Think of liability insurance as your financial bodyguard. It's the policy that steps in to cover the legal costs and financial payouts you're responsible for if you cause injury or damage to someone else. It's the safety net that protects your personal and business assets when an accident turns into a lawsuit.

Your Financial Shield Against The Unexpected

Let's paint a picture. Your business is doing great, but then the unexpected happens. A customer slips on a freshly mopped floor, a product you sold has a defect and causes harm, or a simple mistake in your professional advice costs a client a fortune.

Suddenly, you're facing a lawsuit that could jeopardize everything you've built. This is exactly where liability insurance becomes so critical. It acts as a financial buffer, standing between the high costs of a legal claim and your hard-earned assets.

Essentially, this insurance is designed to handle the legal defense fees and any settlements or judgments you are legally required to pay when found responsible for hurting someone or damaging their property.

Understanding this type of protection is a fundamental piece of the broader concept of risk management planning—a strategy focused on identifying and neutralizing potential threats before they can cause serious harm.

A single liability claim can be financially devastating. You could face tens of thousands of dollars in legal fees alone, even if the court ultimately decides you weren't at fault.

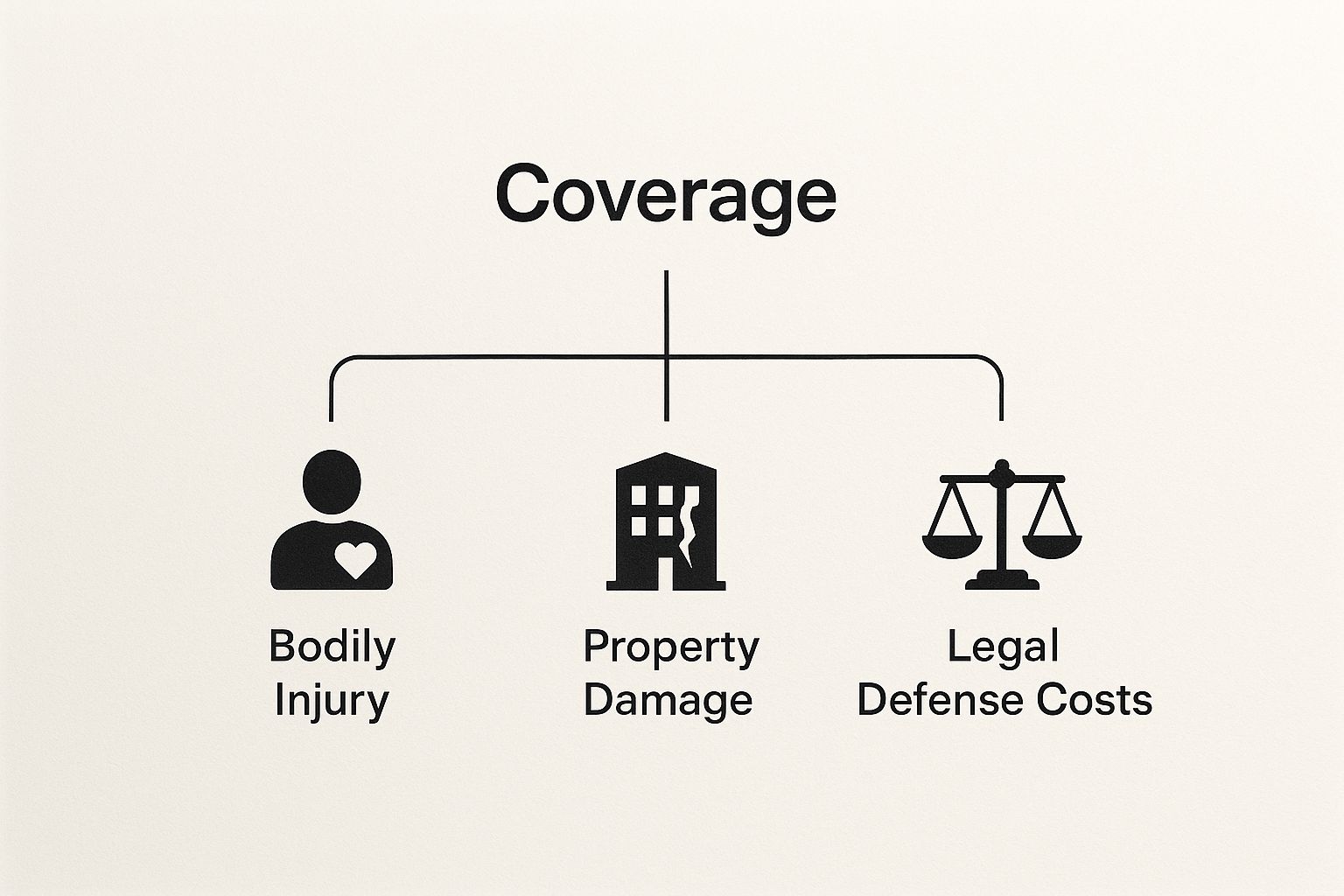

To help you get a clearer picture, here’s a quick breakdown of what standard liability insurance typically covers.

Liability Insurance At a Glance

| Coverage Area | What It Typically Includes |

|---|---|

| Bodily Injury | Medical expenses, loss of income, and pain and suffering for someone injured due to your negligence. |

| Property Damage | Costs to repair or replace another person's property that you or your business damaged. |

| Legal Defense | Attorney fees, court costs, and other legal expenses needed to defend you against a covered lawsuit. |

| Judgments & Settlements | The final amount awarded to the other party by a court or agreed upon in a settlement, up to your policy limits. |

These core protections are what make liability insurance such an indispensable tool for both individuals and business owners.

Being prepared for the unexpected is always a smart move. You can learn more about different protection strategies and how the claims process works by exploring our collection of helpful insurance resources.

The Core Protections of Liability Insurance

When you get right down to it, liability insurance is really built on two main safeguards. Think of them as the twin pillars holding up your financial safety net, protecting you from the most common (and costly) claims you might face in the course of doing business.

At its core, liability coverage is all about Bodily Injury and Property Damage that you might cause to other people—what the insurance world calls "third parties." These aren't just legal terms on a policy document; they're real situations that happen every single day. Let's break them down with some practical examples.

