You get the call from the adjuster. The body shop says the damage doesn't look catastrophic, but the insurer says your car is a total loss. Then the offer arrives, and it feels low. Lower than what it would take to replace the vehicle you owned, with its condition, options, maintenance history, and local Spokane market value.

That's where most drivers get stuck. They assume “totaled” means the insurer's number must be final. It isn't.

A total loss settlement in Spokane follows Washington rules, not guesswork. If you understand how the state's formula works, how Actual Cash Value is built, and how to use the appraisal clause in your policy, you can push back in a way that's organized, credible, and hard to ignore.

Your Car Is Totaled in Spokane Now What

The first mistake I see is panic-driven agreement. A driver loses transportation, misses work, starts worrying about a loan payoff, and signs before reviewing anything. That's exactly when bad valuations slip through.

If you're in that spot right now, slow down. A total-loss decision creates pressure, but it also opens a review process. You need the insurer's valuation report, the repair estimate, and the salvage figure before you decide whether the offer is fair. If you need a practical starting checklist, what to do when your car is totaled lays out the immediate next steps.

What usually happens in the first few days

The adjuster inspects the vehicle or reviews shop documentation. A repair estimate is written. Then the insurer runs its total-loss math and valuation.

The frustration usually starts when the owner hears two things at once:

- The car is not being repaired

- The settlement amount won't buy a comparable replacement easily

Those are separate issues. Whether the car is totaled and whether the value is correct are not the same question.

Most bad total-loss outcomes happen because the owner argues with the conclusion, but never audits the numbers behind it.

What helps and what doesn't

What helps is document-driven pushback. That means checking trim, mileage, condition adjustments, options, recent repairs, and local comparable vehicles. What doesn't help is telling the adjuster the offer “feels wrong” without evidence.

You don't need to be a lawyer to challenge a low offer. You need to understand the valuation process better than the insurer expects you to.

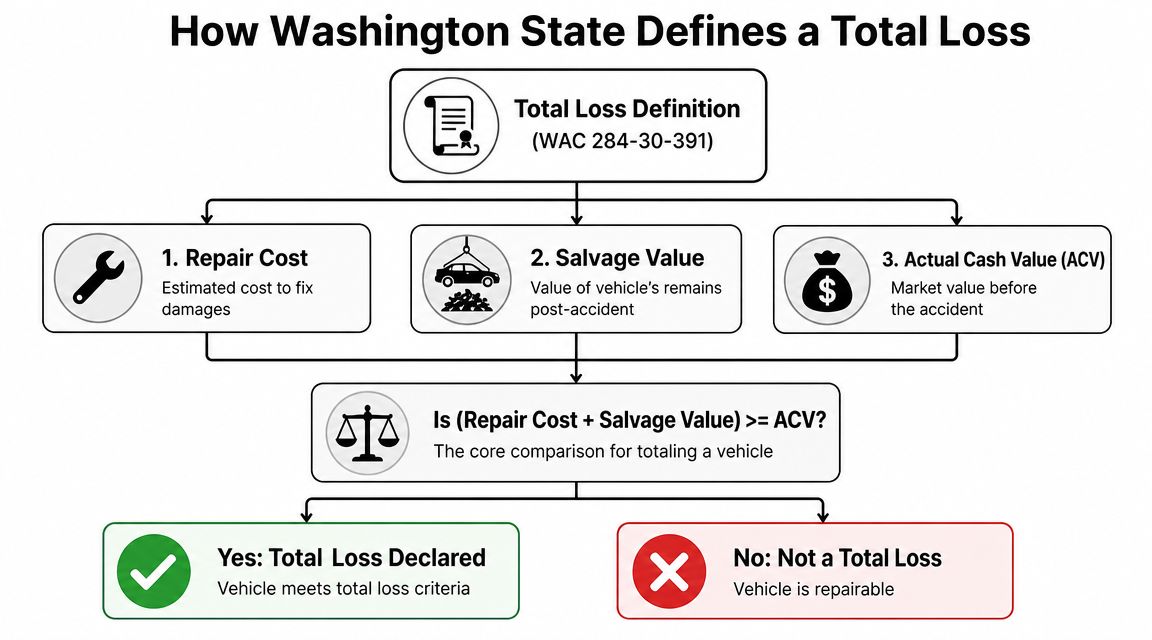

How Washington State Defines a Total Loss

Washington doesn't use a simple one-line percentage rule as the legal definition. It uses a Total Loss Formula, often shortened to TLF.

