You've got the estimate. The adjuster says the number is fair. Your car may be repairable, or the insurer may be pushing it into total loss territory faster than you expected. Either way, the process often feels one-sided because the insurer handles claims every day and you don't.

That's where solid Washington claim support matters. A fair claim doesn't start with arguing louder. It starts with understanding the rules, documenting the right things, and knowing when the insurer's number is just an opening position rather than the final word.

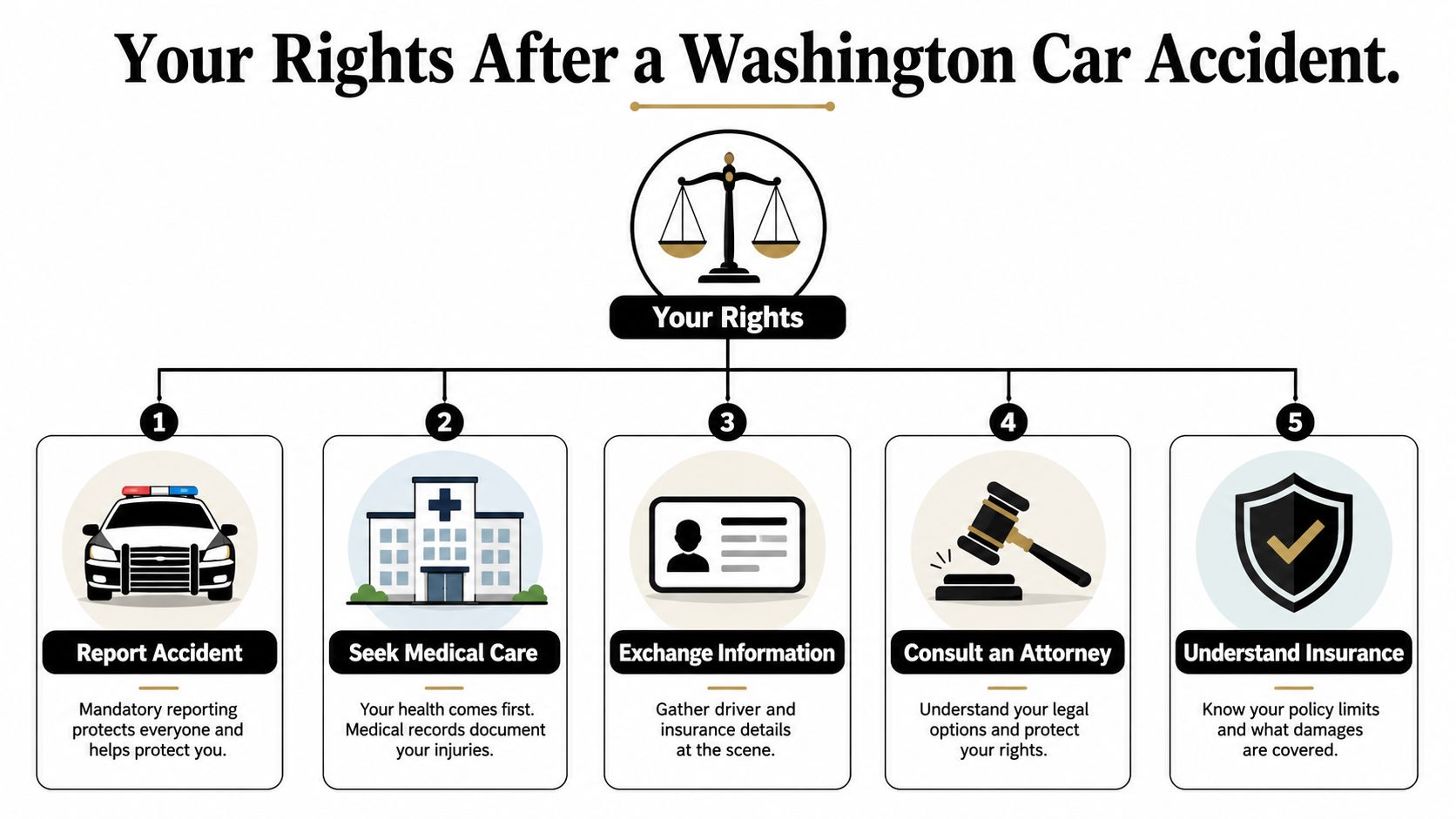

Your Rights After a Washington Car Accident

The first thing to know is that Washington doesn't use the kind of simple percentage rule you may have heard about in other states. In Washington, a vehicle is a total loss when the cost of repairs plus salvage value equals or exceeds the vehicle's Actual Cash Value, under Washington total loss rules explained with WAC 284-30-391.

That matters because it gives you a real standard to measure the insurer's decision against. If the carrier is calling your vehicle a total loss, or refusing to, the question isn't whether the adjuster “feels” it makes sense. The question is whether the numbers fit the legal formula.

Start with the basics and protect the record

Most drivers focus on the damage first. That's normal. But a strong claim also depends on what you do in the first few days after the crash.

Use a simple order of operations:

- Report the crash properly so there's a record of the event.

- Get medical attention if you're hurt, even if symptoms seem minor at first.

- Exchange complete information with the other driver and confirm policy details.

- Notify your insurer promptly and keep copies of every communication.

- Avoid guessing about value before you've seen the insurer's documentation.

If you need a practical refresher on immediate next steps, this post-accident legal guidance is a useful companion for the early stage of the process.

Know what the insurer must do

Washington claim support starts with one principle. The insurer has to follow the state's valuation rules, not its own convenience.

Practical rule: If the insurer's conclusion affects whether your car is repaired, totaled, or underpaid, ask what data supports that conclusion.

That question changes the tone of the claim. Instead of debating opinions, you're requiring the carrier to show its work.

A few rights are especially important in Washington:

