You've probably already had the call.

The adjuster sounded calm, efficient, and certain. They asked a few questions, told you what they think your car is worth, and moved the claim along as if the number came from some neutral machine. But when you heard the settlement offer, or got the estimate after repairs, your gut told you something was off.

That instinct is usually right. Insurance companies use valuation software to control payouts. You're dealing with a claim tied to a real vehicle, with a real history, in a real local market. Their system is dealing with averages. That gap is where money gets left on the table.

For drivers in Oregon and Washington, this holds greater significance than generally acknowledged. Vehicle ownership is widespread. 91.7% of American households had at least one vehicle in 2022, 37% had exactly two, and 22.1% had three or more according to Forbes Advisor's review of U.S. Census and transportation data. When one vehicle gets hit, the financial damage spreads into work, family logistics, and future resale value fast.

If you're serving vehicle owners statewide, you don't need vague advice. You need a clear path to challenge a bad number and get a fair one.

After the Accident Navigating Your Vehicle Claim in Oregon and Washington

The first day after a crash is messy. You're juggling the repair shop, the other driver's insurer, your own carrier, maybe a rental, maybe a missed shift at work. Then the valuation conversation starts, and suddenly the company with all the data claims your vehicle is worth less than you know it is.

That's where a lot of owners get pushed into accepting the wrong outcome. They hear “comparable vehicles,” “market valuation,” or “standard methodology,” and assume the number must be objective. It usually isn't.

Why drivers feel blindsided

A repaired car isn't the same as a clean-history car. Buyers know that. Dealers know that. Insurers know that too, even if they don't lead with it on the phone.

Data shows that 68% of accident-repaired vehicles experience a 10–25% reduction in market value, yet only 12% of eligible owners pursue diminished value claims according to Car Consumers. That tells you two things. First, value loss after repairs is common. Second, most owners never make the claim they could have made.

Practical rule: If the insurer is talking only about repair cost, they may be skipping the separate issue of lost market value.

That's why basic post-crash steps matter. If you need a plain-language checklist on documentation, medical follow-up, and preserving your claim, this guide on protecting your rights after an accident is worth reading early.

What to do before you agree to anything

Don't assume the first offer is complete. Don't assume the software looked at your vehicle the way a buyer would. And don't assume a repaired vehicle claim ends when the body shop is done.

A smart owner starts collecting the documents that move a valuation dispute:

- The insurer's written offer: Verbal explanations don't help later.

- Photos and repair records: These show severity and repair scope.

- Your vehicle details: Trim, options, mileage, condition, and service history matter.

- Any valuation report or CCC-style estimate: You need to see what they relied on.

If you need help organizing the claim and responding to the insurance company, use dedicated insurance claim support before you sign off on their number.

