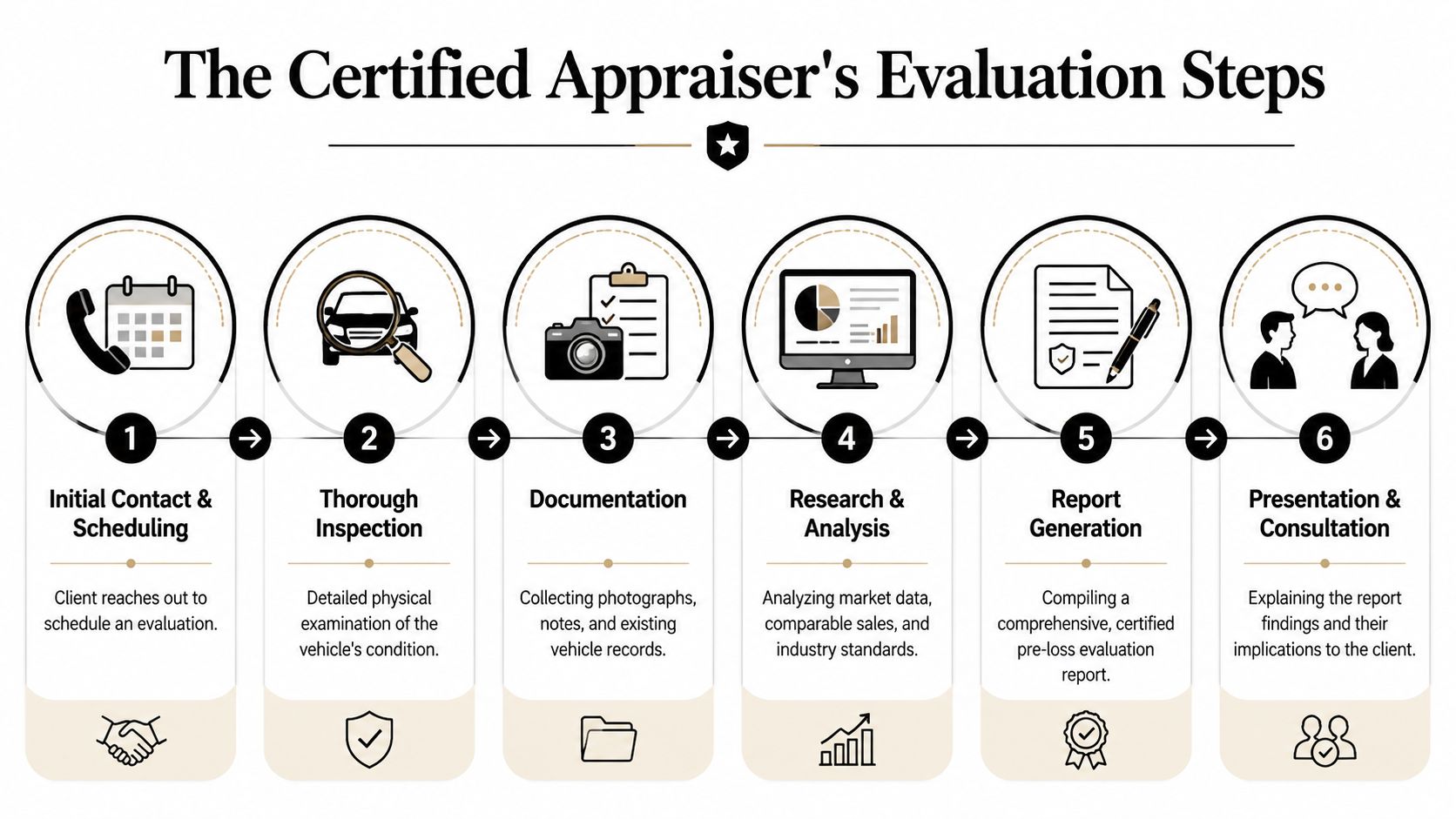

The Certified Appraiser's Evaluation Process

When a certified appraiser steps into a claim, the job isn't to repeat the insurer's number with different wording. The job is to build an independent valuation from the ground up. That means inspection, documentation, market research, and condition analysis that fits the actual vehicle, not a generic profile.

What happens first

The process usually begins with intake. The appraiser reviews the VIN, loss facts, title status, photos, insurer documents, repair estimate if one exists, and the records you've gathered. Then the vehicle is inspected in person or through a structured remote process, depending on the situation.

The key difference is attention to specifics. An independent appraiser looks for the details that shift real market value:

- Factory equipment that may be missing from the insurer's valuation

- Condition variances that can support a higher rating than the carrier assigned

- Recent repairs and maintenance that show the car was above ordinary market average

- Modifications or specialty features that generic systems often fail to recognize properly

Where independent analysis matters most

Modern vehicles create more valuation blind spots than older guides tend to acknowledge. Public guidance often gives little practical direction on EV battery condition, driver-assistance systems, software-dependent features, aftermarket wheels, wraps, or custom builds. At the same time, used-vehicle pricing remains high. The Manheim Used Vehicle Value Index was 1.4% higher year over year in May 2026, according to this discussion of pre-loss vehicle condition factors. That makes accuracy more important, not less.