- A lawful total loss decision: The company must apply the Washington formula, not an informal repair percentage.

- A supportable value calculation: The insurer can't just drop a number on you without a valid valuation method.

- A settlement based on pre-loss value: The focus is what the vehicle was worth immediately before the crash, not what the company would prefer to pay.

- A chance to challenge a low number: If the valuation is off, you're not stuck accepting it.

Why this changes your leverage

Drivers lose ground when they treat the insurer's first conclusion as final. In practice, many disputes come down to whether the company used sound comparables, recognized the vehicle's actual condition, and followed Washington rules from start to finish.

Once you understand that, the claim becomes less personal and more procedural. That's good for you. Procedures can be tested. Math can be challenged. Bad comparisons can be replaced.

That's the foundation of effective Washington claim support. You don't need to know every insurance phrase. You need to know where the carrier has to be right.

Documenting Everything for a Stronger Claim

A claim gets stronger when your file tells a complete story before the insurer finishes building theirs. That means documenting damage, yes, but also documenting your vehicle's condition, equipment, maintenance history, and market position before the crash.

Start early. The best evidence is usually gathered before the car is moved, cleaned, stripped, or written up by someone else.

Build a file that another person can understand

Think like a stranger reviewing your case months later. If they open your folder, can they see what happened and what the vehicle was worth?

Collect these items first:

- Scene photos: Wide shots, close-ups, skid marks, debris, traffic controls, and weather conditions.

- Damage photos: Every impacted panel, wheel, light, sensor area, interior deployment, and undercarriage issue you can safely capture.

- Vehicle identity details: VIN, odometer, trim badge, wheel package, and any option package labels.

- Ownership and maintenance records: Registration, title copy if available, service invoices, tire receipts, recent parts replacements, and upgrade receipts.

- Communication logs: Claim number, adjuster names, email chains, call notes, and every estimate version.

For a more complete checklist, this guide to auto claim documentation is worth saving before you start sending files around.