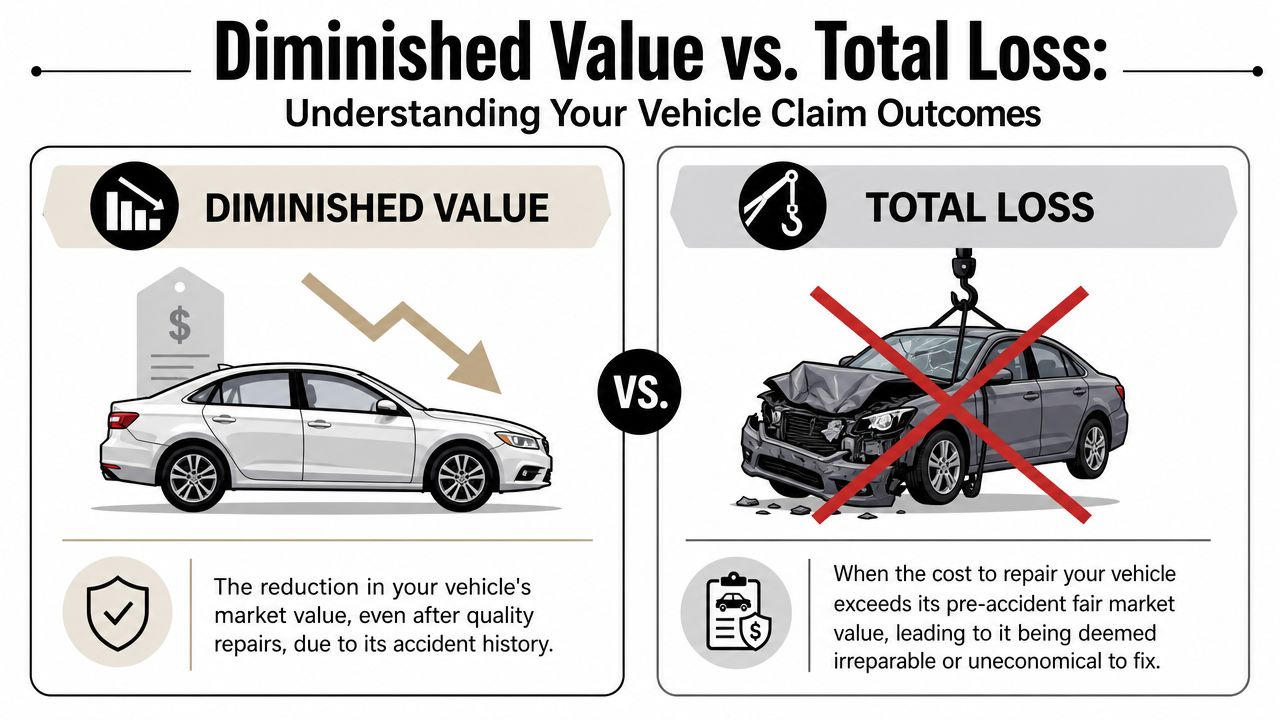

Diminished Value vs Total Loss Explained

Most drivers hear these terms after the accident, not before it. That's a problem, because diminished value and total loss are not the same claim, and confusing them costs people money.

Diminished value means your car was repaired but still lost value

Think about a used phone. If two identical phones sit on a table and one had a cracked screen professionally replaced, buyers still prefer the one that was never damaged. Cars work the same way, except the money involved is much bigger.

A vehicle with an accident history carries a stigma in the market. Buyers, dealers, and appraisers account for that history when they price it. Diminished value claims are legally recognized under tort law, which requires compensation for repair costs plus the difference between pre-accident and post-repair value, and that loss can be 10–25% in markets like the Pacific Northwest according to this diminished value explanation.

That means a body shop can do excellent work and you can still be owed money.

Total loss means the insurer decides not to repair

A total loss happens when the insurance company decides the vehicle won't be repaired under the claim. The fight then shifts from “what value did I lose after repair?” to “what was my vehicle worth right before the crash?”

Here's the simplest comparison:

| Claim type | What happened to the car | What you're fighting over |

|---|---|---|

| Diminished value | Repaired and returned to you | The drop in resale value caused by accident history |

| Total loss | Declared uneconomical to repair | The pre-accident fair market value |

The insurer likes when owners blur these categories, because confused claimants ask the wrong questions.

A short overview helps if you want to hear the distinction explained visually:

Why this distinction changes your next move

If your vehicle is repaired, you're looking at whether the market now sees it as worth less.

If your vehicle is totaled, you're looking at whether the insurer undervalued its condition, trim, upgrades, mileage, or local market demand before the crash.

A repaired claim is about loss after the work. A total loss claim is about value before the wreck.

Those are different fights. They require different evidence, different timing, and often a different strategy with the carrier.

Why Your Insurer's Offer Is Just a Starting Point

The insurer's first number is not a verdict. It's an opening position.

That point matters because too many drivers treat the company's valuation as if it came from a court, not a claims system. It didn't. It came from software, internal rules, and a process built to create consistency for the insurer. Consistency for them doesn't mean fairness for you.

What the software gets wrong

Automated valuation tools flatten details. They can miss condition. They can miss upgrades. They can miss the effect of local demand. They can also ignore how buyers react to accident history, especially with premium, collector, or custom vehicles where “average” comps are worthless.

That's why independent appraisal matters. A real appraiser isn't just plugging data into a template. A real appraiser is challenging the assumptions behind the insurer's number.

Here's the part most guides skip. The bargaining power typically arises from the Appraisal Clause in the policy.

