Your car is totaled. Now what? The tow truck has left, the adjuster is talking about actual cash value, and you're already realizing the insurance company has a process ready for you. What many drivers miss is that the insurer's process is built to close the claim efficiently. It is not built to maximize what lands in your pocket.

That matters because a total loss is usually a financial decision, not a mechanical one. Insurers commonly total a vehicle when repair costs reach roughly 70% to 80% of its actual cash value, though state rules and carrier methods vary, and some use a total-loss formula instead of a straight percentage, as explained by GEICO's overview of totaled cars. Once that happens, the settlement usually turns on the car's pre-accident actual cash value, not what you paid, not what you owe, and not what it will cost you to replace it.

That's where people get hurt financially. A low valuation, weak comparable vehicles, missing options, or ignored maintenance history can drag down the offer fast.

If you're dealing with a personal claim or managing Tampa Bay fleet collisions, the first steps matter. Handle this correctly and you can challenge a low number with evidence. Handle it casually and you may lock yourself into a settlement that doesn't come close to making you whole.

1. Document the Accident Scene and Vehicle Damage Immediately

The first battle in a total loss claim is the record. If the insurer's file starts with a sparse tow-yard photo and a brief adjuster note, you've already given away your advantage.

Put together your own evidence before the vehicle is moved, cleaned up, stripped, or exposed to more damage. That means wide shots, close-ups, interior photos, wheel and suspension views if visible, deployed airbags, glass damage, fluid leaks, and any visible mechanical issues. Capture the odometer and VIN tag too.

What to capture before the insurer frames the story

A lot of valuation disputes start with language like “moderate damage” or “prior wear consistent with age.” Photos let you challenge that. If the impact pushed the rear body structure, buckled a quarter panel, disturbed alignment, or damaged interior safety components, your images can show the severity in a way a summary line never will.

I also tell drivers to record one slow walkaround video. Narrate the date, location, and what you're seeing. If the steering wheel is off-center, if a door won't latch, if warning lights are on, say it on camera.

Practical rule: If you can see it, photograph it. If you can describe it, record it.

A solid post-crash record also helps when you're following steps to take after a car accident and preparing for the total loss fight that may follow.

Preserve the file like evidence

Don't leave the only copy on your phone. Upload everything to cloud storage the same day and keep the original file names and metadata intact if possible.

Use this short capture list:

- Shoot all four corners: Photograph front, rear, both sides, and angled views.

- Document identity details: Include the VIN plate, license plate, and odometer.

- Show the cabin: Photograph airbags, seats, dash warnings, and infotainment if impacted.

- Save originals: Keep unedited files in cloud storage and on a second device.

A quick visual guide can help if you're doing this under stress.

2. Understand Your Insurance Policy and Total Loss Definition

Many drivers make a costly mistake early. They assume “totaled” has one universal definition and that the insurer's conclusion must be final. It doesn't work that way.

Policies, state rules, and carrier procedures interact. Some insurers use a percentage threshold. Some states apply different legal standards. Some carriers use a formula that factors salvage value into the decision. Kelley Blue Book explains that total-loss handling can vary by state and by insurer, and that owners should review the valuation details closely through the Kelley Blue Book guidance on totaled cars.

Find the language that controls the claim

Pull the full policy, not just the declarations page. You're looking for the valuation language, the loss settlement provision, any appraisal clause, deductible language, and any specialty endorsement if the vehicle is collector, agreed value, or stated value insured.

If you own something unusual, the policy matters even more. A daily driver on standard actual cash value coverage is one thing. A restored truck, performance car, or specialty vehicle may have endorsements that change how value should be handled.

What works is reading the contract before you argue. What doesn't work is calling the adjuster and saying the number “feels low” without knowing what the policy allows.

Questions that usually expose weak handling

Ask the insurer these questions in writing:

- What definition was applied: Ask whether the carrier used a threshold method or total-loss formula.

- What valuation method was used: Request the full worksheet, not a summary.

- What coverages control value: Confirm whether the policy is actual cash value, stated value, or agreed value.

- What deductions apply: Verify the deductible and any salvage-related deduction if you keep the vehicle.

Your leverage improves the moment you stop arguing feelings and start asking for the exact policy and valuation language the insurer relied on.