Don't just document damage. Document value.

Many owners find themselves shorted. They send excellent crash photos but almost nothing showing what the vehicle was before impact.

If your car had recent maintenance, new tires, a clean interior, desirable options, or documented upgrades, gather proof. If it was a collector vehicle, specialty trim, or unusually clean for its age, document that condition in plain, visual terms.

A useful file often includes:

| Evidence type | Why it matters |

|---|---|

| Service records | Shows the vehicle was maintained rather than neglected |

| Upgrade receipts | Helps establish equipment the insurer may overlook |

| Pre-accident photos | Supports condition adjustments in your favor |

| Comparable listings you saved | Helps test whether the insurer's valuation fits the real market |

A blurry photo of the damage is less helpful than a clean record of the car's condition before the collision.

What works and what usually doesn't

Some evidence moves the claim. Some evidence just creates noise.

What tends to work:

- Organized photo sets: Label by front, rear, driver side, passenger side, interior, wheels, and options.

- Receipts with dates and VIN references: Those tie your records directly to the car.

- Short written summaries: One page explaining the vehicle's condition, recent work, and notable features helps an appraiser or adjuster understand the file quickly.

What usually doesn't:

- Sending random screenshots with no explanation

- Arguing from emotion instead of records

- Assuming the insurer noticed every option or recent repair

- Waiting until late in the dispute to gather proof

Good Washington claim support is often simple. Keep records clean, chronological, and easy to verify. If the insurer undervalues your vehicle later, your documentation becomes the backbone of the challenge.