The Appraisal Clause changes the power dynamic

The Appraisal Clause gives you a formal way to dispute value. Instead of begging the adjuster to reconsider, you invoke a contract mechanism that forces a valuation process outside the insurer's preferred software lane.

That's the difference between asking nicely and asserting a right.

Invoking the Appraisal Clause was highly effective in recent premium vehicle disputes. In 41% of those cases, initial insurer valuations under $15,000 were corrected to over $22,000 after an independent appraiser was brought in, according to Consumer Watchdog. Those figures are tied to premium vehicles, but the lesson applies broadly. The insurer's first number can be wrong by a lot.

The adjuster's valuation is often the starting line, not the finish line.

What an appraiser actually does when the clause is invoked

An independent appraiser doesn't wave a hand and “override” the insurer. They replace weak assumptions with evidence. They review the vehicle itself, the market, the condition, and the flaws in the insurer's comp selection. Then they issue a defensible valuation that can survive scrutiny.

That matters statewide because the tactic is practical whether you drive a commuter sedan, a truck, or something harder to value. If the carrier is leaning on software and you're leaning on facts, your position gets stronger fast.

The wrong move is waiting for the insurer to volunteer that option. They usually won't.

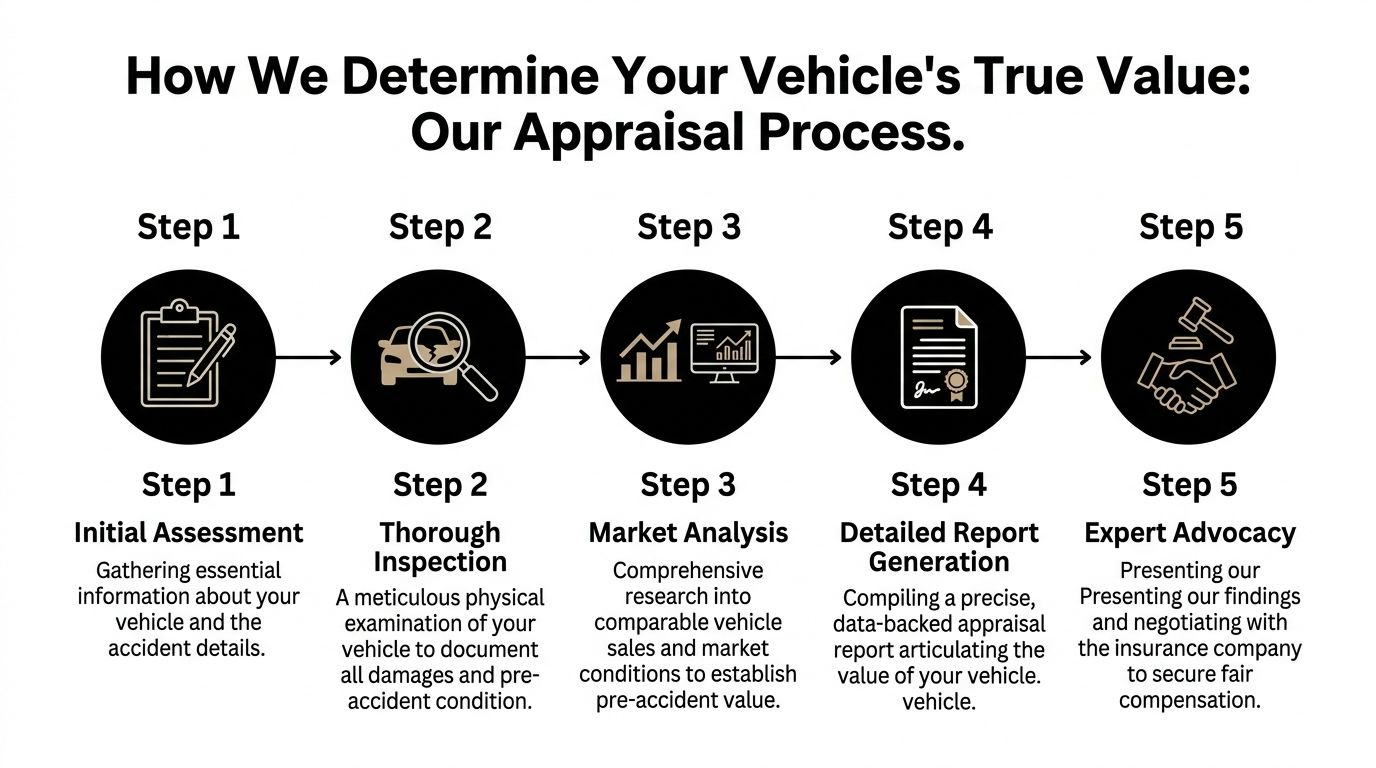

How We Determine Your Vehicle's True Value

A credible appraisal is built, not guessed. If you want a fair settlement, you need a report that can stand up in negotiation, in a dispute, and if necessary, in a more formal challenge.

Step one is getting the right facts in front of the appraiser

The process starts with the basics, but not the watered-down version insurers prefer. The appraiser needs the VIN, trim, mileage, ownership details, condition before loss, damage details, repair records if the vehicle was fixed, and every insurer document tied to value.

That first review usually reveals the problem quickly. Maybe the insurer compared your vehicle to weaker comps. Maybe they ignored options. Maybe they treated prior condition like an average fleet unit instead of a well-kept owner vehicle.

A lot of owners never realize how important pre-loss market value is until they see how insurers frame it. If you need a deeper look at the mechanics, this guide on how to calculate fair market value helps explain what should go into the number.

Step two is inspection and market analysis

A serious appraiser looks at the vehicle, the records, or both, depending on the claim and logistics. Some claims need in-person inspection. Others can be handled remotely if the photo set, damage documentation, and records are strong enough.

Then comes the part software can't do well. Real market analysis.