Bodily Injury Coverage Explained

This is the part of your policy that kicks in when your business operations, your property, or even your own actions lead to someone getting physically hurt. And it’s not always about some catastrophic accident; even a minor slip-up can snowball into a massive claim.

The classic example is a customer slipping on a wet floor in your shop. If they break an arm, your Bodily Injury coverage is what handles the fallout. This can include a whole range of expenses:

- Medical Bills: Covering everything from the ambulance ride and ER visit to surgery and ongoing physical therapy.

- Lost Wages: Reimbursing the injured person for the income they lost because they couldn't work.

- Legal Defense: Paying for the lawyers needed to defend you if a lawsuit is filed.

Without coverage, you’re on the hook for all of it. Those costs can easily climb into the tens or even hundreds of thousands of dollars, threatening everything you've worked for.

Property Damage Coverage in Action

The second pillar, Property Damage coverage, steps in when you're responsible for damaging, breaking, or otherwise destroying something that belongs to someone else. If you ever work with client property or operate on their premises, this coverage is absolutely non-negotiable.

Picture this: you're a painter working in a client's living room. You accidentally trip and spill a full can of paint all over their priceless antique rug. That's a textbook property damage claim.

Your liability policy is designed for exactly this kind of honest mistake. It would pay to have the rug professionally restored or, if it’s ruined beyond repair, cover the cost to replace it.

Together, Bodily Injury and Property Damage are the foundation of any solid general liability policy. They’re what stand between a simple accident and a potential financial disaster for your business.

Specialized Coverage for Unique Professional Risks

A standard general liability policy is a great starting point, but it's not a one-size-fits-all solution. Some professions carry risks that just aren't covered by a basic plan.

Think of it this way: your family doctor is perfect for an annual check-up, but you'd want a cardiologist if you had a serious heart condition. Specialized liability insurance is the same concept—it’s designed for the specific, high-stakes risks inherent in certain lines of work. These policies step in where general liability stops, covering things like professional errors, faulty products, or even management-level decisions that cause financial harm.

Tailored Policies for Specific Industries

One of the most essential types is Professional Liability Insurance, which you'll often hear called Errors & Omissions (E&O) coverage. This is non-negotiable for anyone who gets paid for their advice or services—think architects, consultants, accountants, and IT professionals. It protects them if a client sues for negligence, a costly mistake, or a failure to deliver on professional promises.

