When you hear an insurance adjuster mention "Fair Market Value" (FMV), what they're really talking about is the cash price your car would have sold for the moment before it was damaged.

It’s the number that matters most in your claim. Think of it less like a dictionary definition and more like a real-world snapshot of your vehicle's worth on the open market.

Defining Your Car's True Worth

Getting a solid handle on fair market value is the most critical part of any total loss or diminished value claim. This single number dictates how much the insurance company will pay you, so it's essential to understand where it comes from.

The insurer’s first offer is exactly that—an offer. It's their starting position, not a final, non-negotiable figure. The concept of FMV isn't just some random number they pull out of thin air; it’s based on the idea of a fair transaction between two people who know what they're doing and aren't being forced to make a deal.

Key Aspects of Fair Market Value

At its heart, the idea of FMV is built on a few core principles that ensure the price reflects what’s actually happening in the market. When you're dealing with an insurance claim, you're essentially the "seller," and the payout should represent a fair "purchase" price for your vehicle.

Here’s a breakdown of what that means for your claim:

- A Willing Buyer and Seller: The price is based on what a real person would have willingly paid for your car in its pre-accident condition—not some clearance or desperation price.

- No Pressure to Act: This is a theoretical sale where neither you nor the buyer is under any pressure. This prevents the insurance company from justifying a lowball number by acting like you're in a "must-sell-now" situation.

- Full Knowledge of the Facts: The FMV assumes both parties are well-informed. They know the car's exact condition, mileage, options, and any prior history.

Essentially, FMV answers one simple question: What would it have cost you to go out and buy your exact car from a private seller or a local dealer right before the accident happened?

Understanding this puts you in a much stronger position to negotiate. While you're at it, digging into various automotive blog posts can give you a broader sense of vehicle ownership and value. Your job is to make sure the insurance company's valuation truly reflects this real-world replacement cost, not just a number that saves them money.

What "Fair Market Value" Really Means

Let's cut through the jargon. When an insurance adjuster talks about your car's value, they often have a very different number in mind than you do. To get what you're owed, you first have to understand the true definition of Fair Market Value (FMV).

It’s not just some random number an insurer pulls from a database. FMV is a well-established legal and financial concept based on a simple, fair idea.

Picture this: You decide to sell your car. A potential buyer, who has been looking for your exact model, comes along. Neither of you is desperate or under any pressure to make a deal. You're both well-informed about the car's condition, mileage, and features. The price you naturally agree upon in that open, honest transaction? That's the essence of Fair Market Value.

At its core, FMV is all about retail replacement cost. It's the answer to one simple question: "How much money would I need today to go to a local dealership and buy a car just like the one I lost?" It has nothing to do with what a dealer would offer you for a trade-in or what your car might fetch at a wholesale auction.

Where Does This Definition Come From?

This isn't just industry-speak; it's a concept with deep roots in law and finance. The whole point of FMV is to create a level playing field, making sure that a vehicle's worth is set by the open market, not by one party who has a financial incentive to lowball the number.

The term "fair market value" actually goes way back, first appearing in the U.S. Revenue Act of 1918. It was later cemented by Revenue Ruling 59-60, which made it the benchmark for valuations in everything from IRS disputes to court cases. The Supreme Court even weighed in, confirming that FMV is what’s determined in an "arm's-length" transaction—a deal where no one is being forced or pressured. You can dig deeper into the fundamentals of Fair Market Value and its history if you're curious.

This legal foundation is your biggest advantage. An insurance company can't just make up a number; they are supposed to follow a standard that reflects a fair, real-world sale.

The Bottom Line: Fair Market Value is not your car's trade-in or wholesale value. It's the retail price you would have to pay to buy a comparable replacement vehicle from a dealer in your area.

Why This Is a Game-Changer for Your Claim

Grasping this one concept is the single most powerful tool you have when negotiating with an insurer. Most insurance companies will slide an initial offer across the table that feels final, but it's often based on valuation reports that lean heavily on wholesale prices or auction data. Remember, they're running a business, and minimizing claim payouts is part of their model.

When you insist that the valuation reflects the true retail replacement cost, you're not being difficult—you're simply holding them to the correct, legally recognized standard.