If the representative can't explain the basis clearly, slow the process down. A rushed total loss is often a poorly supported one.

3. Obtain an Independent Professional Appraisal

If the insurer's number looks wrong, stop relying on the insurer to fix its own valuation. Bring in an independent appraiser.

That step matters most when the vehicle has unusually strong condition, low mileage for its age, rare trim, premium options, documented upgrades, collector appeal, or a local market value that generic software often misses. In those claims, the fight usually turns on evidence quality, not on who complains the loudest.

What an appraiser should actually do

A real appraisal is not a guess and it isn't a printout with a number at the bottom. The appraiser should inspect the vehicle record, verify trim and options, assess condition, review maintenance and upgrades, and analyze comparable vehicles that reflect your market.

That independent work becomes even more important because the insurer's settlement is based on pre-loss value, not what you originally paid or what your loan balance says. If options are missing, condition is understated, or the comparable vehicles are poor matches, the settlement drops. That's why Kelley Blue Book emphasizes requesting the valuation worksheet and verifying its inputs in the same totaled-car guidance noted earlier.

If you want a practical breakdown of the process, this explanation of what a car appraisal is is directly relevant.

When this step makes the biggest difference

Independent appraisals are especially useful when:

- The vehicle is not ordinary: Collector, luxury, performance, or limited-production vehicles rarely fit neatly into insurer software.

- The condition was above average: Detailed maintenance history and strong cosmetic condition can move value meaningfully.

- Upgrades matter: Quality wheels, suspension, audio, paintwork, restoration, or factory options may be overlooked.

- The comparable vehicles look weak: If the insurer used bad comps, a professional can challenge them with better local market evidence.

What works is hiring someone who knows your vehicle category. What doesn't work is pulling random listings online and calling that an appraisal.

4. File a Claim and Notify Your Insurer Promptly

Prompt notice protects your position. It creates a clean timeline, gets the claim moving, and prevents the insurer from arguing that delayed reporting complicated the investigation.

When you call, stick to facts. State where the crash happened, when it happened, who was involved, where the vehicle is located, and whether it's drivable. Don't speculate about fault, speed, injuries you haven't had evaluated, or damage you haven't confirmed.

Control the communication from day one

Every conversation with the insurer should leave a paper trail. Get the claim number, the adjuster's full name, direct phone number, and email address. Then send a short email confirming the basics of the conversation.

That simple follow-up often cleans up later disputes. Verbal statements get fuzzy. Written records don't.

Use a communication log with the date, time, who you spoke with, and what was said. If an adjuster promises to send the valuation report, note it. If the tow yard charges storage, note it. If the insurer says they still need documents, note exactly which ones.

What to ask for right away

Before the claim gets too far down the road, request these items:

- Written claim confirmation: Make sure the loss is opened and tied to the correct vehicle.

- Valuation process details: Ask how the insurer determines actual cash value in total loss claims.

- The complete valuation report: Don't settle for a one-line offer.

- Instructions on next steps: Confirm title, lienholder, storage, rental, and salvage procedures.

Ask early, in writing, for the full valuation worksheet. Waiting until after the offer arrives usually costs time and leverage.

This is also the stage where drivers often discover how industrialized the process has become. Industry summaries cited by Total Loss Appraisals note that many insurers use a repair-cost threshold around 70% to 75% of actual cash value, with some sources citing 70% to 80% depending on insurer and state. The practical takeaway is simple. Your claim is moving through a system. You need your own documentation inside that system.

