A lot of classic car owners learn the same lesson at the worst possible moment. The car gets hit, stolen, or declared a total loss, and the insurance company values it like an old used vehicle instead of a documented collector asset. The offer arrives. It looks official. It also ignores the restoration work, the originality, the parts hunt, the receipts, and the market reality that makes your car worth more than a generic valuation tool can recognize.

That gap is where classic car appraisal certification matters.

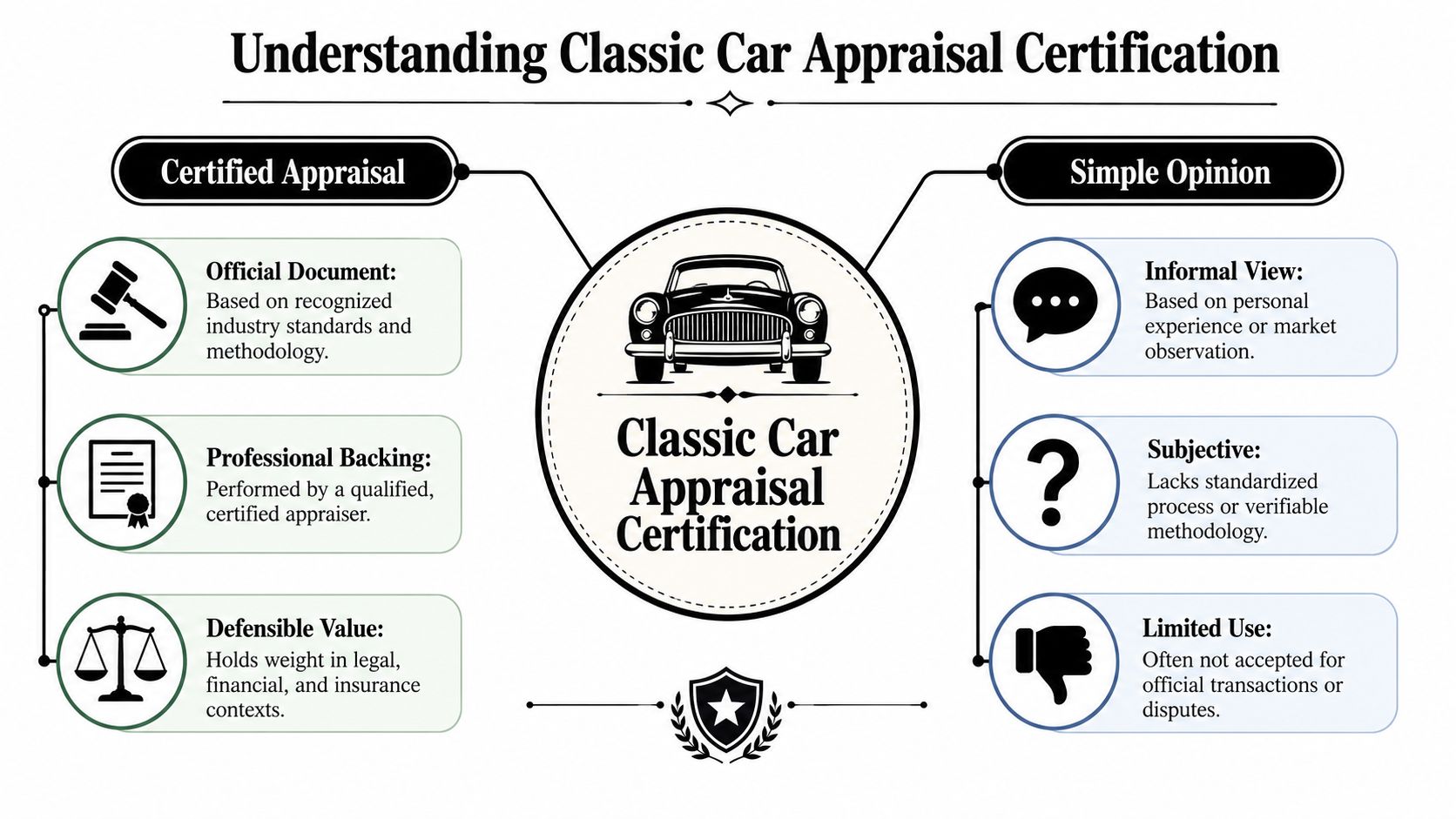

A certified appraisal isn't just paperwork for a file folder. In a dispute, it becomes evidence. It gives your value position structure, support, and a methodology that an adjuster, underwriter, attorney, or court can follow. If you own a classic car, that matters long before a claim ever happens. It matters when you buy coverage, when you set an agreed value, when you settle an estate, and when you need to prove that your vehicle is not interchangeable with every other example of the same year and model.