That means reviewing comparable vehicles and evaluating whether those comps are comparable. Same model isn't enough. Condition, equipment, mileage, region, and market behavior all matter. For diminished value, the appraiser also has to analyze how accident history changes what buyers will pay.

Step three is producing a report that can hold up

Weak appraisals fall apart here. A short opinion letter won't do much if the insurer pushes back.

A USPAP-compliant appraisal report must define the value type, describe the methodology, present supporting evidence, and include the appraiser's signed certification, as outlined by Certified Auto Appraisers. The methodology may include tools like the 17C formula, but its key strength comes from documented evidence and a clear explanation of how the conclusion was reached.

What matters most: a report should show its work. If the valuation can't be traced, the insurer will attack it.

A proper report typically addresses:

- Vehicle identification: VIN, year, make, model, trim, and relevant equipment.

- Purpose of the appraisal: Diminished value, total loss, dispute support, or another defined use.

- Valuation method: The framework used and why it fits the claim.

- Evidence set: Comparable sales, condition data, repair information, and market context.

- Certification: Signed appraiser certification and required disclosures.

One option for owners in Oregon and Washington is Total Loss Northwest, which provides certified diminished value and total loss appraisals and can invoke the Appraisal Clause as part of the dispute process.

Why independence matters more than people think

An appraiser has to be independent. If the person valuing the vehicle is financially tied to the insurer, the report loses force before the argument even starts.

That's why owners should ask hard questions. Is the appraisal written to recognized standards? Does it explain the value conclusion? Will it survive if the insurer challenges every comp and every assumption? If the answer is no, you don't have a strong position yet. You just have paperwork.

Your Action Plan to a Fair Settlement

If the insurer's number feels light, don't freeze. Act in order.

First moves that protect your leverage

Don't sign a final release too early

Once you sign away rights, your options narrow fast. Read every settlement document before you agree to anything.Don't assume the check ends the dispute

A payment can create pressure to move on, but pressure isn't accuracy. Review what the payment is supposed to cover.Collect every claim document in one place

You want the estimate, valuation report, repair records, photos, insurer emails, and policy language if you have it.

If the insurer controls the paperwork and the timeline, they control the pace of the claim. Take that back.

Then get strategic

Your goal isn't to argue emotionally. Your goal is to create a documented valuation challenge.

- Identify the claim type: Is this diminished value, total loss, or both issues at different stages?

- Check the insurer's assumptions: Look for bad comps, missed options, and generic condition adjustments.