Imagine an IT consultant makes an error that causes a client's entire network to crash, leading to a massive data breach. E&O insurance would be what covers the expensive legal battle and any resulting settlement. Without it, the consultant's personal assets could be completely wiped out.

Another critical one is Product Liability Insurance. This is for any business involved in making, distributing, or selling a physical product. If that product has a defect that injures someone or damages their property, this coverage kicks in to handle the claims.

Protecting the People in Charge

Finally, there’s Directors & Officers (D&O) Insurance. This policy shields the personal assets of a company's executives and board members from lawsuits stemming from their management decisions. If shareholders or employees sue them for mismanagement, D&O insurance covers their defense costs and potential settlements.

These specialized policies are a huge part of the U.S. insurance landscape, which is projected to see over $1.9 trillion in premiums by 2035. It's a massive number that really drives home just how critical this kind of protection has become for businesses.

Of course, insurance isn't the only tool in the box. Many businesses also lean on legal instruments to manage risk, and it’s worth looking into the common considerations for using a liability waiver in your business.

Demystifying Your Policy Limits and Deductibles

Having liability insurance is a great first step, but the real peace of mind comes from knowing exactly where its financial protection begins and ends. To get that clarity, you need to understand two key numbers on your policy: your limits and your deductibles. These figures determine how much your insurance company will pay versus how much you'll pay out-of-pocket when a claim arises.

Think of your policy limit as the maximum amount of money your insurer has agreed to pay on your behalf. This cap is typically broken down in two ways:

- Per-Occurrence Limit: This is the absolute most your insurer will pay for a single, individual claim.

- Aggregate Limit: This is the grand total your insurer will shell out for all claims combined during your policy period, which is usually one year.

If a claim's costs blow past these limits, you're on the hook for the difference. It’s a critical detail that can have massive financial consequences if your limits are too low.

What You Pay First: Your Deductible

The other side of the coin is your deductible. This is your share of the cost—the amount you have to pay before your insurance coverage even kicks in.

Let’s say you have a covered claim that totals $20,000, and your policy has a $1,000 deductible. You would pay the first $1,000, and then your insurer would cover the remaining $19,000.

It's a trade-off. Choosing a higher deductible can lower your monthly premium, which feels great on the wallet. But it also means you’ll face a bigger upfront expense if you actually need to use your insurance. It's all about finding that sweet spot. The same goes for understanding how your insurer values your property; for instance, it’s helpful to know how the actual cash value of your car is calculated after an accident.

A crucial reason to pay close attention to your policy limits is the rise of "nuclear verdicts"—jury awards that can easily exceed $10 million. These massive settlements are a major factor driving up insurance costs and highlight just how important it is to have enough coverage to protect your assets. You can read more about how large settlements impact the insurance industry on InsuranceJournal.com.

Common Exclusions: What Liability Insurance Won't Cover

It’s tempting to think of liability insurance as a magic shield that protects you from any and all financial mishaps. But that’s a common—and potentially costly—misconception. This insurance is designed for a specific purpose, and understanding what it doesn’t cover is just as critical as knowing what it does.

Think of it as a specialized tool in your financial toolkit, not an all-purpose wrench. It's built to handle accidental harm you cause to others, which means some big categories of risk are intentionally left out.

Intentional and Criminal Acts

This one’s at the top of the list for a reason. If you or someone at your company deliberately harms a person or their property, your liability insurance won’t touch it. The core of these policies is to cover accidents and negligence, not malicious or willful misconduct.

Along the same lines, any liability stemming from a criminal act is a definite exclusion. Insurance is there to manage unexpected risks, not to cushion the financial fallout from breaking the law. If a claim arises because a crime was committed, the insurer will deny it.

Damage to Your Own Property

This is a frequent source of confusion. General liability insurance is all about protecting you from claims for damage you cause to other people's stuff, not your own.

Picture this: a pipe bursts in your office, damaging your computers and desks. That’s a claim for your Commercial Property Insurance. But if that same burst pipe floods the office next door, your General Liability policy is what steps in to cover their damages.

This separation is fundamental. Your own assets need their own dedicated coverage.