Your Classic Car Is More Than Just Metal

A common scenario goes like this. A well-kept classic is damaged in an accident caused by someone else. The owner expects the claim to be straightforward because liability is clear. Then the insurer values the car using ordinary market logic that fits commuter vehicles, not collector cars.

That's where owners get blindsided.

A classic car can look familiar on paper and still be completely different in value once you account for originality, restoration quality, documentation, rarity, and historical significance. A generic online estimate or a quick opinion from a local shop won't carry enough weight when an insurer pushes back. If you want to understand the moving parts behind collector values, this guide on how to value a classic car is a useful starting point.

What goes wrong with ordinary value opinions

Most low offers have the same weakness. They flatten the car into a model-year entry and ignore the details that collectors pay for.

That approach fails owners in a few predictable ways:

- Originality gets ignored: Numbers-matching components, correct finishes, and factory-correct details often make a major difference to buyers, but generic systems don't inspect for them.

- Restoration work gets treated casually: A car with documented restoration receipts and careful workmanship isn't the same as one with cosmetic freshening.

- Documentation gets discounted: Titles, maintenance records, restoration photos, and period paperwork help support value, but they only matter if someone is trained to evaluate them.

- Collector market behavior gets missed: Standard used-car logic relies on depreciation patterns. Classic cars don't always follow that pattern.

Practical rule: If the value can be explained in one sentence, it usually isn't strong enough for a contested claim.

The report that changes the conversation

A certified appraisal changes the discussion because it gives you a report built for scrutiny. It turns “my car is worth more than that” into a supported position.

Owners often think the battle is about convincing the insurer emotionally. It isn't. The battle is about presenting a valuation in a form the insurer has to address. Certification matters because it signals that the appraiser used a recognized process, documented the vehicle in detail, and prepared a report that can stand up in negotiation.

That's why I tell owners to stop thinking of certification as a bureaucratic hurdle. It's a defensive tool. It protects the investment you already made in the car.

What Classic Car Appraisal Certification Really Means

Certification separates a defensible appraisal from an unsupported opinion. Anyone can say a classic “should be worth” a certain amount. A certified appraiser has to show how that conclusion was reached and why the support behind it is credible.

Certified appraisal versus casual opinion

Think of it this way. A casual opinion is like a knowledgeable conversation at a car show. A certified appraisal is closer to a forensic report. It has to identify the subject vehicle, inspect it, review the records, analyze comparable market activity, and explain the reasoning behind the final value.

According to Auto Praise's explanation of accurate classic car appraisals, certified appraisers use data points from Hagerty Valuation, proprietary auction results, private sales data, and dealer sales data. That same source also states that certification requires a detailed physical inspection, documentation of modifications or restoration work, and a thorough market comparison so the final value reflects the actual market rather than a generic depreciation model.

What a certified appraiser actually does

A proper assignment usually includes more than owners expect. It isn't just a walk-around and a guess.

A serious report is built on several layers:

| Element | Why it matters |

|---|---|

| Physical inspection | Confirms actual condition, not assumed condition |

| Documentation review | Supports restoration claims, ownership history, and maintenance |

| Market comparison | Connects the vehicle to real-world collector transactions |

| Modification analysis | Distinguishes value-enhancing work from value-reducing changes |

| Written report | Creates a record that can be used in insurance, legal, or financial settings |

What certification is really buying you

Certification buys methodology. That's the overlooked part.

Owners sometimes focus only on the final number. The number matters, but the process matters more when someone challenges that number. If your appraisal is going into an insurance negotiation, estate file, or donation record, the value has to be supported in a way that another professional can follow.

A certified appraisal works because it gives the other side something harder to dismiss than opinion.

That's why a short letter with a rough value rarely helps in a difficult claim. It may tell you what someone thinks. It does not always tell an insurer why they should pay attention.

The Authorities Behind the Certification

A certified appraisal carries weight only if the credential traces back to recognized standards. In classic car work, that standard is USPAP, the Uniform Standards of Professional Appraisal Practice.

Why USPAP matters

USPAP sets the rules for ethical conduct, scope of work, recordkeeping, and how an appraiser supports a conclusion. The Appraisal Foundation's overview of USPAP explains that these standards are established by the Appraisal Standards Board and are used to guide credible appraisal practice.