An appraiser has to ask better questions than the default software asks. On an EV, battery condition and feature content may matter. On a luxury vehicle, package combinations and calibration-related options matter. On a modified truck or enthusiast car, originality versus upgraded market appeal can change how comparables should be selected.

How the report gets built

Once inspection and document review are done, the appraiser researches the local and regional market. Comparable vehicles must be comparable in the ways that buyers care about. Year, make, model, and mileage aren't enough by themselves.

A proper report usually weighs:

- Vehicle-specific facts including trim, options, mileage, condition, and service history

- Market comparables that reflect similar equipment and condition, not just broad category matches

- Adjustments for differences that materially affect value

- Claim context such as total loss, diminished value, or dispute under an appraisal clause

The insurer's software may classify your car. The appraiser has to identify your car.

If you want to see how one independent appraisal service describes that work, this page on vehicle appraisal services shows the kind of evaluation support available in these disputes.

The value of the process is not just the final number. It's the paper trail behind the number. That's what gives you something durable to negotiate from.

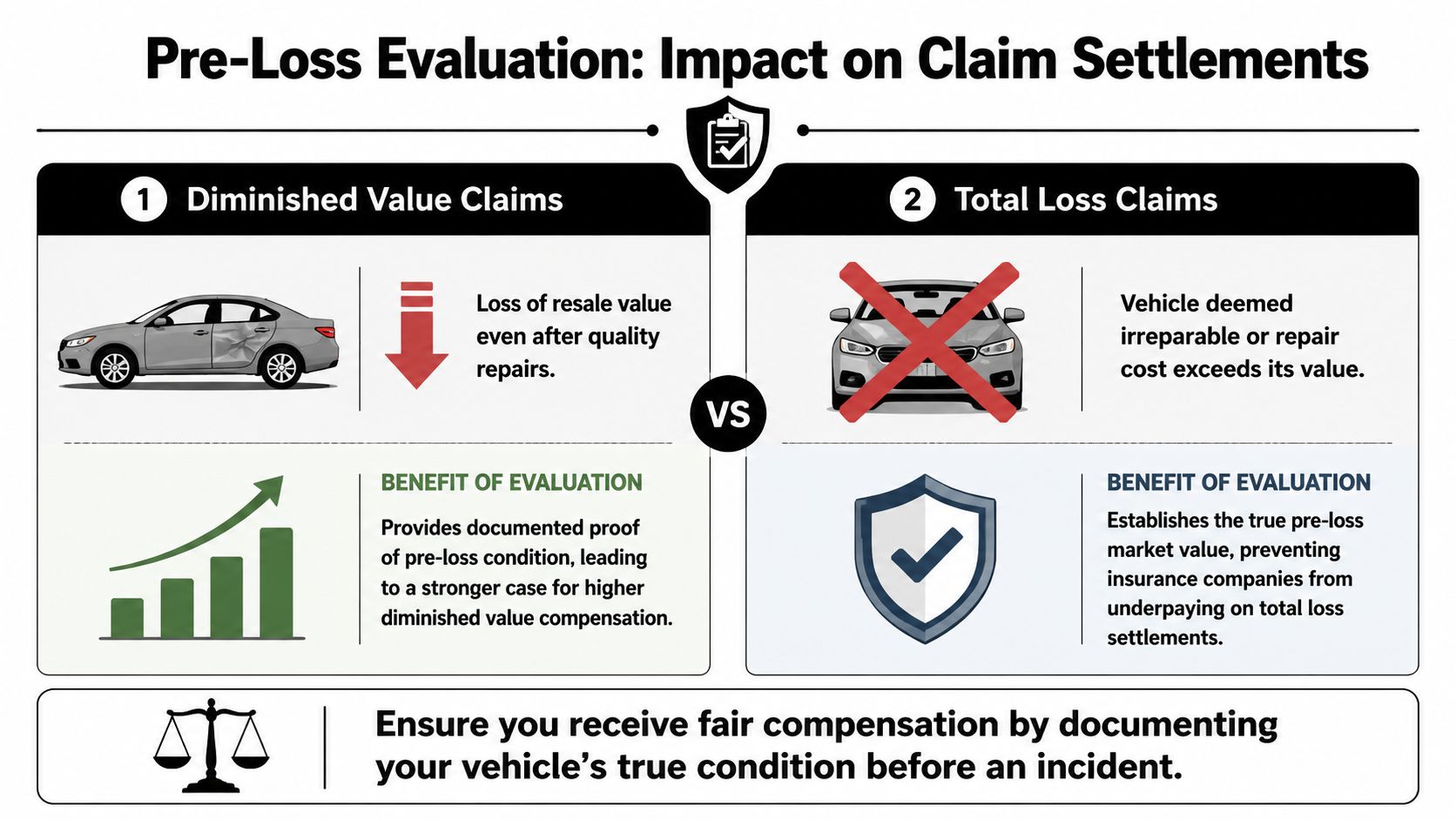

How the Evaluation Impacts Your Settlement

The settlement impact shows up in two places most often. One is a total loss claim. The other is a diminished value claim after repairs.