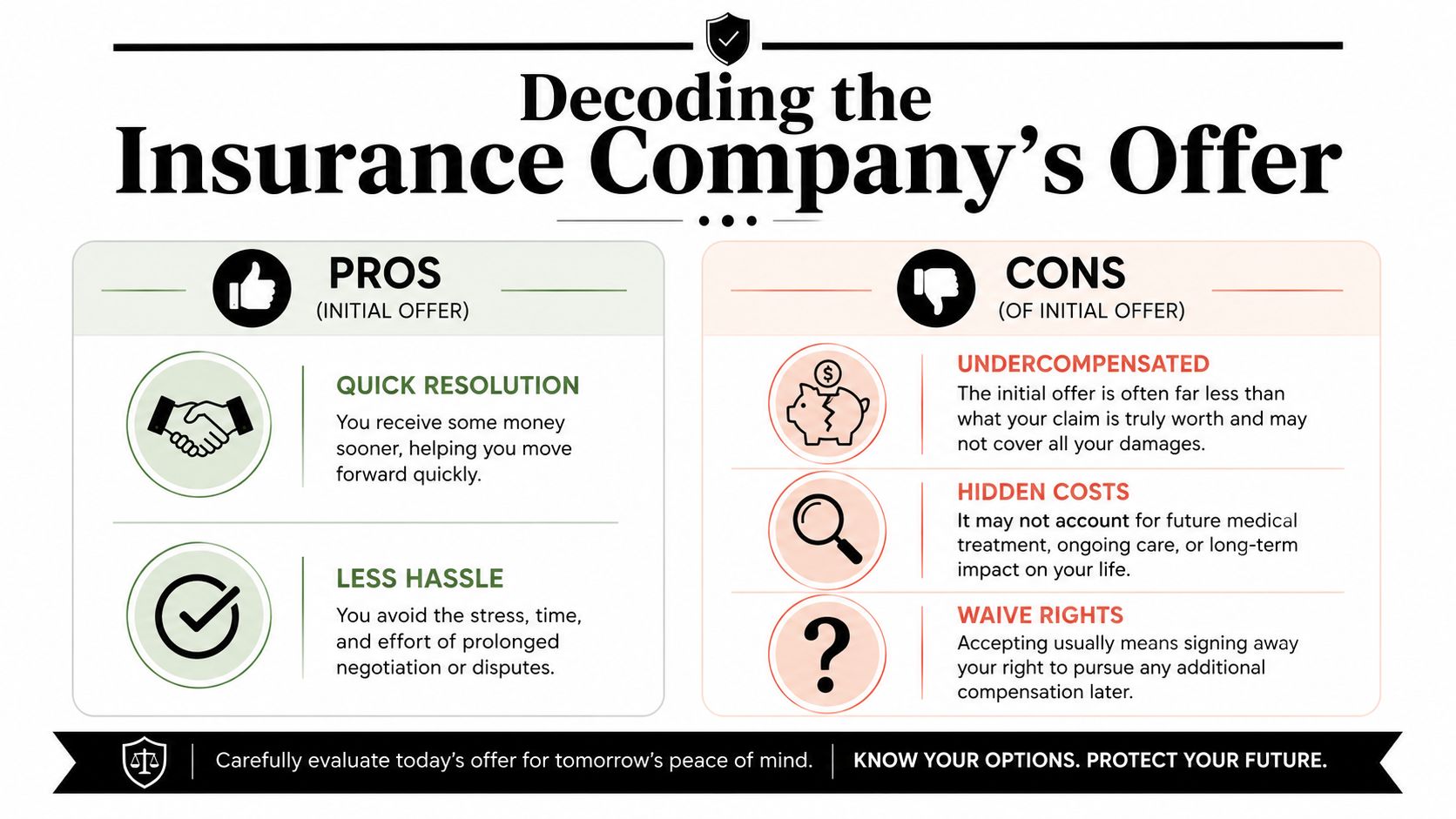

Decoding the Insurance Company's Offer

When the insurer sends its settlement number, most drivers look at the total and stop there. That's a mistake. The actual story is inside the valuation method, the comparable vehicles used, and the adjustments hidden in the report.

Washington requires insurers to determine Actual Cash Value through specific methods, including comparable vehicles, dealer quotes, or a computerized source that meets state requirements. The insurer also must include applicable taxes, license fees, and other fees in the ACV calculation, as outlined in this overview of Washington valuation dispute rules under WAC 284-30-391.

Ask for the valuation report before you argue

If you don't have the full valuation report, you're debating a number without seeing the inputs. That puts you behind immediately.

Request the report and review it line by line. Look for the comparables. Look for mileage adjustments. Look for condition changes. Look for omitted features.

A short review table helps:

| What to check | Why it matters |

|---|---|

| Comparable vehicles | They should actually resemble your vehicle in trim, condition, and market position |

| Options and packages | Missing features can pull the value down |

| Condition adjustments | Negative adjustments are often accepted too easily unless challenged |

| Taxes and fees | Those should be reflected in the ACV calculation |

Where low offers usually come from

A low settlement number often comes from one or more valuation choices rather than one obvious error. The insurer may use comparables that are technically similar but commercially weaker. It may miss trim-specific equipment. It may rate your car's condition lower than the file supports.

Watch for these patterns:

- Weak comparables: Different trim, rougher condition, or vehicles that don't compete with yours in a purchase decision

- Incomplete equipment lists: Premium audio, technology packages, safety systems, wheels, towing packages, or specialty options left out

- Condition penalties with thin support: Interior, paint, or tire deductions that don't match your records

- Geographic shortcuts: A valuation can skew low when the search pool doesn't reflect the local market

If the report doesn't make sense on paper, the settlement probably won't be fair in practice.

Treat the first number as a position, not a verdict

There's a practical difference between an insurer's first offer and a defensible value. A first offer is often built for speed. A defensible value holds up when someone checks the assumptions.

That's why Washington claim support isn't about rejecting every offer automatically. It's about finding out whether the offer survives scrutiny. If it does, resolution can be quick. If it doesn't, the report itself gives you the road map for the challenge.

The best response is specific. Don't say the number feels low. Point to the bad comparable, the missed option, the unsupported condition deduction, or the omitted fees.

