Let's be honest—when you've been in a car accident, the last thing you want to deal with is more financial stress. You get the car fixed, it looks great, and you think you're whole again. But there's a hidden cost that most people don't discover until it's too late: diminished value.

In simple terms, the diminished value of a car after an accident is the immediate, and often significant, drop in its resale price, even after it's been perfectly repaired. Why? Because a vehicle with an accident on its record is simply worth less to the next buyer.

What Diminished Value Really Means for Your Car

Put yourself in a car buyer's shoes for a moment. You're looking at two identical used sedans on a lot—same year, same mileage, same features. One has a squeaky-clean vehicle history report. The other was in a collision a year ago but was professionally repaired and looks brand new.

Which one are you going to pay top dollar for? The answer is obvious. You’d probably offer less for the one that’s been in a wreck, or you might just walk away. That gap in value, that gut feeling that makes you hesitate, that is diminished value in a nutshell. It's the real, tangible financial loss your car suffers the second an accident is logged in its history.

The Stigma of an Accident Report

No matter how masterful the repairs are, an accident leaves a permanent mark on a car's record. Reports from services like CARFAX and AutoCheck will show that history to any potential buyer, creating what's known in the industry as "inherent diminished value."

This isn't about shoddy repair work. It’s all about perception. Buyers get nervous about potential hidden frame damage or future mechanical gremlins, so they naturally devalue the car. This isn't just a theory; it's a market reality that can cost you thousands when you go to sell or trade in your vehicle.

The key takeaway is this: Your car was damaged, and now, through no fault of your own, its history makes it less desirable. You have a right to be compensated for that specific financial loss.

For a clearer picture, let's break down the core ideas with a quick overview.

Quick Overview of Diminished Value Concepts

| Concept | Simple Explanation |

|---|---|

| Diminished Value | The loss in a car's market value after an accident, even with perfect repairs. |

| Inherent Diminished Value | The automatic loss in value due to the accident history itself. It's about stigma. |

| Repair-Related DV | Additional value loss from subpar repairs (e.g., mismatched paint, poor part alignment). |

| Claim Process | Filing a claim against the at-fault driver's insurance to recover this lost value. |

Understanding these distinctions is the first step toward getting the compensation you deserve.

Who Foots the Bill for This Loss?

So, who is on the hook for this loss? In nearly all situations, if the other driver was at fault for the accident, their insurance company is responsible for paying your diminished value claim.

This is considered a third-party claim. It’s filed to cover the full scope of your property damage, which includes not just the repair bill but also the proven loss in your car's market value.

This guide will walk you through everything you need to know about navigating the diminished value of a car after an accident. We'll cover:

