So, you've just been told your car is a total loss. That phone call from the insurance adjuster is often followed by a settlement offer that feels like a punch to the gut. It’s almost always a lowball number, leaving you wondering how you’re supposed to replace your vehicle with that amount.

Here's the thing you absolutely need to know: that first offer isn't the final word. It's the starting point of a negotiation. The insurance company calculates your car's Actual Cash Value (ACV), but their version of "actual value" and reality are often miles apart. You have every right to push back.

Your Car Is Totaled. What Happens Next?

The moment an adjuster slaps the "total loss" label on your car, a specific process kicks into gear—but you have more say in it than they let on. A car usually gets totaled when the repair costs hit a certain percentage of its pre-accident value. This is called the total loss threshold, and it typically sits around 70-80%, though it varies by state and your specific policy.

Make no mistake, the insurance company wants to settle this claim as quickly and cheaply as possible. They use third-party valuation software to spit out an ACV number. While these tools sound official, they often rely on flawed data, creating a frustrating gap between their offer and what it would actually cost to buy a similar car today.

Pinpointing the Valuation Gap

At its core, nearly every total loss appraisal insurance claim dispute comes down to this difference between the insurer's ACV and your vehicle's true Fair Market Value (FMV). Think of FMV as what someone in your local area would have realistically paid for your car right before the accident.

So, where does the insurance company go wrong? The gap usually comes from a few key areas:

- Bad "Comps": The comparable vehicles they use to justify their offer might be base models, have higher mileage, or be in noticeably worse condition than yours was.

- Missing Upgrades: Did you recently install a new sound system or add custom wheels? Automated reports almost never account for these. Major work, like a recent engine replacement, adds real value that has to be manually factored in.

- Ignoring Local Markets: A 4×4 truck is worth a lot more in a snowy state like Washington than it is in Florida. Their valuation has to reflect your local market, not a national average.

Your very first move should be to demand a copy of the insurer's full valuation report. Don’t just glance at the final number. Scrutinize every detail—the "comps" they chose, the condition they assigned your vehicle, and any adjustments they made. This is where you’ll find the ammunition to build your case.

Your Immediate Game Plan

That sinking feeling you get from a low offer should be your cue to switch from defense to offense. Don't even consider accepting it. Their offer is a business tactic, and you need to respond with a solid business case of your own.

Start digging up every piece of paper related to your car. I'm talking about the original bill of sale, every maintenance receipt, and proof of any recent purchases or upgrades. For example, if you just spent $1,200 on new tires a month before the crash, that receipt is powerful evidence that their valuation is off. By getting proactive, you immediately change the dynamic. You're no longer just accepting their numbers; you're proving them wrong with cold, hard facts.

Using the Appraisal Clause in Your Policy

When you're at a dead end with your insurance company over your car's value, it can feel like you have no options. But you do. Buried in your policy is a powerful tool designed for this exact situation: the Appraisal Clause.

Think of it as your contractual right to a second opinion. Invoking this clause formally rejects the insurer's lowball offer and forces the dispute into a structured, binding resolution process. It's often the single most effective way to break a stalemate in a total loss appraisal insurance claim dispute.

Finding and Understanding the Appraisal Clause

First things first, you need to find this clause in your policy documents. Don't look on the declarations page; it won't be there. You'll need to dig into the main policy booklet, usually in the section labeled "Physical Damage" or "Damage to Your Auto."

The wording can vary slightly, but you're looking for language that outlines a clear process for disagreement. It will say something along these lines:

- "If we and you do not agree on the amount of loss, either may demand an appraisal of the loss."

- "Each party will select a competent and impartial appraiser."

- "The two appraisers will select an umpire."

- "An award in writing of any two will determine the amount of loss."

This isn't a friendly suggestion—it's a contractual right. Once you trigger it, the insurance company is obligated to participate.

My Two Cents: I've seen it time and again: the moment a policyholder properly invokes the Appraisal Clause, the entire dynamic shifts. It levels the playing field, moving you away from frustrating phone calls and toward a process with real teeth.

This is so critical because most total loss disputes boil down to one thing: a disagreement over the valuation method. Insurers lean heavily on third-party software that uses algorithms you'll never see. These "black box" valuations are a constant source of friction, and challenging their statistical validity can feel impossible—until you invoke the clause.

How to Formally Invoke the Clause

Telling the adjuster on the phone that you want an appraisal isn't enough. You have to make it official. A formal, written demand is non-negotiable.

Send your letter via certified mail with a return receipt. This gives you undeniable proof that they received your demand, creating a paper trail that protects you. Your letter should be short, professional, and to the point. No need for legal jargon or angry prose.