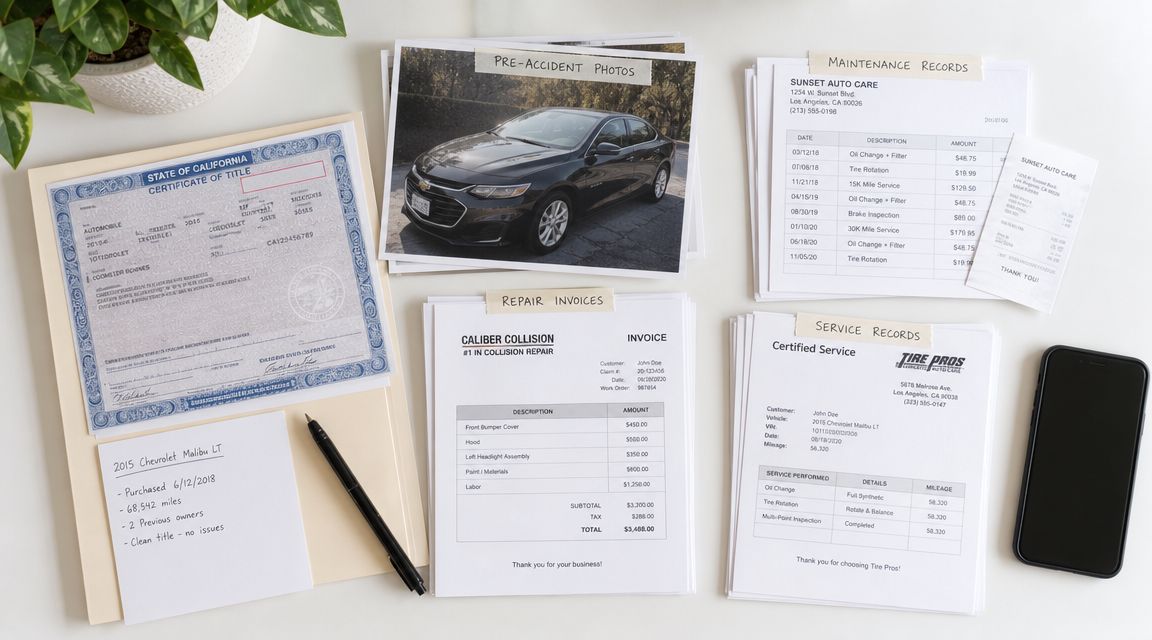

5. Gather Complete Vehicle History and Documentation

A strong total loss challenge is built on paperwork. If you want a better valuation, prove the vehicle deserved one.

Start with title, registration, payoff information if there's a lien, service history, repair invoices, parts receipts, warranty documents, inspection records, and recent photos from before the crash. If the vehicle had new tires, major maintenance, recent bodywork, restoration, or dealer-installed options, collect those records too.

Why records change the number

Insurance valuations are only as good as the inputs. If the report treats your vehicle like an average example with average care, you need records that show otherwise.

Maintenance records help establish condition. Receipts for recent work help show the car wasn't neglected. Build sheets, option stickers, and original purchase documents can help verify equipment the insurer may have missed.

Owners of custom and specialty vehicles usually have an opportunity here. A standard valuation platform may not fully capture rarity, high-end condition, or meaningful equipment differences. That risk matters even more in today's insurance environment, where the NAIC reported the national combined average premium per issued vehicle reached $1,438 in 2023, up 14.42% from 2022. With higher repair costs and pressure across the market, older or specialized vehicles can cross total-loss thresholds more easily, so the valuation file needs to be stronger.

Build one claim packet, not a pile of papers

Organize the documents before sending them. I recommend one digital folder with labeled PDFs and photos, plus a short summary sheet explaining what each document proves.

Include:

- Condition support: Service history, inspections, detailing records, and recent photos.

- Value support: Option lists, build sheets, window sticker, and upgrade receipts.

- Ownership support: Title, registration, lienholder information, and payoff details.

- Recent investment support: Invoices for tires, brakes, suspension, restoration, or major repairs.

Messy records weaken good claims. Organized records move adjusters and appraisers.

6. Challenge Lowball Settlement Offers and Invoke the Appraisal Clause

The first offer is not sacred. In many cases, it's a starting number built from software, condition codes, and comparable vehicles you may never have chosen yourself.

When the offer comes in low, don't respond emotionally. Respond methodically. Ask for the complete valuation report, review every line, and identify what's wrong. Wrong trim. Missing options. Unrealistic condition deductions. Bad comparable vehicles. Mileage errors. Local market mismatch. Those are the issues that move settlements.

How to dispute the valuation the right way

Write a short dispute letter or email. Keep it tight and specific. State that you disagree with the actual cash value, list the errors, attach your support, and ask the insurer to revise the valuation.

Then look for the appraisal clause in your policy. That provision often allows either side to demand a formal appraisal process when there's a dispute over value. This is one of the few tools policyholders have that can move the decision out of the insurer's internal valuation track and into a contract-based procedure.

If you need a practical overview, review how an insurance appraisal clause works.