For an owner, that matters in one place above all. A disputed claim.

Insurance companies rarely react to passion, restoration receipts alone, or a seller's opinion of value. They respond to a report built on recognized standards, clear methodology, and support they can audit. In practice, a certified appraisal becomes the language the insurance company cannot ignore.

The organizations owners should recognize

Reputable certification often comes from established organizations such as:

- American Society of Certified Auto Appraisers

- Bureau of Certified Auto Appraisers

- Professional Automobile Appraisers Association of America

- Other specialty appraisal groups that require formal training, standards compliance, and ethics rules

The point is not brand recognition by itself. The point is whether the organization requires structured training, enforces professional standards, and expects the appraiser to produce work that can stand up in an insurance file, legal review, or tax matter.

A self-issued title does not protect your value

Collector car experience has value. So does time in the hobby. Neither replaces a recognized appraisal framework.

If I review an appraisal after a loss, I look for three things right away:

- Standards. Does the appraiser work under recognized rules such as USPAP?

- Method. Can the report show how the value was developed?

- Defensibility. Would the report hold up if an adjuster, attorney, or opposing expert challenged it?

That is the practical difference between a credential that helps and a title that only sounds impressive. If a report cannot survive scrutiny, it gives the insurer room to cut value, question condition, or substitute a weaker number. A certified appraisal closes off much of that opening before the argument starts.

The Rigorous Path to Becoming a Certified Appraiser

A claim gets contentious fast when the insurer questions condition, rarity, or restoration quality. At that point, the owner needs more than enthusiasm and more than a number pulled from a price guide. The report has to be built by someone who has been trained to inspect, analyze, document, and defend a value in terms the insurance company will accept.

That is why the path to certification matters.

According to Auto Appraisal Network's overview of becoming a professional auto appraiser, candidates commonly start with basic educational prerequisites, then complete specialized coursework through recognized appraisal organizations. The same source notes that appraisers are expected to complete continuing education each year so their methods stay current with changing market conditions and valuation standards.

Training covers far more than car knowledge

A long history around collector cars helps, but it does not teach someone how to produce a report that survives an adjuster's review. Certified appraisers are trained to inspect a vehicle methodically, separate original components from replacement parts, assess restoration quality, review supporting records, and connect those findings to comparable market data.

They also learn how to write the report itself.

That part gets overlooked by owners until a dispute starts. An insurer may not care that an appraiser has owned old cars for decades. It will care whether the report clearly explains condition, documents the inspection, identifies the valuation approach used, and shows how the final number was reached.

Some certification tracks are structured and demanding

Formal programs are not casual weekend seminars. According to the National Auto Appraisal Association certification course page, candidates complete online instruction, practical training, supplementary assignments, and a required passing score before earning initial certification.

Other certification bodies require extended hands-on inspection work, standards instruction, ethics training, and a technical written report. As noted earlier, serious programs expect candidates to do more than attend class. They must show that they can inspect a vehicle carefully and turn that inspection into a defensible appraisal.

In practice, that is the dividing line.

An owner hiring a certified appraiser is paying for trained judgment under a recognized process, not just familiarity with old cars.

Why owners should care about the training path

Training shows up in the details that affect value and in the way those details are documented. A properly trained appraiser knows where owners and insurers usually clash. Originality versus replacement. Older restoration versus fresh cosmetic work. Correct driveline versus period-looking substitute. High-end refinish versus average driver-quality paint. Those differences can move value substantially.

They also know what weakens a report before the insurer ever responds:

- A verbal estimate with no inspection record

- A short letter with no market support

- A guide-based number that ignores the actual car

- A value promised before documentation and condition are reviewed

A stronger appraisal usually includes:

- A structured, documented inspection

- Review of titles, invoices, photos, and history files

- Market analysis tied to comparable vehicles

- A written report prepared under recognized standards

That is what gives certification practical value for an owner. In a routine conversation, anyone can state an opinion. In a disputed claim, the actual playing field is documentation, method, and credibility. A certified appraisal speaks that language, and that is the language the insurance company cannot ignore.