Covered vs. Not Covered: A Quick Guide

To make this crystal clear, let's look at a few common scenarios. This table breaks down what typically falls under a general liability policy and what requires a different type of insurance.

| Scenario | Typically Covered by Liability Insurance? | Relevant Insurance Type |

|---|---|---|

| A customer slips on a wet floor in your store. | Yes | General Liability |

| Your employee gets injured lifting a heavy box. | No | Workers' Compensation |

| A fire you caused spreads to a neighboring shop. | Yes | General Liability |

| That same fire damages your own equipment. | No | Commercial Property |

| A company vehicle is involved in an at-fault accident. | No | Commercial Auto |

| You deliberately break a client's equipment out of anger. | No | N/A (Intentional Act) |

As you can see, each policy has a distinct job to do. Relying on one to cover everything leaves you exposed.

Other Common Gaps in Coverage

Beyond those big categories, a few other specific exclusions often show up in policies:

- Contractual Liability: If you sign a contract where you agree to assume the liability of another party, your standard policy probably won't cover it. It’s designed for your own negligence, not for risks you voluntarily take on.

- Employee Injuries: On-the-job injuries to your team are the exclusive domain of Workers' Compensation Insurance. This is a mandatory coverage in most states for a reason.

- Auto Accidents: Any liability from accidents involving your business vehicles falls under a separate Commercial Auto Insurance policy.

Getting a handle on these exclusions is the first step toward creating a truly solid financial safety net for your business. It ensures you don't have any surprise gaps in your protection. Navigating insurance claims can be tricky, especially when it comes to auto incidents, which is why it's so important to understand the specifics of how to file a diminished value claim to ensure you get everything you're entitled to.

Let's Tackle Your Biggest Liability Insurance Questions

Okay, we've covered the basics. But the real world is messy, and that's where the important questions always come up. When you're trying to protect your business or your assets, you need practical answers, not textbook definitions.

Let's dive into the questions I hear most often from business owners and individuals trying to make sense of their liability coverage. My goal here is to cut through the jargon and give you the straightforward answers you need to make smart decisions.

How Much Liability Insurance Do I Actually Need?

This is the million-dollar question—sometimes literally. There's no magic number, and anyone who tells you there is isn't giving you the whole picture. The right amount of coverage really boils down to your specific situation: your industry, the risks you face every day, and even what your clients demand in their contracts.

A freelance graphic designer might be perfectly fine with a $1 million policy. But a general contractor working on a commercial building site? They're facing much bigger potential accidents and will likely need $5 million in coverage, or possibly even more.

The best way to figure this out is to do an honest risk assessment. What's the worst-case scenario? What could a major lawsuit cost you? It’s always a good idea to chat with an experienced insurance broker. They’ve seen it all and can help you find that sweet spot—enough coverage to let you sleep at night, but not so much that you're wasting money.

Are General Liability and Professional Liability the Same Thing?

Not at all. This is probably one of the most common and dangerous mix-ups I see. They cover two completely different kinds of risk, and you might need both.

-

General Liability: Think of this as your "oops, I broke something" or "oops, someone got hurt" policy. It’s for physical, tangible harm—the classic slip-and-fall, a piece of equipment damaging a client's property, that kind of thing.

-

Professional Liability: This is often called Errors & Omissions (E&O) insurance. It protects you from claims that your advice, expertise, or professional services caused a client a financial loss.

For example, if an architect's design flaw leads to costly rework, that’s a professional liability claim. If a visitor trips over a blueprint at their office and breaks an arm, that's a general liability claim.

The simplest way to remember it: General liability covers physical harm. Professional liability covers financial harm from your work.

Will My Homeowners Insurance Cover My Home-Based Business?

I can't be clearer on this: absolutely not. Your standard homeowners policy comes with personal liability protection, which is great if a friend slips on your icy porch during a holiday party. But the moment an incident is related to your business—even a tiny Etsy shop run from your spare room—that coverage disappears.

Your policy has a specific exclusion for all business-related activities. If a client comes to your home for a meeting and trips, or a product you sell from your garage causes an injury, your homeowners insurance won't help you. You need a separate commercial general liability policy. Trying to skate by on your home insurance leaves a massive, potentially ruinous gap in your protection.

Navigating an insurance claim after a major accident can be a nightmare. When it comes to a total loss or diminished value claim for your vehicle, don't just accept the first lowball offer the insurer throws at you. At Total Loss Northwest, we provide certified, independent auto appraisals to make sure you get the full compensation you deserve. Learn more about how we can help you fight for a fair settlement.