Don't argue that the offer is unfair. Show why it is unsupported.

When the appraisal clause becomes powerful

This mechanism is especially effective when the disagreement is about value, not coverage. If the carrier agrees the loss is covered but the number is wrong, the appraisal clause may be the cleanest route available.

What works:

- Pointing to specific errors: Bad comps and missing equipment matter more than general complaints.

- Backing every challenge with evidence: Listings, records, photos, and independent appraisal support.

- Invoking the contract language clearly: Ask for appraisal in writing and cite the policy provision.

What doesn't work:

- Threatening a lawsuit immediately: That often hardens positions before you've built a proper record.

- Sending unsupported online listings: Random ads without trim, condition, or equipment alignment won't carry much weight.

- Accepting quickly because you're stressed: Once you settle, reopening value is much harder.

In practice, this is the step where disciplined claimants separate themselves from rushed ones.

7. Understand Diminished Value Claims and Your Rights

Not every serious accident ends in a total loss. Sometimes the insurer repairs the vehicle and sends it back to you. That does not automatically mean you've been made whole.

A repaired vehicle can still be worth less because accident history follows it. Buyers, dealers, and appraisers all account for that. If you weren't at fault, you may have a separate diminished value issue to evaluate, depending on the law that applies and which insurer is paying.

Why this matters even in a total loss discussion

Drivers who are told, “Good news, it's repairable,” often assume the financial problem is over. Sometimes it isn't. The repair may address physical damage while leaving a market-value loss behind.

This comes up most often with newer vehicles, luxury vehicles, and cars with clean history before the crash. It also matters when structural repairs, major panel replacement, airbag deployment, or repainting become part of the repair history.

A vehicle can be fixed correctly and still be worth less on the open market.

If the insurer backs away from a total loss decision and switches to repair, don't just compare repair quality. Compare pre-accident market position to post-repair market position.

What to do if the car is repaired instead

Take these steps quickly:

- Ask which carrier is responsible: Diminished value claims are often pursued against the at-fault party's insurer.

- Get a post-repair value opinion: An independent appraiser can assess market stigma after the repairs.

- Save the repair file: Estimate, supplements, invoices, parts records, and photos all matter.

- Watch the timeline: Rights and procedures vary, so don't let the file sit.

This is a separate issue from a total loss valuation, but drivers need to know it exists. If the vehicle survives, value may still have been lost.

8. Decide on Settlement and Plan for Vehicle Replacement

Once the number is finally right, don't treat the final paperwork like a formality. Read it carefully and make sure you understand exactly what you're giving up.

Confirm the settlement amount, deductible treatment, lien payoff handling, title transfer instructions, and whether you're surrendering the vehicle or retaining salvage if that option is available. If there's a lender involved, find out where the payment is going and whether you'll receive any balance directly.

Think past the check

Actual cash value and replacement cost are not the same thing. That gap catches people off guard. A settlement may reflect the market value of the lost vehicle, while the next vehicle you need to buy may cost more once taxes, fees, transportation needs, and financing reality enter the picture.

If you still owe money on the totaled vehicle, contact the lender early. The settlement may go to the lienholder first. If the payoff exceeds the insurance settlement, gap coverage becomes a practical question immediately.

GEICO notes that once a vehicle is deemed a total loss, the insurer usually calculates actual cash value just before the incident and then subtracts any deductible in the settlement process, as described in its totaled-car overview noted earlier. That's why you need to know the net amount before you release the vehicle.

Make the closing steps work for you

Before signing off, handle these details:

- Remove your property: Check glove box, console, trunk, cargo bins, toll devices, and garage openers.

- Verify the release language: Make sure you understand whether you're settling property damage only or more.

- Plan transportation: Rental time can end quickly, so line up the replacement path early.

- Get final terms in writing: Never rely on a verbal summary of the settlement.

The goal at this stage is simple. Don't win the valuation fight and then lose money in the handoff.