Here’s what that means for your claim in simple terms:

- It’s About Replacement: The goal is to make you "whole," meaning you should have enough cash in hand to buy a similar car.

- It’s About Local Prices: The value has to be based on what comparable cars are actually selling for near you, not some national average or a market in another state.

- It’s an Apples-to-Apples Deal: The valuation must compare your vehicle to others with similar mileage, options, and overall condition.

Knowing this empowers you to push back on a lowball offer. This isn't just about getting a good deal; it's about getting the full amount you're owed so you can get back on the road in a car just like the one you lost.

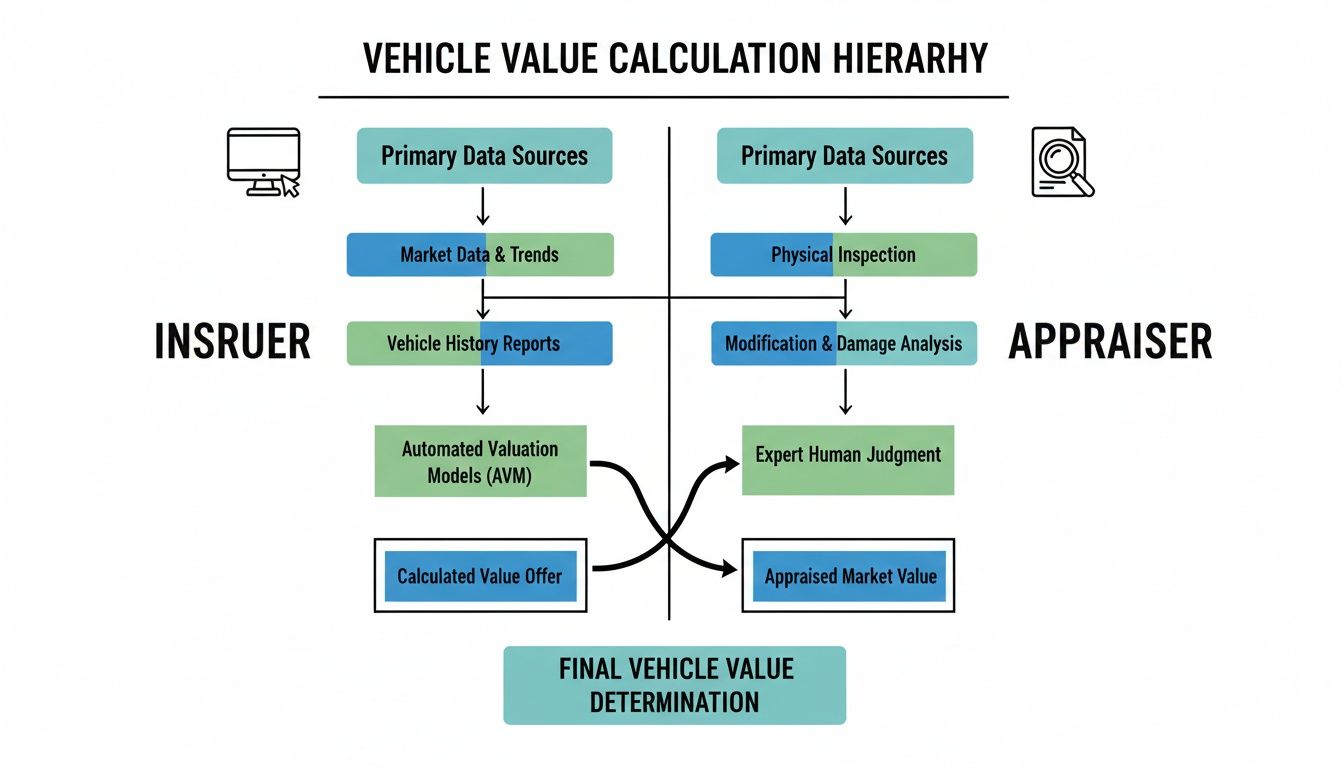

How Insurers Actually Calculate Your Car's Value

Ever wonder how your insurance adjuster comes up with their settlement offer? They don't just pull a number out of thin air. In most cases, they're using third-party valuation software. One of the biggest names in the game is CCC Intelligent Solutions (formerly CCC ONE), a platform built to process a massive volume of claims with speed and consistency.