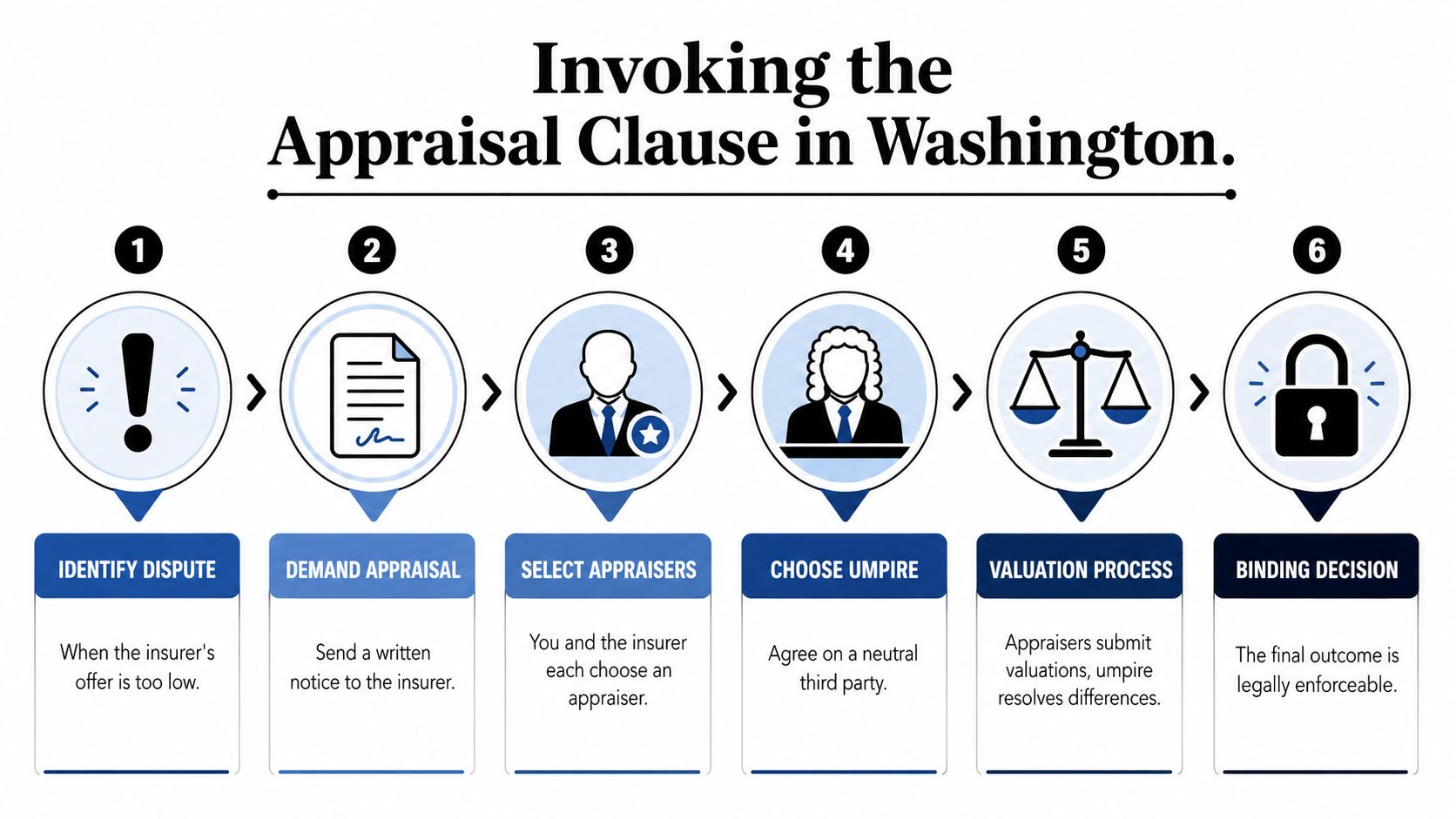

Invoking the Appraisal Clause in Washington

When negotiations stall, the Appraisal Clause is often the cleanest way to move the dispute out of the adjuster's hands and into a structured valuation process. Many drivers wait too long to use it because they assume they need the insurer's permission. They usually don't. If the policy includes an appraisal provision and the dispute is about value, that clause can become your strongest tool.