8-Point Comparison: When Your Car Is Totaled

| Item | 🔄 Implementation Complexity | ⚡ Resources & Time | ⭐ Expected Outcome (Effectiveness) | 💡 Ideal Use Cases |

|---|---|---|---|---|

| Document the Accident Scene and Vehicle Damage Immediately | Low, quick, time‑sensitive actions; may be hard if injured | Minimal, smartphone/camera, cloud backup; minutes to an hour | High, strong visual evidence to support total‑loss or damage disputes | Any accident, especially when disputing damage severity or protecting collectible value |

| Understand Your Insurance Policy and Total Loss Definition | Moderate, careful review; may need expert interpretation | Low–Moderate, policy docs, time; possible agent or legal consultation | Medium‑High, clarifies rights and prevents premature or unfair totals | Before negotiating settlement or if policy/state definitions are unclear |

| Obtain an Independent Professional Appraisal | Moderate, schedules, inspection, appraiser selection | Moderate, $300–$1,000+, time for inspection and report | High, often yields higher, market‑based valuations and strong dispute support | High‑value, collector, customized vehicles or when insurer estimate is disputed |

| File a Claim and Notify Your Insurer Promptly | Low, procedural but must be accurate and timely | Minimal, phone/email, documentation; immediate action within 24–48 hrs | Medium, activates coverage and creates official timeline; may prompt low initial offers | All accidents as the first formal step in the claims process |

| Gather Complete Vehicle History and Documentation | Moderate, time‑consuming collection and organization | Low–Moderate, service records, receipts, scans; possible retrieval requests | High, substantiates pre‑accident condition and can raise settlement value | Luxury, well‑maintained, or modified vehicles and any dispute over condition |

| Challenge Lowball Offers & Invoke the Appraisal Clause | High, formal dispute, coordination, possible arbitration | Moderate–High, appraisal costs, potential legal fees, longer timeline (30–60 days) | High, can produce binding, higher settlements that insurers must honor | When insurer offers are significantly below market (e.g., >10–15% difference) |

| Understand Diminished Value Claims and Your Rights | Moderate, state‑specific law and valuation methods | Moderate, independent diminished‑value appraisal, documentation, possible claim against third party | Medium, additional compensation possible where law permits | Repaired vehicles with residual market loss; important in OR/WA and similar jurisdictions |

| Decide on Settlement and Plan for Vehicle Replacement | Moderate, negotiation of salvage, towing, and replacement logistics | Low–Moderate, time to research replacement, potential salvage negotiations | Medium‑High, finalizes recovery and replacement strategy; may reveal shortfalls | Final claim stage when settlement adequacy and replacement planning are required |

Take Control of Your Total Loss Settlement

The tow truck leaves, the insurer calls quickly, and a value number shows up before you have seen the worksheet behind it. That is the point where many drivers lose money. A total loss claim can look settled long before it has been properly examined.

The drivers who do best in these claims treat valuation like a file, not a conversation. They ask for the insurer's valuation report. They compare the listed trim, mileage, options, condition ratings, and comparable vehicles against the actual car. They pull together service records, receipts, photos, and any proof that the vehicle was worth more than a generic book figure. That work matters because total loss disputes are usually won on documentation and procedure, not on how strongly someone objects to the offer.

The appraisal clause deserves special attention. Many policyholders do not know it exists until the adjuster has already framed the insurer's number as final. In a value dispute, that clause can force a formal process with independent appraisers instead of repeated requests for the carrier to review its own work. It does not solve every claim, and it does not apply to every disagreement, but it is often the clearest contractual tool available when the fight is about what the car was worth on the date of loss.

Good claim handling is specific. Review the valuation worksheet line by line. Correct factual errors in writing. Ask why certain comparable vehicles were used and why others were excluded. If the vehicle had unusual value because of condition, documented upgrades, rare options, or a strong local market, an independent appraisal can put credible support into the file that the insurer has to address.

That is often the difference between a routine low offer and a settlement that reflects the market.

Drivers also need to make a practical decision about time and cost. An independent appraisal and appraisal-clause dispute can add expense and extend the claim, but that trade-off can make sense when the insurer's number is materially below supportable market value. I have seen this matter most with luxury vehicles, collector cars, trucks with documented equipment packages, and older vehicles in unusually clean condition. Those are the claims where insurer databases and generic condition adjustments often miss the mark.

Keep the claim focused on evidence, policy language, and procedure. Ask for the documents. Preserve your records. Put objections in writing. If the insurer will not correct a flawed value analysis, use the formal tools built into the policy to challenge it. That is how you protect your position and get to a number you can use.