- The different types of diminished value you can claim

- How to properly calculate what you're owed

- The step-by-step process for filing a claim that gets results

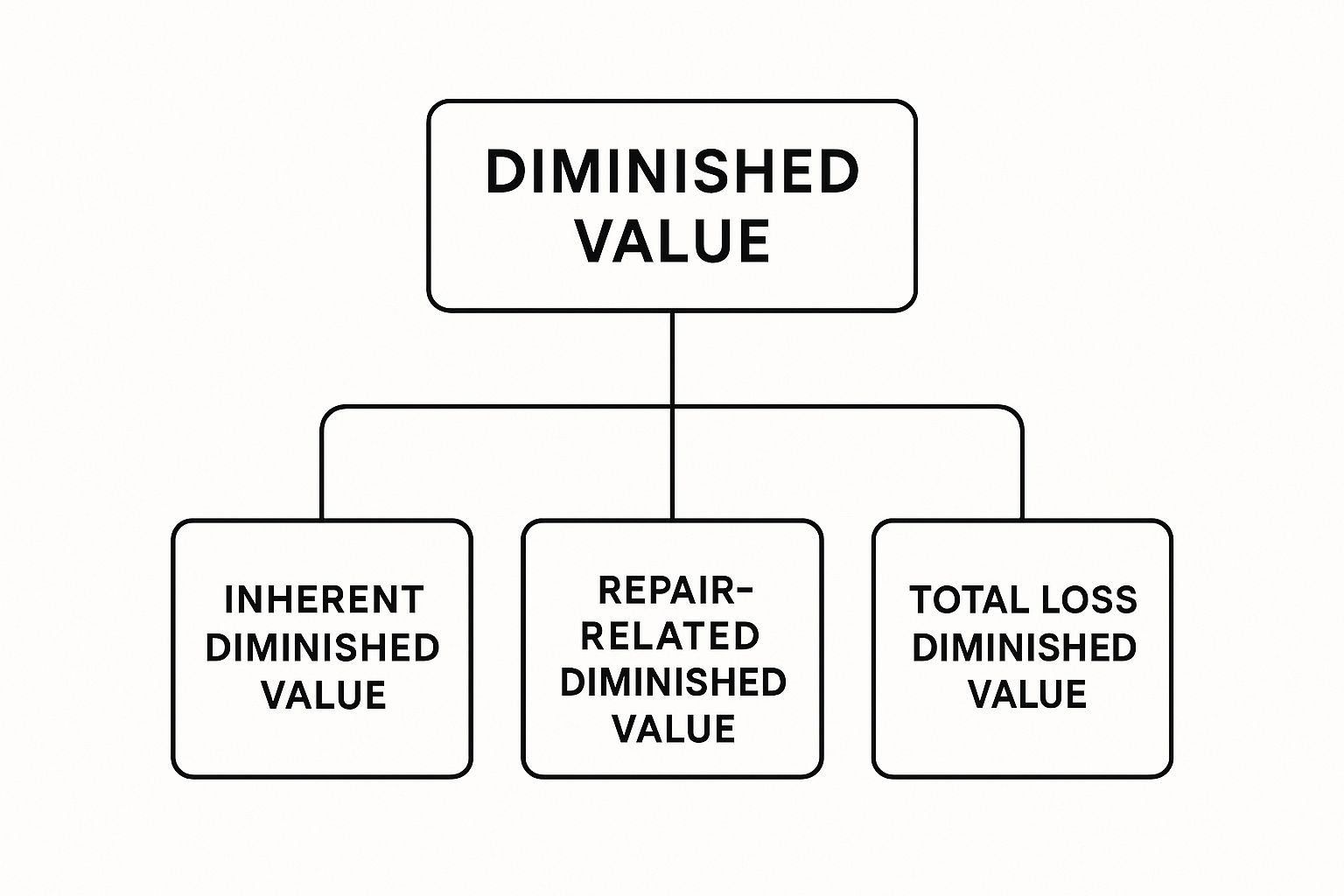

The Three Types of Diminished Value Claims

When your car gets into an accident, the loss in value isn't a single, simple number. It's actually a bit more nuanced. Think of diminished value as having three distinct flavors, and figuring out which one applies to your situation is the key to filing a successful claim.

The infographic below breaks it down nicely, showing how each type fits into the bigger picture.

As you can see, they all branch out from the accident itself. While all three are technically real, you’ll find that one of them is the basis for the vast majority of insurance claims. Let's break them down.

Inherent Diminished Value

This is the big one—the most common and universally recognized type of claim. Inherent Diminished Value is the automatic drop in your car’s resale value just because it now has an accident on its record.

It has absolutely nothing to do with how well the car was fixed.

You could have the best body shop in the state, using top-of-the-line equipment, restore your car to a condition that’s visually and mechanically perfect. It doesn't matter. The moment that accident was logged on a vehicle history report like CARFAX or AutoCheck, a permanent stigma was attached to it. Future buyers will always choose the car without the accident history if all else is equal, and that perception forces its market price down. That loss is what you’re owed.

A vehicle’s history is part of its identity in the marketplace. Once that history includes a collision, its perceived risk increases, and its value decreases—permanently. This is the core principle behind inherent diminished value.

Let's say your two-year-old SUV was worth $35,000 before someone ran a red light and hit you. After flawless repairs, you decide to trade it in. The dealer pulls the history report, sees the collision, and offers you $31,000. That $4,000 gap is the inherent diminished value, created solely by the accident record.

Repair-Related Diminished Value

Now, let's flip the coin. While inherent diminished value assumes a top-notch repair job, Repair-Related Diminished Value covers the opposite. This is the additional loss in value caused by shoddy or incomplete repair work.

This kind of value loss shows up in obvious (and not-so-obvious) ways:

- Mismatched Paint: The new panel is a slightly different shade that you can see in the sunlight.

- Use of Aftermarket Parts: The shop used cheaper, non-OEM (Original Equipment Manufacturer) parts instead of factory-grade ones.

- Poor Panel Alignment: You can fit your finger in the gap around the new door, but the other side is tight.