What Your Letter Must Include

- Your Details: Full name, address, and policy number.

- Claim Details: The claim number and the date of your loss.

- Statement of Disagreement: A simple sentence stating you dispute their Actual Cash Value (ACV) offer.

- Formal Demand: Explicitly write, "I am invoking the Appraisal Clause of my policy."

- Your Appraiser's Details: You must name the independent appraiser you've hired and include their contact information.

Taking this formal step signals that you're serious and know your rights. It transforms the conversation from an informal argument into a binding procedure defined by your contract. To get a better handle on the specifics, I recommend learning more about how the auto insurance appraisal clause works. Understanding this process is the bedrock of a successful dispute, ensuring you get the fair treatment your policy guarantees.

Building an Evidence-Based Case for Your Car's Value

Arguing with an insurance adjuster based on emotion will get you nowhere fast. What they can't ignore, however, is a mountain of well-organized, factual evidence. When it comes to winning total loss appraisal insurance claim disputes, the strength of your proof is everything.

Your mission is to assemble a file that meticulously breaks down the insurer's lowball offer and rebuilds it with cold, hard facts. This isn't about what you feel your car was worth; it's about proving its true Actual Cash Value (ACV) right before the accident.

Finding Compelling Comparable Vehicles

The bedrock of any vehicle valuation is "comps"—comparable vehicles currently for sale in your local area. The insurance company's report will include the comps they used, and scrutinizing this list is your first move. More often than not, their examples are poor matches chosen to justify a lower value.

Now, you get to find better ones. Your goal is to find vehicles that are a mirror image of your car, focusing on:

- Trim Level: A Toyota Camry XSE is a different beast than a base LE model. Make sure you’re comparing apples to apples.

- Mileage: Search for listings within 10-15% of your car’s mileage at the time of the crash.

- Condition: Was your car garage-kept and spotless? Don't let them use comps with dings, dents, and stained interiors. Find cars that reflect your car's pre-accident condition.

- Location: Comps must be from your local market, generally within a 75-100 mile radius. National data from a site like Kelley Blue Book is a starting point, but local dealer listings are the real proof.

I always tell my clients to save screenshots of these listings as PDFs. Make sure the screenshot captures the dealer's name, the price, VIN, mileage, and the date you found it. This creates a time-stamped paper trail.

Documenting Your Vehicle's Unique Value

Next up is proving what made your car stand out. Standard valuation reports from insurers are notoriously bad at factoring in recent upgrades or premium features. This is where your personal records become your secret weapon.

A Quick Tip from Experience: Don't just claim you had upgrades; prove their value with receipts. Simply saying "the engine was great" is weak. A receipt for a $3,000 engine overhaul six months before the accident? That's undeniable proof of added value.