In a total loss dispute

If the insurer's valuation starts with average-condition assumptions and weak comparable vehicles, the settlement offer can come in low. A pre-loss condition evaluation gives your appraiser the material needed to challenge those assumptions. The issue isn't whether the insurer found a number. The issue is whether they found your number.

A stronger file can support arguments about:

- Condition grade when your vehicle was better maintained than the insurer recognized

- Option content that was omitted or undervalued

- Recent major service that affects market perception

- Modifications or specialty market appeal that generic valuation methods flatten

In a diminished value claim

If the car is repaired, pre-loss evidence still matters. Diminished value is tied to what the vehicle was worth before the accident compared with what the market will pay after a reported accident history. If the pre-accident condition was excellent, that strengthens the case that the post-repair vehicle lost meaningful resale value.

This explainer may help if you're dealing with a difficult carrier response and need a legal overview of your rights when car insurance won't pay.

A short video can also help frame how claim disputes develop in actual scenarios.

A repair restores function and appearance. It doesn't erase the market history of an accident.

The practical takeaway is simple. Better pre-loss proof creates better settlement advantage. It gives your side a record of value that doesn't depend on the insurer's first pass.

Key Considerations for Oregon and Washington Drivers

Drivers in Oregon and Washington should treat claim strategy as local work, not a national template. Valuation disputes are always tied to the actual market where the vehicle would have sold, the policy language in play, and how insurers handle claims in that region. Local comparable vehicles matter. Local repair economics matter. Local claim handling habits matter too.

Why local market knowledge changes the outcome

A national valuation approach can miss what buyers in the Pacific Northwest pay attention to. Condition, service history, trim popularity, AWD demand, truck configurations, EV feature sets, and enthusiast modifications can all play differently in Oregon and Washington than they do in a generic national database.

That's one reason local independent support can be useful. For example, services focused on this region, including diminished value auto appraisal support in Oregon and Washington, are built around the specific claim patterns and market conditions drivers here face.

Policy rights are only useful if you use them

Many drivers technically have the right to dispute value, invoke appraisal under the policy, or present independent evidence. In practice, those rights don't help much if the owner never assembles the documentation or doesn't know how to challenge a weak valuation file.

For Oregon and Washington drivers, the smart move is to assume the claim will require proof. Keep records. Save photos. Preserve service invoices. If the carrier's valuation doesn't reflect the vehicle you owned, don't treat that first number as final.

A local claim can still be mishandled by a national process. That's exactly why a region-specific, evidence-based response matters.

Frequently Asked Questions About Pre-Loss Evaluations

Can I gather the evidence myself without hiring an appraiser

Yes. You should gather it yourself whether you hire an appraiser or not. Owners usually have the best access to service records, old photos, receipts, listing screenshots, and modification paperwork.

What you may not have is the experience to convert that evidence into a valuation argument that holds up against an insurer's process. An appraiser doesn't replace your records. The appraiser organizes, tests, and applies them.

What if my car had minor damage before this accident

That's common. A small door ding, wheel rash, bumper scuff, or windshield chip doesn't destroy your claim. It just needs to be separated from the new loss.

Be direct about it. A credible pre-loss condition evaluation identifies prior unrelated flaws and prevents the insurer from using them to discount the whole vehicle unfairly. Honest documentation is stronger than exaggerated documentation.

Is an independent appraisal worth it

It depends on the size of the dispute, the vehicle, and the quality of the insurer's valuation. If the car is ordinary, the documentation is sparse, and the dispute is small, the cost-benefit may be limited.

If the vehicle is high-value, newer, specialty, modified, exceptionally clean, or obviously undervalued by the insurer, independent appraisal can be a practical tool. The bigger the gap between the insurer's assumptions and the actual vehicle, the more useful professional valuation work becomes.

What should I do right now if the claim is already underway

Start with the documents you control.

- Pull photos first from your phone, cloud backups, texts, and social media

- Request service history from dealers and repair shops that worked on the car

- Collect upgrade receipts for wheels, tires, suspension, audio, wrap, tint, or performance parts

- Write a condition summary while details are fresh, including prior flaws and recent maintenance

- Review the insurer's valuation closely for wrong trim, missing options, weak comparables, or condition errors

Does pre-loss condition matter only in total loss claims

No. It matters in both total loss and diminished value matters. In a total loss case, it affects actual cash value. In a repairable case, it helps establish how strong the vehicle's pre-accident market position was before the collision history attached to it.

The common thread is proof. The claim gets stronger when the pre-accident vehicle is documented with enough detail that the insurer has to address the facts, not just rely on default assumptions.

If you're dealing with a low total loss offer or need support proving diminished value, Total Loss Northwest provides independent auto appraisal services for Oregon and Washington drivers. If the insurer's number doesn't match your vehicle's real pre-loss condition, an evidence-based appraisal can give you a clear path to challenge it.