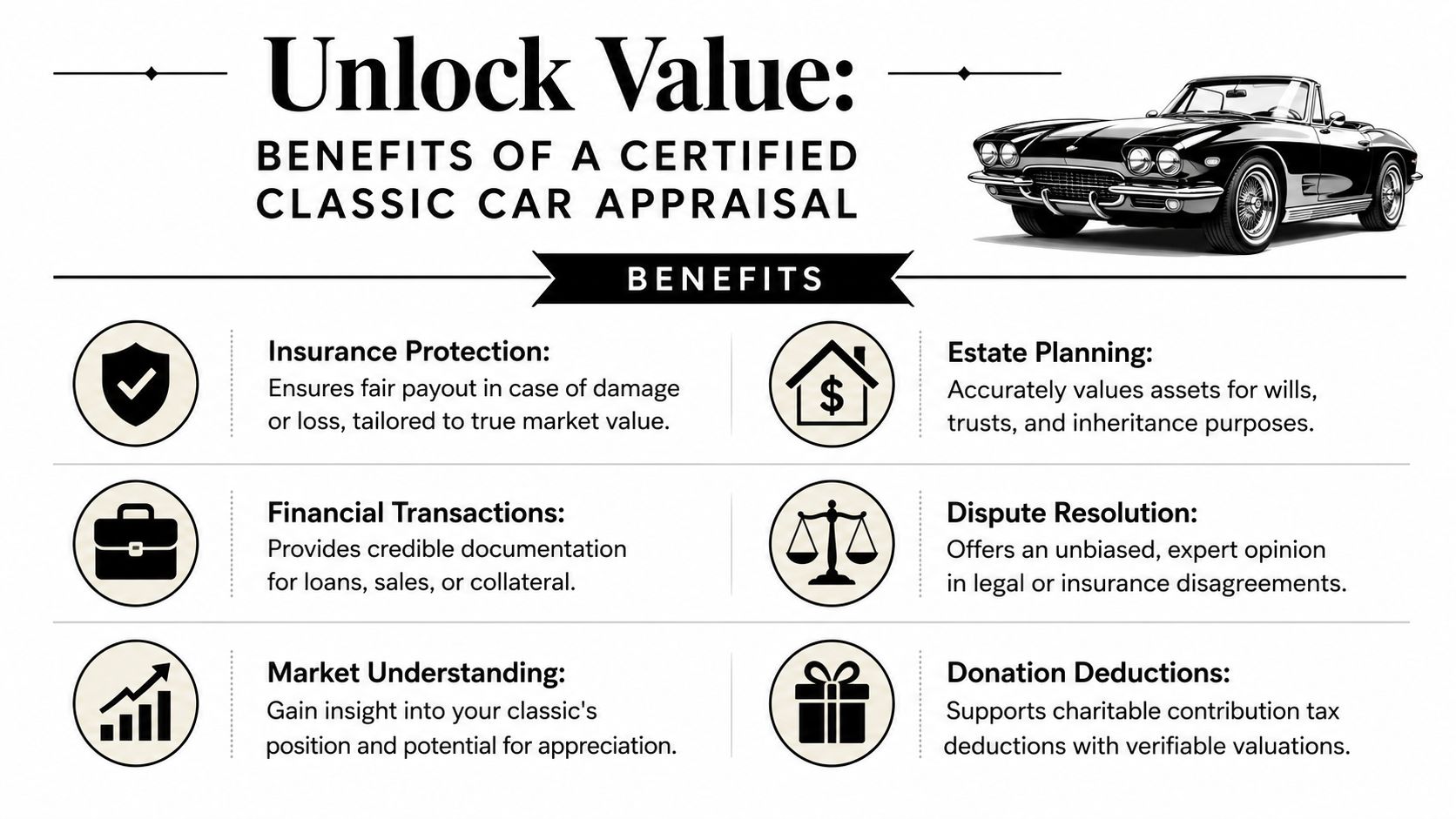

Key Benefits of a Certified Appraisal for Owners

Owners often ask whether a certified appraisal is worth paying for before a dispute exists. In practice, that's the best time to get one. It puts you in a stronger position before you need to argue.

Where a certified appraisal pays off

A certified appraisal helps in several situations that owners face repeatedly over the life of a collector vehicle.

- Agreed value insurance: This is the most immediate benefit. A certified report supports the value you want the insurer to accept before a loss occurs.

- Estate and probate work: Executors and families need a value that can be documented and defended.

- Private sale negotiations: A buyer may challenge your asking price. A certified report gives your price support.

- Donation and tax-related uses: A documented appraisal can support the file when a vehicle is donated.

- Dispute resolution: If an insurer or opposing party minimizes value, the appraisal provides an independent record.