This software acts like a giant data scraper, pulling information from sources like dealer sales data and auction results to spit out a baseline value. It’s a system designed for efficiency, crunching numbers on an industrial scale.

But here’s the catch: this automated approach often leans heavily on wholesale data. That’s the price cars fetch at auction or what a dealer might pay for a trade-in, not what you’d have to pay to buy a replacement off a local lot. It's a system built for volume, not for accuracy in your specific situation.

The Algorithm vs. The Appraiser

This is where the insurance company's method and a real, independent appraisal part ways—dramatically. While their software casts a wide, generic net, a certified appraiser gets out a magnifying glass. An appraiser's job isn't to be fast; it's to be right.

They start by digging into your local retail market. Forget national averages or auction prices from three states away. They look for comparable vehicles—the same make, model, year, and trim—for sale at dealerships near you. This is the only way to figure out what it would actually cost you to replace your car today. To see this process in more detail, check out our guide on calculating a vehicle's total loss value.

An independent appraisal hinges on the key details that automated systems almost always overlook:

- Pre-Accident Condition: Was your car garage-kept and in pristine shape? Did it have unusually low mileage? Those things matter.

- Optional Packages: That premium sound system, sunroof, or tow package you paid extra for can add thousands to a car's fair market value.

- Local Market Demand: A four-wheel-drive SUV is going to be worth a lot more in Denver than it is in Miami. A good appraiser knows your local market inside and out.

The Real-World Value Gap

This fundamental difference in approach is precisely why an insurer’s first offer can feel like a lowball. To a professional appraiser, FMV isn't a guess; it's a number backed by hard, verifiable evidence from the real world.

For example, a 2021 NADA guide showed the clean retail FMV for a 2018 Ford F-150 hovering around $35,000. Yet, it wasn't uncommon for insurers to offer settlements closer to a $28,000 trade-in value. That’s a 20% gap coming directly out of your pocket.

The difference is stark: an insurer's algorithm values a generic version of your car, while an independent appraiser values your specific car in your specific market.

And that distinction is everything. An algorithm doesn't know about the immaculate leather interior you maintained or that rare sport package from the factory. An independent appraiser builds their entire report around these critical details to prove your vehicle's true worth and make sure you get the settlement you’re entitled to.

Decoding FMV vs. ACV and Other Insurance Jargon

When you're dealing with an insurance claim, a whole new vocabulary gets thrown at you. You'll hear terms like Fair Market Value (FMV), Actual Cash Value (ACV), Retail Value, and Trade-In Value, and it's easy to assume they all mean the same thing.

They absolutely do not.

Understanding the subtle—and not-so-subtle—differences between these terms is the key to protecting your financial interests. Each one represents a different dollar figure, and knowing which one applies can mean thousands of dollars in your pocket.

The biggest point of confusion usually boils down to FMV vs. ACV. Your insurance policy is probably full of references to "ACV," but this is where the games often begin. If you're trying to figure out the value of a totalled car using ACV, you need to know what that term really means.

ACV vs. FMV: The Critical Difference

Here’s the inside scoop: in many states, the legal definition of Actual Cash Value is required to be the same as Fair Market Value. In plain English, that means your ACV payout should be what it would cost to buy a comparable replacement vehicle from a local dealer. It's the retail price.

So, where's the problem? Some insurance adjusters will use the term "ACV" to justify an offer that looks a lot more like a wholesale or trade-in value. They're banking on the fact that most people won't know the difference.

This little trick results in a settlement offer that isn't nearly enough to actually replace your car, forcing you to pay the difference out-of-pocket. For a deeper dive, you can learn more about how this works in our guide on the actual cash value of a car at https://totallossnw.com/what-is-actual-cash-value-of-my-car/.

Key Takeaway: When it comes to your claim, "Actual Cash Value" should equal "Fair Market Value." This isn't the trade-in number or some auction price; it’s the retail replacement cost. Knowing this is your first line of defense against a lowball offer.

The flowchart below gives you a bird's-eye view of how differently an insurer and a professional appraiser approach the valuation process.

As you can see, an insurer's automated system often misses the real-world, market-specific details that a hands-on appraiser will catch.