- Ask whether the Appraisal Clause applies: If it does, use it deliberately.

- Get an independent valuation: You need evidence, not frustration.

If the dispute is already active, focused loss settlement negotiation support can help frame the right response instead of sending the insurer another email they'll ignore.

What not to do

Don't rely on a dealer's casual opinion. Don't send screenshots of random listings and think that's the same as an appraisal. And don't let the adjuster convince you that challenging value means you're being difficult.

You're not being difficult. You're forcing the claim onto factual ground.

Timelines Deliverables and Expected Outcomes

Most owners want two answers after they decide to challenge a valuation. How long does this take, and what do I receive?

The honest answer is that timing depends on the records, the vehicle, and how fast the insurer responds. A simple claim with complete documentation moves faster than a disputed high-value vehicle with missing repair information. What matters is that the process produces something useful, not just fast.

What you should expect to receive

A proper deliverable is a written appraisal report. Not a vague estimate. Not a one-line email. A report.

That report should tie together the vehicle facts, valuation method, supporting market data, and the appraiser's signed conclusion. If your claim heads into a tougher negotiation, that document becomes the backbone of the argument.

A useful deliverable usually includes:

| Deliverable | Why it matters |

|---|---|

| Vehicle identification and condition summary | Shows the insurer exactly what was valued |

| Comparable market support | Replaces weak or misleading comps |

| Valuation conclusion | Gives a clear number tied to evidence |

| Formal certification | Adds credibility in negotiation and disputes |

Why older vehicles need extra care

This issue gets sharper in Oregon. The average vehicle age in Oregon is 14.5 years, compared with the national average of 12.2 years, according to Self Financial's vehicle ownership data. Older, well-maintained vehicles are easy for automated systems to undervalue because software tends to flatten condition and treat age as the whole story.

That's a mistake. A carefully maintained older vehicle can have a stronger real-market value than a generic database estimate suggests.

Older doesn't mean low value. It means condition and market evidence matter more.

What outcome is realistic

A good appraisal doesn't guarantee instant agreement. It gives you a solid basis to challenge the insurer with something stronger than opinion. Sometimes that leads to a revised offer quickly. Sometimes it leads to a longer dispute. Either way, the conversation changes because the insurer now has to answer evidence instead of brushing off objections.

That's the practical benefit of serving vehicle owners statewide with formal appraisals. The goal isn't drama. The goal is a number the insurer can no longer defend against serious scrutiny.

Common Questions from Drivers We Help

I wasn't at fault. Does the other insurance company have to pay diminished value

In many claims, a not-at-fault owner can pursue diminished value from the at-fault party's insurer. The key issue is whether your vehicle lost market value because of the crash, even after proper repairs. You still need proof. The fact that you weren't at fault helps your legal position, but it doesn't replace the need for a documented appraisal.

My vehicle is custom, collector, or high-end. Can the insurer still use generic comps

They can try. That doesn't make those comps reliable. Specialty vehicles often get mishandled because standard valuation systems prefer easy categories and broad averages. If your vehicle has rare options, modifications, provenance, unusual condition, or a narrow buyer market, a generic database approach is exactly what you should challenge first.

Do I need an appraisal if the adjuster says their number is non-negotiable

Yes, if you believe the value is wrong. “Non-negotiable” usually means they don't want to revisit it informally. It doesn't erase your right to dispute value through the policy process and independent evidence.

Is the Appraisal Clause only useful in one state

No. The mechanism is used nationwide through policy language, which is why it matters so much for owners who think the insurer's software has the final say. The legal details of the claim still depend on the policy and the dispute, but the clause is often the practical tool that shifts the matter into a real valuation process.

What should I have ready before I contact an appraiser

Bring the insurer's valuation, repair estimate or total loss paperwork, photos, VIN, mileage, options list, and anything showing pre-loss condition. The faster an appraiser can see the full file, the faster they can identify where the insurer cut corners.

If your insurance company is leaning on software and you know the number is wrong, get a real valuation behind you. Total Loss Northwest handles diminished value and total loss appraisals for Oregon and Washington vehicle owners and supports Appraisal Clause disputes with certified, evidence-based reports.