- Unresolved Mechanical Issues: The car just doesn't drive right anymore. It might pull to one side or make a new, unsettling noise.

This loss is a direct result of the body shop's poor workmanship. Proving it means getting a post-repair inspection from an independent, trusted mechanic who can document exactly what’s wrong and how it impacts the car’s safety and value.

Immediate Diminished Value

The third type, Immediate Diminished Value, is more of a temporary, technical state. It’s the difference between your car’s pre-accident value and its value as a crumpled wreck right after the collision, before a single tool has touched it.

Because nearly every claim is settled after the car is fixed, this type of diminished value rarely comes into play. Once the repairs begin, the conversation naturally shifts to either inherent or repair-related value, which reflect the car's final, post-accident condition.

Key Factors That Influence Your Claim Amount

So, what determines if your diminished value claim is worth a few hundred dollars or tens of thousands? It’s not a random number. The final amount hinges on a specific set of variables that appraisers and insurance companies look at to gauge the hit to your car's resale value.

Think of it this way: a minor door ding on a 10-year-old daily driver with 150,000 miles on the clock barely moves the needle. But what about frame damage on a brand-new luxury SUV? That’s a huge red flag for any potential buyer, and the vehicle's market value will nosedive as a result.

It all boils down to two main things: the car's pre-accident prestige and the severity of the damage it sustained.

Vehicle Age, Mileage, and Condition

The car's story before the accident is chapter one. A newer vehicle in pristine condition with low mileage simply has more value to lose. That’s why these vehicles see the biggest drops.

For instance, a one-year-old car with just 5,000 miles will take a much bigger financial hit than a decade-old vehicle with 150,000 miles. Why the big difference? Buyers looking for a nearly new car demand perfection. An accident history, even with flawless repairs, is often a deal-breaker and forces the seller to slash the price. On an older car, a minor accident history is just another part of its long life and is often already factored into its much lower price.

Severity and Type of Damage

This is the big one. The nature of the damage is probably the single most important factor in any diminished value calculation. Not all dents are created equal.

- Cosmetic Damage: We're talking about scratches, small dings, or scuffed bumpers. If the damage didn't touch the frame or any safety systems, the diminished value will be on the lower end.

- Structural Damage: This is where the numbers get serious. Any repair to the vehicle's frame, unibody, or core support structures will cause a major loss in value. Buyers worry—and for good reason—about the car's long-term safety and integrity.

- Airbag Deployment: If the airbags went off, the accident is automatically classified as severe on vehicle history reports. This alone signals a major impact and leads to a much higher diminished value assessment.

As a rule of thumb, if the collision was bad enough to require frame straightening or welding, you can expect the diminished value of a car after an accident to be substantial. No buyer wants to gamble on a car whose core safety structure has been compromised and pieced back together.

The quality of the repair work also plays a huge role. A mismatched paint job, shoddy bodywork, or the use of cheap aftermarket parts can make the value loss even worse. This is precisely why getting independent auto insurance appraisals is so critical. A professional appraiser can document not just the inherent loss from the accident itself, but also any additional loss caused by subpar repairs.

On average, a car loses between 10% and 25% of its pre-accident value after a wreck. For a luxury sedan, that could easily be a 15-20% drop, while an SUV might see a 10-15% reduction, even after being fixed by a top-tier shop.

Impact of Key Factors on Diminished Value

To see how these factors interact, let's look at some side-by-side scenarios. The table below shows how different circumstances can push your diminished value claim higher or lower.

| Factor | High Impact Scenario (Increases DV) | Low Impact Scenario (Decreases DV) |

|---|---|---|

| Vehicle Type | Luxury brand, sports car, or new model | Common, older model, economy car |

| Vehicle Age | Less than 2 years old | 7+ years old |

| Mileage | Under 20,000 miles | Over 100,000 miles |

| Damage Type | Structural or frame damage, airbag deployment | Minor cosmetic damage (dents, scratches) |

| Repair Quality | Use of aftermarket parts, poor paint match | OEM parts used, undetectable repairs |

| Accident History | First accident reported on a clean history | Vehicle has a prior accident history |

As you can see, the "perfect storm" for a high diminished value claim is a new, low-mileage luxury vehicle with significant structural damage. Conversely, an older, high-mileage car with a few scratches will result in a much smaller claim.