Comparing Key Valuation Terms

To make this crystal clear, let's put these terms side-by-side. The table below breaks down the key differences between the most common valuation terms you'll see in an insurance claim.

| Valuation Term | What It Represents | Typical Value (Example: $20,000 Car) | Who Uses It |

|---|---|---|---|

| Fair Market Value (FMV) | The price a willing buyer would pay a willing seller in a free market. It's the real-world retail price. | $20,000 | Courts, Appraisers, IRS, Insurance (should be the standard) |

| Actual Cash Value (ACV) | Your vehicle's pre-loss value, accounting for depreciation. Legally, it should align with FMV. | Should be $20,000 | Insurance Companies |

| Retail Value | The price a dealer lists a similar car for on their lot. This is effectively the same as FMV. | $20,000 | Car Dealerships, Consumers, Appraisers |

| Private Party Value | The amount you'd get selling the car directly to another person, without a dealer involved. | $18,500 | Private Sellers/Buyers, Car Buying Guides |

| Trade-In Value | The lowest value, representing what a dealer offers as credit toward another car purchase. | $16,000 | Car Dealerships |

Seeing the numbers laid out like this really shows you what's at stake.

This valuation hierarchy is your best defense. When an adjuster comes back with a settlement based on "ACV," your first question should be, "Is this figure based on retail replacement cost, or is it closer to a trade-in value?" The difference could be the thousands of dollars you are rightfully owed.

Putting Fair Market Value into Practice

Knowing the definition of fair market value is one thing. Seeing how it works in a real insurance claim is where the rubber really meets the road. Let's walk through two common situations where understanding your vehicle's true FMV can make a huge difference—often to the tune of thousands of dollars.

These examples aren't just hypotheticals; they reflect what happens every day. They show why an insurer's first offer is just that: an offer. It's the starting point of a conversation, not the final word.

Example 1: The Totaled Family SUV

Picture this: a family's beloved SUV, kept in great condition, gets totaled in a wreck. The insurance company acts fast, which seems great at first, and comes back with a settlement offer of $18,500. But the number just doesn't feel right to the owners. They know their SUV was special—it had the top-tier tech package, a huge panoramic sunroof, and incredibly low mileage for its model year.

So, they ask for the insurer's valuation report. It turns out the value was spit out by an automated system that pulled "comparable" vehicles from a massive statewide database. The problem? The computer missed the details that made their SUV worth more.

- It completely ignored the $3,000 premium package.

- The so-called "comps" had, on average, 30,000 more miles.

- Two of the listed comps were from a different city where cars sell for much less.

Not willing to accept the lowball offer, the family decides to use the Appraisal Clause in their policy and hires a certified independent appraiser. This appraiser does the real legwork. He builds a new report based on the SUV's actual features and what similar vehicles are selling for right now, in their local area.

He quickly finds three nearly identical SUVs for sale at dealerships within a 50-mile radius. Their asking prices? Between $22,000 and $23,500.

Armed with this specific, local, and verifiable evidence, the appraiser submits his report. After a brief negotiation between the appraiser and the insurer's representative, the final settlement is adjusted to $22,750—a $4,250 increase over the initial offer.

This is a perfect illustration of how FMV isn't some abstract number. It's tied directly to what it would cost you to buy a truly comparable replacement vehicle in your local market.

Example 2: The Diminished Value Claim

Now let's look at a different scenario. A fairly new truck gets into a nasty accident, but it's repairable. The body shop does an amazing job, and cosmetically, the truck looks perfect. The at-fault driver's insurance covers the entire $11,000 repair bill. Case closed, right?

Not quite. The truck now has a permanent accident history on its record. A year later, when the owner goes to trade it in, the dealer’s offer is a shock. It's $6,000 less than the going rate for an identical truck with a clean history. The dealer points to the "inherent diminished value" caused by the accident.

This loss in resale value is a real, tangible loss, and it's something you can be compensated for. The owner files a diminished value claim, but the insurance company's initial offer is a measly $1,500.

To prove the actual loss, the owner brings in an appraiser who specializes in diminished value. The appraiser first establishes the truck's pre-accident fair market value, which was $45,000. Then, by analyzing the severity of the damage and pulling data from local auto auctions and dealer networks, he calculates that the accident caused a 15% drop in the truck's FMV.