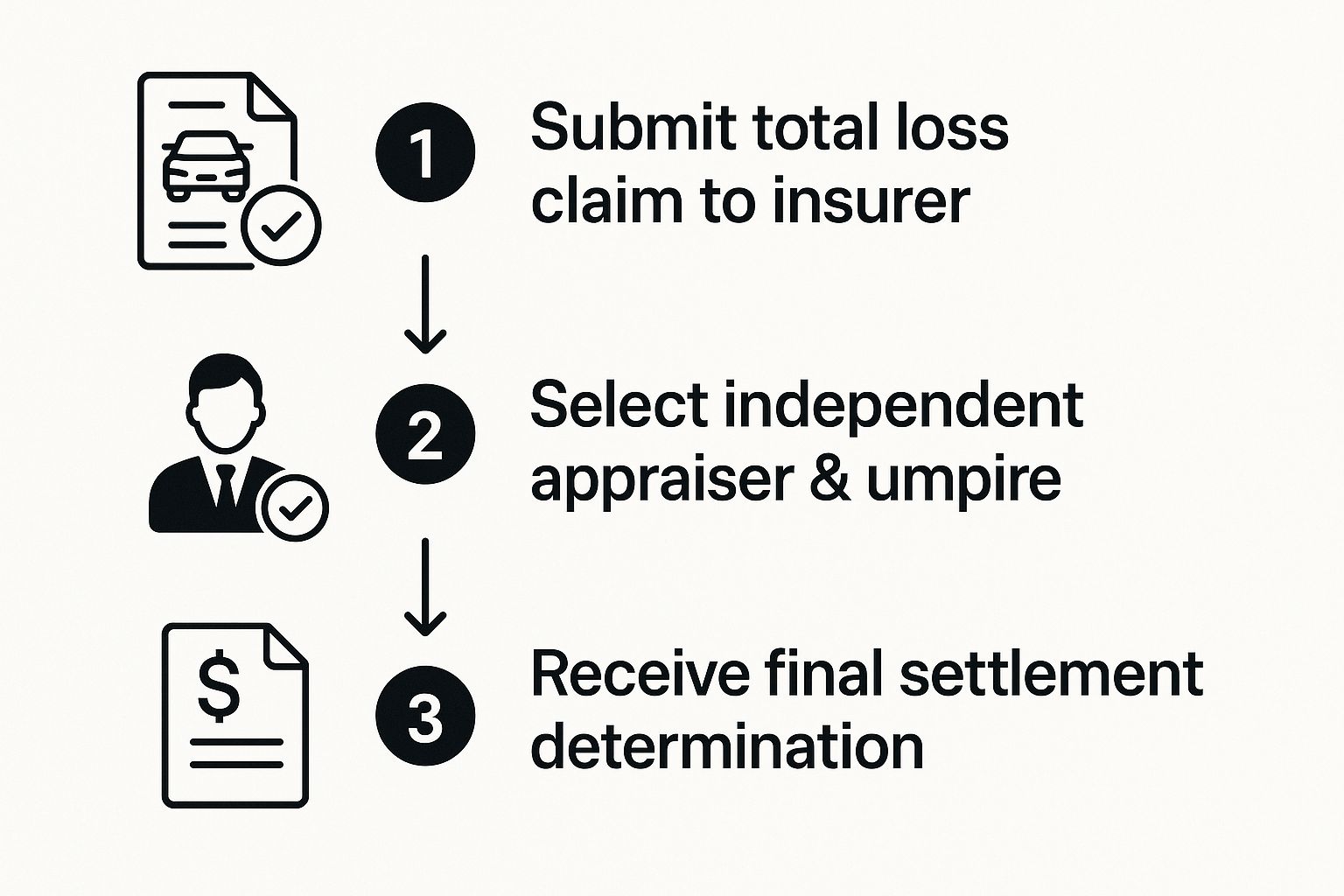

Once you have your evidence and decide to formally dispute the offer, the process follows a clear path.

This visual shows exactly what that journey looks like.

As you can see, hiring an independent appraiser is the key step. It takes the negotiation out of the insurer's hands and puts it into a neutral, fact-finding process.

So, let's talk about the specific proof your appraiser will need from you.

Your Evidence-Gathering Checklist

To build the strongest possible case for your vehicle's value, you need to collect and organize key documents. Think of it as creating a portfolio for your car. A complete and professional package gives your appraiser the ammunition they need to fight for you.

For a deeper look into all the factors that go into a vehicle's final number, you can explore our detailed guide on how much your totaled car is worth.

Here is a table outlining the critical evidence you should start gathering immediately.

| Essential Evidence for Your Total Loss Claim | ||

|---|---|---|

| Evidence Category | Specific Items to Collect | Why It's Important |

| Maintenance History | Oil change receipts, tire rotation records, service invoices from your mechanic. | Establishes a pattern of consistent care, proving the vehicle was in excellent mechanical condition. |

| Recent Investments | Invoices for new tires, brakes, battery, timing belt, or any major repairs in the last 1-2 years. | Demonstrates recent spending that directly adds to the vehicle's pre-loss value. |

| Original Documents | The original window sticker (Monroney label) if you have it. | Provides undeniable proof of the vehicle's factory-installed options, packages, and trim level. |

| Photographic Proof | Pre-accident photos of your car (interior and exterior) showing its condition. | Directly refutes an insurer's attempt to classify your car's condition as "average" or "fair" without proof. |

| Unique Features | Receipts for aftermarket additions like custom wheels, stereo systems, or performance parts. | Ensures you get credit for value-adding features that standard valuation tools often miss. |

By presenting this information clearly to your independent appraiser, you empower them to build an airtight report. They will use your documentation to justify a higher, more accurate valuation—one the insurance company can't just brush aside. The effort you put in now directly translates to a better settlement later.

Finding the Right Independent Appraiser

Once you've decided to invoke the appraisal clause, your next move is arguably the most important one you'll make: choosing your independent appraiser. This isn't just a box to check. This person is your advocate, your expert witness, and your best weapon in securing a fair settlement.

Picking the right professional can easily mean the difference between accepting thousands less than you're owed and getting the true market value for your totaled vehicle. This isn't a job for your local mechanic or a family friend who knows a bit about cars. You're entering a formal dispute, and you need a specialist.

Don't Hire a Damage Appraiser for a Valuation Fight

First things first, let's clear up a common—and costly—misconception. When most people hear "appraiser," they picture the person who inspects a dented fender and writes up a repair estimate. That's a damage appraiser. Their expertise is in parts, labor costs, and repair procedures.