How to Figure Out Your Car's Loss in Value

Putting an exact dollar amount on your car’s diminished value after an accident can feel a bit like guesswork. It’s not. While there's no single, universally accepted formula, several solid methods can help you build a powerful, fact-based case for your claim. The goal is to get past speculation and into documented proof of your financial hit.

The Infamous "Rule 17c" Formula

One of the first things you might hear about from an insurance adjuster is a formula often called "Rule 17c." This is an internal calculation some insurance companies use as a starting point. It takes a percentage of your car’s pre-accident value and then chips away at it with "modifiers" for damage severity and mileage.

Frankly, this formula has major problems. It was created for a specific court case and almost always spits out a lowball number that serves the insurer’s interests, not yours. It’s good to know what it is, but you should never accept a 17c-based offer as the final word.

For a much more realistic starting point, a good diminished value claim calculator can give you a better sense of what your vehicle might actually be worth.

Better Ways to Prove Your Claim

To build a case that an adjuster can't easily dismiss, you need to bring real-world proof to the table—evidence that shows what’s actually happening in your local car market.

Here are the most effective ways to establish your car's true loss in value.

1. Get Quotes from Car Dealerships

This is a simple but incredibly powerful strategy to show what your car is worth now. It’s all about creating a clear "before and after" picture.

- Step One: Ask a sales manager at a dealership—ideally one that sells your car’s make—for a written trade-in estimate for a vehicle just like yours, but with a clean history. Make sure they note the same year, model, mileage, and condition.

- Step Two: Now, show them your actual repaired car. Provide the full accident history and all the repair records, and ask for a formal written trade-in offer.

- Step Three: The difference between those two numbers is your diminished value, plain and simple. Getting this in writing from two or three different dealerships gives you undeniable proof.

The beauty of this approach is its irrefutable logic. You're showing the insurance company exactly what a professional in the business would pay for your car now, versus what they would have paid before the wreck. It’s hard to argue with that.

2. Hire a Certified Independent Appraiser

When it comes to winning a serious diminished value claim, this is your ace in the hole. An independent, certified appraiser is an expert who works for you, not the insurance company. They have no skin in the game other than providing an accurate, unbiased assessment.

The appraiser will perform a hands-on inspection of your car, scrutinize the repair work and documentation, and research your specific local market to see how the accident history affects its resale value.

What you get back is a comprehensive, detailed report that presents an expert opinion on your car's precise loss in value. This report elevates your claim from a simple request to a professional, evidence-backed demand. It provides the leverage you need to negotiate effectively and is truly the gold standard for proving your case.

Your Step-by-Step Guide to Filing a Claim

Knowing your car has lost value is one thing; getting that money back is a whole different ball game. To successfully claim the diminished value of a car after an accident, you need a smart plan and rock-solid proof. This guide will walk you through the process, step by step, so you can hold the at-fault driver's insurance company accountable.

The entire process hinges on one simple fact: who was at fault. Diminished value is almost always a third-party claim. That just means you’re filing against the insurance company of the person who hit you, because their client’s mistake is what cost you money.

Step 1: Get Your Paperwork in Order

Before you even think about picking up the phone, you need to build your case. Think of it like a legal file—the more organized and compelling your evidence, the better. Insurance adjusters see claims all day long, and a professionally prepared file immediately signals that you mean business.

Your evidence folder should have these key items:

- The Official Police Report: This is ground zero. It establishes the basic facts of the crash and, most importantly, who was ticketed for causing it.

- Repair Invoices and Photos: Get the detailed, itemized bill from the body shop. Before-and-after pictures are also incredibly powerful, as they visually show the severity of the damage.

- Proof of Pre-Accident Value: Use trusted sources like Kelley Blue Book or NADAguides to print out a report showing what your car was worth right before the accident.

- Your Independent Appraisal Report: This is the cornerstone of your entire claim. A report from a certified, independent appraiser gives you an expert, unbiased calculation of exactly how much value your car lost.

Step 2: Write and Send a Demand Letter

With your evidence locked and loaded, it’s time to formally tell the at-fault driver's insurance company that you're coming for your diminished value. This is done with a professional demand letter.

Keep the letter clear, firm, and to the point. State your car's pre-accident value, reference the accident details, and clearly state the diminished value figure from your appraisal. Make sure to attach copies of all your supporting documents (especially that appraisal report!) to back up every word you say.