Why insurers respond differently to certified reports

Insurance companies handle claims through systems, procedures, and documentation standards. If your response is emotional, they can ignore it. If your response is a detailed certified report, they have to address the substance.

That's why I often describe a certified appraisal as the language the insurance company can't ignore. It speaks in inspection findings, market support, documentation, and methodology.

One report, multiple jobs

Owners sometimes see an appraisal as a one-time transaction tied to a single event. That's too narrow. A well-prepared report can support ownership decisions for years, especially if the car has stable documentation and the file is updated when needed.

Here's a practical approach:

| Owner situation | What the certified appraisal does |

|---|---|

| Buying specialty insurance | Supports the insured value |

| Selling privately | Helps justify the asking price |

| Estate administration | Creates a supportable asset value |

| Insurance dispute | Provides independent evidence |

| Donation planning | Documents the vehicle for file support |

A good appraisal doesn't just tell you what the car is worth. It gives you something usable when another party questions that worth.

That's the difference between an expense and a protective tool.

How to Verify and Choose a Qualified Appraiser

Choosing the appraiser is where many owners either protect themselves or set themselves up for trouble. The right appraiser gives you a report that holds up under pressure. The wrong appraiser gives you a number with no real traction.

A good first move is to review firms that focus on this work and understand how classic auto appraisers approach collector vehicles in contested situations.