In Washington, invoking the clause begins with written correspondence to the insurer. Each side selects an appraiser. If those appraisers can't agree, an umpire can step in, and any agreement by two of the three becomes binding. Washington insurers must also pay the appraisal award within 15 days of submission, as described in this breakdown of the Washington appraisal clause process.

How to trigger the process correctly

The first move is straightforward. Send a written demand stating that you and the insurer have been unable to reach agreement on the value of the loss and that you are invoking the Appraisal Clause in the policy.

Email may work, but many experienced people still prefer a delivery method that creates a stronger paper trail. The reason is simple. When a claim gets contentious, proof of notice matters.

A practical sequence looks like this:

- Review your policy language and confirm the appraisal provision applies to your valuation dispute.

- Send a written invocation that clearly states you are demanding appraisal.

- Ask again for the valuation report if you still haven't received it.

- Select your appraiser and notify the insurer of that selection.

- Track deadlines and responses so the carrier can't slow-walk the process without accountability.

If you want a plain-language explanation of how the process works in auto claims, this page on the appraisal clause in auto insurance gives a helpful overview.

What happens after the demand

Once appraisal is invoked, each side appoints an appraiser. Those appraisers review the vehicle, the records, and the valuation support. If they agree, the dispute ends there.

If they don't agree, they submit the disagreement to an umpire. The umpire reviews the evidence and sides with one position, or lands somewhere between them, depending on the record. When any two members of that three-person group agree, the amount is binding.

That structure matters because it changes the conversation. The insurer's adjuster no longer controls the number by repeating it.

Common mistakes that weaken appraisal

A lot of drivers invoke appraisal but do it loosely. That creates avoidable problems.

Here are the mistakes I see most often:

- Vague demands: If the letter doesn't clearly invoke the clause, the insurer may pretend it was just another negotiation email.

- No supporting file: Appraisal isn't magic. You still need maintenance records, option proof, photos, and comparable support.

- Choosing the wrong appraiser: A body shop estimator and a valuation appraiser don't always do the same job well.

- Skipping the report request: Without the insurer's valuation materials, it's harder to identify where the disagreement starts.

Important distinction: Appraisal is a dispute-resolution process for value. It works best when your position is documented, organized, and tied to actual market evidence.

Why appraisal changes leverage

The Appraisal Clause works because it takes a claim that feels subjective and forces it into a method. That shift benefits prepared owners. If your evidence is stronger than the insurer's assumptions, appraisal gives that evidence a place to matter.

In Washington claim support, this is often the moment the claim stops being a take-it-or-leave-it conversation.

Working with an Independent Appraiser

A valuation dispute can look simple from the outside. The insurer says one number. You think the number should be higher. But the disagreement usually sits inside the details: condition grading, trim recognition, market selection, option treatment, and whether the final figure includes everything Washington requires.

That's where an independent appraiser earns their place. They don't just look at a damaged vehicle and guess at value. They review records, compare market evidence, identify weak assumptions, and build a report that can stand up inside a formal dispute.

The financial stakes are real

The average collision claim in the United States reached $5,489 in 2024, according to the Insurance Information Institute's auto insurance facts. That figure helps explain why valuation fights happen so often, especially when repair costs approach a vehicle's worth.

In Washington, when a vehicle is totaled, the insurer must pay Actual Cash Value including applicable government taxes and fees, and owners must report the total loss to the Department of Licensing and surrender the title within 15 days. Those details sound administrative, but they affect timing, paperwork, and the actual settlement amount.