The math is simple: $45,000 (Pre-Accident FMV) x 0.15 (Diminished Value Percentage) = $6,750.

The appraiser submits a detailed report backing up this calculation with hard market evidence. Faced with a professional, well-supported claim, the insurer raises its offer significantly, and they settle on $6,200. This shows that FMV isn't just for total loss—it’s also the critical baseline for calculating the value your vehicle has lost, even after it’s been perfectly repaired.

How to Dispute a Low Insurance Offer

When your insurance company slides a settlement offer across the table for your totaled car, it can feel like a final, take-it-or-leave-it command. But here’s the thing: you have way more power than you realize. Fighting a lowball offer that ignores your car's real fair market value isn't just an option—it's your right.

Your first move is to formally reject their offer, and you need to do it in writing. A straightforward, professional email is perfect. Just state that you don't accept their valuation and that you'll be providing more information to support your claim. This simple act puts them on notice that you're not going to be pushed around.

Gather Your Evidence

Now, it's time to build your case. You can't just tell the adjuster their offer is too low; you have to show them. This is where you pull together every piece of paper that proves your vehicle's true condition and value right before the accident. Think of it as painting a complete picture of the car they never saw.

The kind of documentation that makes a real difference includes:

- Maintenance Records: A stack of receipts for regular oil changes, tire rotations, and tune-ups proves your car was well-maintained, not neglected.

- Recent Repairs or Upgrades: Did you just drop $1,200 on a new set of premium tires? Or maybe you installed a new audio system? Every invoice adds to its pre-accident value.

- Original Window Sticker: If you still have it, the Monroney label is gold. It lists every single factory option and package that set your car apart from the base model.

Invoke the Appraisal Clause

This is your secret weapon. Tucked away in the fine print of most auto policies is a provision called the Appraisal Clause. This powerful clause is your contractual right to bring in an unbiased, third-party expert if you and your insurer can't agree on the vehicle's value.

Invoking the Appraisal Clause takes the negotiation out of the hands of the insurance company's adjuster. It shifts the power to independent professionals who are only focused on one thing: determining an accurate and fair market value.

To get this process started, you'll need to hire a certified independent appraiser. Their entire job is to conduct a thorough investigation and produce a detailed report establishing your vehicle’s pre-accident FMV using real, local market data. This isn't just an opinion—it's an evidence-backed valuation that forces the insurer back to the negotiating table with a number that reflects reality.

You can get a deeper understanding of how to manage auto insurance appraisals to make sure you’re ready for every step.

Common Questions About Fair Market Value

Going head-to-head with an insurance company over your car's value can feel a bit overwhelming, and it naturally brings up a lot of questions. Getting clear on the answers is the best way to walk into the process with your eyes open, knowing exactly what to expect.

Can I Just Use an Online Estimator Like KBB for My Claim?

It's a great question, and one we hear all the time. Think of tools like Kelley Blue Book as a good first step—a way to get a ballpark idea of what your car might be worth. They give you a general sense of the market.

But when it's time to actually dispute an insurance company's offer, those online numbers just don't cut it. Insurers won't take a KBB printout seriously. They require a formal, certified appraisal report that's built on real, local, and verifiable "comps" (comparable vehicles) to establish a value they can't easily dismiss.

My Car Is Older. Is It Even Worth Disputing a Low Offer?

Absolutely. In fact, older cars are often where we see some of the biggest wins for our clients. The market for solid, reliable used cars is incredibly strong right now, yet insurance companies frequently lowball these vehicles by default.

An independent appraiser digs into the details that matter: your car's specific condition, its maintenance history, and what similar cars are actually selling for in your neighborhood. This deep dive often uncovers hundreds or even thousands of dollars in hidden value, proving what fair market value truly means for your specific vehicle.

If you're staring at a lowball offer for a total loss or diminished value claim, don't just accept it and leave money on the table. The team at Total Loss Northwest specializes in one thing: providing certified, independent auto appraisals that give you the leverage to get paid what you're rightfully owed.

Get a fair and accurate settlement by visiting us at https://totallossnw.com.