That's not who you need.

You need a valuation dispute specialist. This is a completely different skill set. These experts live and breathe vehicle market analysis. Their entire focus is on determining a car's Actual Cash Value (ACV). They know how to dig up solid comparable vehicles, document every last feature and upgrade, and build a report that can stand up to an insurance company's scrutiny.

Hiring a damage appraiser for this job is like asking a real estate agent to do your taxes. They both work with big numbers, but you wouldn't trust them with the wrong task.

How to Properly Vet Your Appraiser

Finding a true valuation expert takes more than a quick online search. You have to do your homework and really dig into their qualifications to make sure they have a history of winning these battles against insurance carriers.

As you start talking to potential appraisers, here’s what to look for and what to ask.

- Look for Real Credentials: Don't be shy about asking for credentials. Certifications from respected groups like the International Automotive Appraisers Association (IAAA) or an ASE Certified Master Technician designation show a serious commitment to their craft. It's a sign they've met a certain standard.

- Ask About Their Dispute Experience: Get straight to the point. "How many total loss appraisal disputes have you actually handled?" You want someone who has navigated this specific process hundreds of times, not just a handful. They need to know the players and the tactics.

- Demand to See Their Work: Ask for a sample of a redacted report from a previous case. A pro's report will be thick, detailed, and almost academic in its approach. It should tell a compelling story about the vehicle's value, not just list a few numbers. If it looks flimsy, walk away.

A good appraiser will confidently walk you through their process for dismantling the insurance company's low offer. If they're vague or can't give you a straight answer about their strategy, it's a huge red flag. Trust your gut.

The Interview: Questions You Must Ask Before Hiring

Treat this like a job interview, because that's exactly what it is. You're hiring someone to protect a significant financial asset. Go into the conversation prepared with a list of pointed questions.

Your Interview Checklist:

- Do you have specific experience with my car's make and model? (Expertise with a Toyota Camry is different from a vintage Porsche).

- Where do you find your "comps" (comparable vehicles), and what's your method for adjusting their value based on condition, mileage, and options?

- What's your fee structure? Most will charge a flat fee or a percentage of the "uplift"—the amount they get you above the insurer's initial offer. Make sure you understand it completely.

- How do you handle it when the insurance company's appraiser disagrees with your findings?

- What's your success rate? Can you give me an idea of how often you secure settlements significantly higher than the first offer?

Choosing your appraiser is the move that sets the board for the rest of the game. A top-tier, unbiased professional will come armed with a report built on hard facts and market data that the insurer simply can't ignore. This is the linchpin of your case—invest the time to get it right.

Getting to the Finish Line: Final Appraisal and Negotiation

Once you've handed over all your evidence to your chosen independent appraiser, you can take a step back. This is where your expert takes the wheel. Their first move is to formally contact the insurance company's appraiser, officially kicking off the work of settling your total loss appraisal insurance claim dispute.

The two appraisers will set up a meeting, either face-to-face or online, to go over their findings. This is your appraiser's moment to shine. They'll present their detailed valuation report, using the evidence you gathered to systematically break down the flaws in the insurance company's initial offer. They'll go through their list of comparable vehicles, their condition assessments, and any adjustments for upgrades, building a rock-solid case for your vehicle's true value.

Believe it or not, this first meeting is often where the magic happens. A well-prepared, professional report from a credible appraiser can be enough to get the insurer’s appraiser to see reason. Many times, they'll agree to a new value somewhere between their initial lowball number and your appraiser's valuation.

What if They Can't Agree? The Umpire's Role

Sometimes, the two appraisers just can't find common ground. That's perfectly normal, and it's why the process includes a neutral third party: the umpire. The umpire is a seasoned professional, usually a highly respected appraiser or industry veteran, that both sides agree upon before the negotiations even begin.

The umpire doesn't start from scratch. Think of them as a tie-breaker. Both your appraiser and the insurer's appraiser will present their final valuation and the evidence backing it up. The umpire reviews everything from both sides and makes the final call.

Here's the key takeaway: An award in writing that is signed by any two of the three parties—your appraiser, the insurer's appraiser, or the umpire—becomes the final, binding settlement amount. Once that paper is signed, the debate is over. The insurance company is legally bound to pay that figure.

This framework is brilliant because it prevents the dispute from dragging on forever. The umpire acts as a vital check and balance, ensuring a stalemate is never the final outcome.

Setting Realistic Expectations for Timelines and Tactics

While this process is designed to be fair, it's not exactly fast. From the moment you invoke the appraisal clause to getting a final decision, you should realistically expect it to take anywhere from 30 to 90 days. My best advice? Be patient. Let your appraiser do their thing without rushing them; a hurried job can lead to costly mistakes.