What a skilled appraiser does that owners usually can't

An owner can absolutely gather records and challenge obvious errors. But a seasoned independent appraiser does work that untrained individuals aren't equipped to do under pressure.

That usually includes:

- Valuation analysis: Testing whether the insurer's comparables compete with your vehicle

- Condition support: Matching the vehicle's real pre-loss condition to documented evidence

- Option verification: Identifying features that valuation systems often miss or undervalue

- Report preparation: Presenting findings in a format that carries weight in negotiation or appraisal

If you're weighing whether professional help makes sense, this explanation of what an independent car appraiser does can help you evaluate the role more clearly.

What to look for before hiring one

Not every person around cars is a valuation professional. That distinction matters.

Ask practical questions. Do they work specifically on total loss and diminished value disputes? Can they explain how they review comparables? Do they understand policy appraisal language and the Washington process? Can they produce a formal report rather than just offering an opinion over the phone?

A good appraiser should make the claim clearer, not murkier. If their explanation sounds vague, argumentative, or purely sales-driven, keep looking.

The right appraiser doesn't replace your documentation. They turn your documentation into a valuation argument the insurer has to answer.

When Negotiations Fail and What's Next

Most value disputes resolve through better documentation, sharper negotiation, or appraisal. Sometimes they don't. If the insurer ignores policy language, refuses to engage with the evidence, or drags the process without explanation, escalation may be the next step.

One option is filing a complaint with the Washington Office of the Insurance Commissioner. That won't replace appraisal or private legal advice, but it can create pressure when a carrier's claim handling raises compliance concerns. Keep the complaint factual. Attach your timeline, written requests, valuation materials, and policy language if relevant.

The bigger pattern behind your claim

This isn't only a Washington problem. According to state-by-state help for Washington policyholders, 68% of policyholders in other states face underpayments from biased valuations, and 79% of drivers don't know they can invoke the Appraisal Clause to fight back.

That national context matters for one reason. If the insurer is treating your low offer like an isolated misunderstanding, it often isn't. Valuation disputes follow patterns.

When to bring in a lawyer

Legal help makes sense when the dispute is no longer just about value. If you're dealing with broader bad-faith conduct, unusual title issues, injury overlap, or a refusal to honor clear policy rights, an attorney may be the right next move.

Keep your file organized before that conversation. Lawyers can do more with a clean chronology than with a stack of scattered screenshots and half-remembered call notes.

Frequently Asked Questions About Washington Claims

Do I have to accept the insurance company's first total loss offer

No. If the valuation looks wrong, you can challenge it. The smart move is to ask for the full valuation report, review the comparables and adjustments, and respond with specific evidence instead of a general objection.

What if the accident wasn't my fault

Fault can matter for the overall claim, but a value dispute still comes down to documentation and method. If the insurer handling the total loss or property damage valuation is using weak comparables or missing equipment, those problems don't become valid just because liability is undisputed.

Can I dispute the value if my car had upgrades or exceptional condition

Yes, but proof matters. Receipts, service records, dated photos, option labels, and trim-specific documentation are what move that argument from opinion to evidence.

Is appraisal only useful for total loss claims

No. Appraisal is commonly discussed in total loss disputes, but it can also be relevant when the disagreement is about the amount of loss rather than broader coverage questions. The policy language controls, so read that section carefully.

How long should I keep claim records

Keep everything until the claim is fully resolved, payment is complete, and title issues are closed out if the vehicle is totaled. In practice, that means preserving your full file well past the first check.

What's the biggest mistake drivers make

They argue with the number before they've demanded the support behind the number. Once you have the report, the claim becomes easier to evaluate and much easier to challenge effectively.

If you're dealing with a low total loss offer or need Washington claim support that's grounded in actual valuation work, Total Loss Northwest helps drivers challenge unfair numbers with independent appraisals, diminished value support, and Appraisal Clause assistance across Washington.