For a more detailed look at crafting this letter, you can check out our comprehensive guide on how to file a diminished value claim.

Step 3: Negotiate with the Insurance Adjuster

After the insurance company gets your letter, they'll assign an adjuster to your case. You have to remember what their job is: to protect their company's bottom line by paying out as little as possible. The first offer you get will almost certainly be a lowball.

Don't take it.

An insurance adjuster's first offer is rarely their best offer. It is the beginning of a negotiation, not the end. Be prepared to stand firm, use your appraisal report as leverage, and professionally argue your case.

Politely but firmly reject their initial offer and point them back to your evidence. Explain that your claim isn't just a number you pulled out of thin air—it's based on a professional appraisal reflecting a real-world market loss.

Be persistent, but always stay courteous. Keep a log of every phone call, noting the date, time, and the adjuster's name. Better yet, try to communicate over email so you have a written record of the entire conversation. If the adjuster still won't budge and offer a fair settlement, you may need to take things to the next level.

Common Mistakes That Can Ruin Your Claim

Navigating a diminished value claim is tricky, and even small missteps can end up costing you thousands. If you want to get the full compensation you're owed for the diminished value of a car after an accident, you have to play your cards right from the very beginning.

One of the most devastating mistakes you can make is cashing the final repair check from the insurance company too soon. Look closely at that check—many have fine print on the back stating that by cashing it, you agree to settle all claims from the accident. Depositing it could legally slam the door shut on your diminished value case. Always read every single word before you sign or cash anything.

Another common pitfall is just taking the insurance company’s appraiser at their word. Remember, their loyalty is to their employer, and their main goal is to minimize the company's payout, not to make you whole.

Protecting Your Claim From Costly Errors

To sidestep these blunders, you have to be your own best advocate. Failing to get everything down in writing, for example, can seriously weaken your position. Whenever you can, communicate with adjusters through email to create a clear paper trail of your entire conversation.

Here are a few more critical mistakes to steer clear of:

- Missing the Deadline: Every state sets a time limit, known as the statute of limitations, for filing property damage claims. This is often just two or three years from the date of the accident. If you miss that window, your right to file a claim is gone for good.

- Accepting Verbal Promises: If an adjuster tells you something over the phone, it means very little. A verbal agreement is almost impossible to enforce later on, so always ask them to confirm it in writing.

- Not Hiring an Expert: A professional, independent appraisal is the most powerful tool in your arsenal. Without it, your claim is basically just your word against the insurance company's, and that’s a tough battle to win.

Common Questions About Diminished Value

Even when you understand the basics, the world of diminished value can feel a little fuzzy. Let's clear things up by tackling some of the most common questions drivers have after an accident.

Can I Claim Diminished Value from My Own Insurance Company?

This is a big one, and the answer is almost always no. Think of it this way: your insurance policy is a contract to repair your car back to its pre-accident condition, not to compensate you for its lost resale value.

A diminished value claim is what's known as a third-party claim. You file it against the insurance company of the driver who caused the accident. Since their client’s mistake led to your car’s drop in value, their policy is the one responsible for making you financially whole again.

There are a few rare exceptions. For instance, Georgia law sometimes allows for first-party claims, but that's not the norm. For most people, the at-fault driver's insurer is your target.

Do I Need to Hire a Lawyer?

It really depends on the situation. If your vehicle is a high-end luxury car, a classic, or brand new, the diminished value can be significant. In those cases, bringing in an attorney can be a very smart move to protect a substantial financial interest.

An attorney becomes especially important if the insurance company is playing hardball—denying a perfectly valid claim, making a ridiculously low offer, or just ignoring you. Having a lawyer in your corner shows them you mean business.

But what if the claim is smaller? Legal fees could easily eat up whatever you might recover. For many people, the best and most cost-effective first step is to hire a certified independent appraiser to build your case.

How Long Do I Have to File a Claim?

There’s a deadline for filing, and it's called the statute of limitations. Because diminished value falls under property damage, the time limit is set by state law and can be anywhere from two to five years from the date of the accident.

This is not a soft deadline—it's a hard stop. If you miss that window, your right to claim compensation for your car's lost value is gone forever. Don't wait.

Don't let an insurance company dictate what your vehicle is worth. At Total Loss Northwest, our certified appraisers provide the expert, unbiased reports you need to fight for a fair settlement on your diminished value or total loss claim. Get the professional appraisal you deserve.