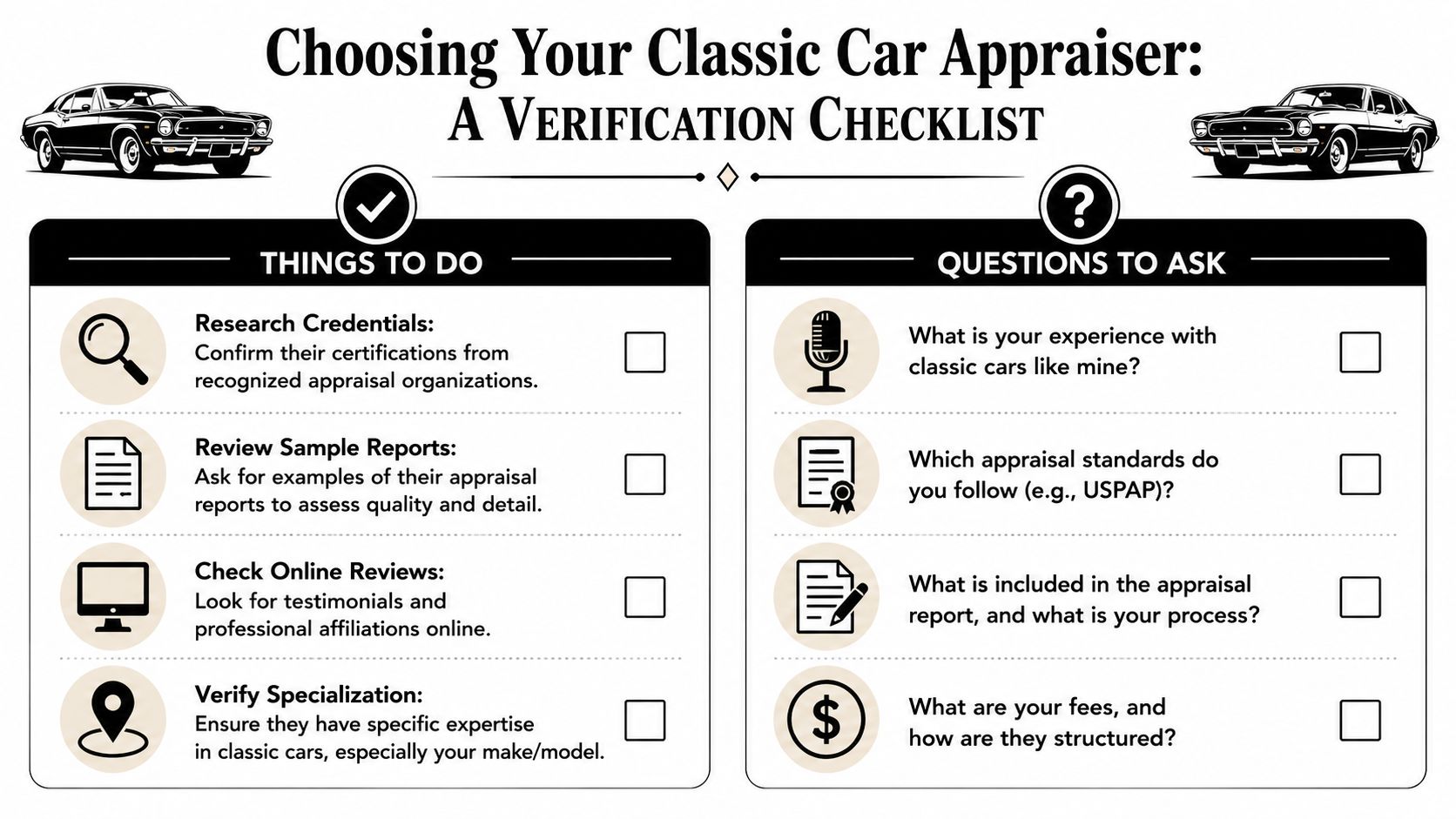

The vetting checklist that matters

Start with verification, not marketing.

- Confirm the certification directly: Ask which organization issued it and verify the credential if the issuing body offers that option.

- Request a sample report: You're looking for depth, structure, photographs, documentation review, and market support.

- Ask about your specific vehicle type: A person who knows general collector cars may not understand your marque, restoration standards, or buyer pool.

- Ask what standards they follow: USPAP should come up clearly if they work in formal valuation settings.

- Ask how their fee is structured: You want an independent professional, not someone whose compensation depends on hitting a target number.

The advanced question that separates pros from amateurs

Provenance is where weak appraisers often get exposed.

According to the Certified Auto Appraisers FAQ, a major gap in many certification systems is the lack of standardized guidance for valuing provenance, even though auction data shows that vehicles with verified history can bring 20 to 40 percent higher prices than comparable models without that history. That source also notes that asking an appraiser how they handle this issue is a key vetting step.

If your car has race history, celebrity ownership, museum display history, documented first ownership, or notable event participation, ask this plainly: How do you document and support the value impact of provenance in your report?

That question tells you a lot, fast.

Here's a helpful overview before you start calling around:

Red flags owners should take seriously

Some warning signs are easy to miss because they sound customer-friendly.

- They promise a value before inspection: That's not analysis. That's salesmanship.

- They produce very short reports: Thin reports usually give opposing parties more room to dismiss the conclusion.

- They work on contingency: Independence matters.

- They avoid process questions: A qualified appraiser should be able to explain what they inspect, what they review, and how they support the final number.

If an appraiser can't explain how they reach value, don't expect an insurance company to respect the report.

Putting Your Certified Appraisal to Work in a Claim

The appraisal matters most when there's money on the table and the other side wants to pay less. That's when the report moves from useful paperwork to strategic evidence.

In a total loss or diminished value dispute, a certified appraisal gives you an independent valuation supported by inspection findings, documentation, and market analysis. Instead of arguing from frustration, you're arguing from a developed record. If you want to understand the mechanics of that process in a claim setting, review the insurance appraisal process.

How the report changes the leverage

Insurance companies are used to dealing with unsupported objections. “My car was worth more than that” is common. It rarely changes the file by itself.

A certified report is different because it can force the discussion onto evidence. It gives your side a methodology, not just a conclusion. In many disputes, that alone improves the quality of the negotiation because the insurer has to answer the report, not just dismiss the owner's opinion.

Why certification matters in adversarial claims

A classic car claim becomes adversarial quickly when the carrier relies on weak comparables, incomplete condition assumptions, or software logic that doesn't fit collector vehicles. Certified appraisals help because they document what the insurer may have overlooked or simplified.

That includes things like:

- verified condition

- restoration quality

- originality

- modifications and whether they help or hurt value

- maintenance and restoration records

- market support drawn from collector-specific sources

The appraisal clause and the real playing field

One of the most important practical points is that a qualified independent appraiser may be able to invoke the Appraisal Clause in an auto policy when that option applies. That can move the dispute away from the insurer's internal valuation process and into a structured disagreement between appraisers.

For owners, that matters because it changes the venue of the fight. You're no longer trapped inside the insurance company's own valuation system. You have a path to put your evidence in front of professionals who have to engage with the actual market and the actual vehicle.

That's the strategic value of classic car appraisal certification. It gives your position form, credibility, and staying power when the insurer's first number is not good enough.

If you're dealing with a total loss, diminished value dispute, or a low settlement on a collector vehicle, Total Loss Northwest provides certified independent appraisals built for negotiation. Their work is focused on giving owners a defensible value position and, when appropriate, invoking the appraisal clause to get the claim out of the insurer's biased software process and into a fairer valuation framework.