You should also be aware that some insurance appraisers might try to play games. I’ve seen it all—slow-walking communications, dragging their feet on scheduling, or refusing to agree on a reasonable umpire. A good independent appraiser has seen these delay tactics a thousand times and knows exactly how to handle them professionally to keep things on track. This is yet another reason why choosing the right expert is so critical.

Reaching a Final Settlement

Whether the agreement comes from the two appraisers finding common ground or from the umpire's binding decision, the result is the same: a new, final number. This figure officially becomes the Actual Cash Value (ACV) for your totaled vehicle.

The insurance company will then cut you a check for this new, higher amount, minus your deductible.

The whole journey, from that frustrating first lowball offer to the final binding award, is there to protect you. By using the appraisal clause in your policy and hiring a true expert, you're not leaving things to chance. For a deeper dive into the specific tactics used during these discussions, check out our complete guide to total loss settlement negotiation. This structured, evidence-first approach is your most reliable path to getting a settlement that truly reflects what your vehicle was worth.

Frequently Asked Questions About Total Loss Disputes

When you're in the thick of a total loss claim, you're bound to have questions. Even with a solid game plan, some specific concerns can keep you up at night. Let's walk through some of the most common questions I hear from policyholders who are fighting a lowball offer. It's crucial to get these answers straight to keep the process moving and manage your own expectations.

The stakes are higher than you might think. We're not talking about small change here. Total loss claims have become a massive issue across North America, with over $1.5 billion in claims recognized by the end of 2023. In just the last three years, a staggering $550 million of that has been paid out.

Consider this: 18.2% of policies had at least one claim, and nearly 43% of the claims paid out were for more than a dollar-for-dollar loss. That tells you disputes are common, and pushing back often leads to a better outcome. You can dive deeper into these trends in Aon's 2024 Global Claims Study.

What if My Loan Is More Than the Settlement?

This is one of the most stressful situations a car owner can face. It’s often called being "upside down" or "underwater" on your loan, and it happens when you owe the bank more than your car is actually worth.

The insurance company's settlement is based purely on the car's Actual Cash Value (ACV), not your loan balance.

If you have Guaranteed Asset Protection (GAP) insurance, now is the time to use it. This is precisely what GAP coverage is for. It bridges the gap by paying the difference between the ACV settlement and what you still owe the lender, saving you from a significant financial blow.

What if you don't have GAP? Unfortunately, you'll be on the hook for the difference. You’ll have to pay the remaining loan balance out of pocket after the insurance settlement is paid.

Key Takeaway: The entire point of the appraisal dispute is to secure the correct ACV for your vehicle. A higher, more accurate settlement can dramatically shrink or even eliminate that gap between the insurance payout and your loan balance.

How Long Does the Appraisal Dispute Process Take?

My best advice? Be patient. While everyone wants a quick resolution, it's wise to set a realistic timeline.

From the day you officially invoke the appraisal clause to the day you have a final, binding settlement, the process typically takes anywhere from 30 to 90 days.

Of course, several things can speed this up or slow it down:

- State Rules: Some states have regulations that put a clock on how quickly insurers must respond.

- The Other Appraiser: A cooperative appraiser from the insurance side can keep things moving. A difficult one who uses delay tactics can drag the process out for weeks.

- Needing an Umpire: If the two appraisers can't find common ground, bringing in a neutral umpire adds another layer—and more time—to the process.

Your best defense against unnecessary delays is hiring a proactive, experienced independent appraiser who knows how to keep the pressure on and move the claim forward.

Can I Keep My Totaled Car?

Yes, in most cases, you have the option to keep your car even after it's been declared a total loss. This is commonly known as "owner retention."

If you decide to go this route, the insurance company will first determine the vehicle's salvage value—that's the price they'd get for selling the wrecked car at a salvage auction. They will then subtract that salvage value from your final ACV settlement.

For instance, if your final agreed-upon settlement is $20,000 and the car has a salvage value of $2,000, you’ll receive a check for $18,000 and the keys to your car.

Just be aware that the state will issue the car a "salvage title." This branded title makes insuring the vehicle much more difficult and slashes its resale value, even if you restore it to perfect condition.

When you're facing down an insurance company's lowball offer, you need an expert in your corner. Total Loss Northwest specializes in total loss and diminished value appraisals, fighting to get you the true market value you're owed. We handle the entire appraisal clause process, ensuring your claim is backed by a powerful, evidence-based report. Don't leave money on the table—get the settlement you deserve. Contact us today at https://totallossnw.com.