Under WAC 284-30-391, a vehicle is a total loss when repair cost plus salvage value equals or exceeds Actual Cash Value. Washington insurers must use that formula when deciding whether repair is financially viable, as explained in this Washington total-loss overview.

The formula in plain English

Think of it as a financial point of no return.

If the insurer would have to spend too much repairing the vehicle, and the damaged vehicle still has salvage value, the claim can cross the line where repairing it no longer makes economic sense under Washington's rule. At that point, the insurer owes a total-loss settlement instead of authorizing repairs.

Three values matter:

- Repair cost. What it would take to fix the accident damage.

- Salvage value. What the damaged vehicle is worth in its current state.

- Actual Cash Value. What the vehicle was worth right before the loss.

Why Spokane drivers get confused

A lot of drivers hear adjusters talk in percentage language. That happens because insurers may use internal thresholds during claim handling, but Washington's legal framework is the formula above, not a shortcut percentage.

That distinction matters. If a company representative talks loosely about a threshold, ask for the actual repair estimate and salvage figure. The total-loss decision should be supportable with numbers, not just a label.

Practical rule: Don't argue “my car shouldn't be totaled” in the abstract. Ask whether the repair estimate, salvage value, and ACV were all calculated accurately.

The real fight is usually not the total-loss label

In many Spokane claims, the stronger dispute is not whether the insurer can total the car. It's whether the insurer undervalued the car before applying the formula. A low ACV can make a total-loss decision look clean on paper even when the owner is being underpaid.

That's why the valuation report matters more than is commonly understood.

How Insurers Calculate Actual Cash Value

Actual Cash Value, or ACV, is the number at the center of nearly every total-loss dispute. It isn't your loan balance. It isn't what you paid when you bought the car. It also isn't a guaranteed “average” payout figure.

Washington doesn't have a fixed average settlement amount for these claims. Value depends on the facts of the case, and in total-loss situations the ACV is determined from comparable market data rather than a statutory average, as noted in this Washington claim value discussion.

If you want a deeper primer on the concept itself, how auto insurance Actual Cash Value works is worth reviewing before you respond to the adjuster.

What the insurer is trying to measure

The target is simple: what your vehicle would have sold for in the local market immediately before the crash.

In practice, the insurer usually uses a valuation report built from comparable vehicles. Those comparables are adjusted up or down based on details such as:

- Mileage

- Trim level

- Drive type and engine

- Factory options

- Overall pre-loss condition

- Prior damage or wear

- Local market availability

That process sounds objective. Sometimes it is. Sometimes it isn't.

Where ACV reports go wrong

I regularly see reports that look polished but contain basic mistakes. The wrong trim package. Missing leather or technology packages. Condition deductions that don't match the actual vehicle. Comparables from outside the relevant market. Recondition adjustments that feel detached from reality.

Small errors stack. The insurer doesn't need one dramatic mistake to lower value. Several modest deductions can push the offer down enough that the owner either gives up or settles under pressure.

Use this quick review grid when you read your report:

| Item to review | What to check | Why it matters |

|---|---|---|

| Trim and model | Exact badge and package | A base model is not equivalent to an upgraded trim |

| Mileage | Odometer accuracy | Mileage adjustments affect value directly |

| Options | Sunroof, safety tech, premium audio, tow package, etc. | Missing equipment lowers the ACV |

| Condition | Seats, paint, tires, glass, maintenance | Generic deductions can be overstated |

| Comparables | Same body style, equipment, and market area | Weak comps distort replacement cost |

What owners often misunderstand

A financed vehicle can be worth less than the loan balance. A well-maintained vehicle can still be undervalued if the report ignores maintenance history. And a “book number” doesn't control the claim if the actual local market supports a different replacement value.

When the insurer says, “This is what the software came back with,” treat that as the start of the conversation, not the end of it.

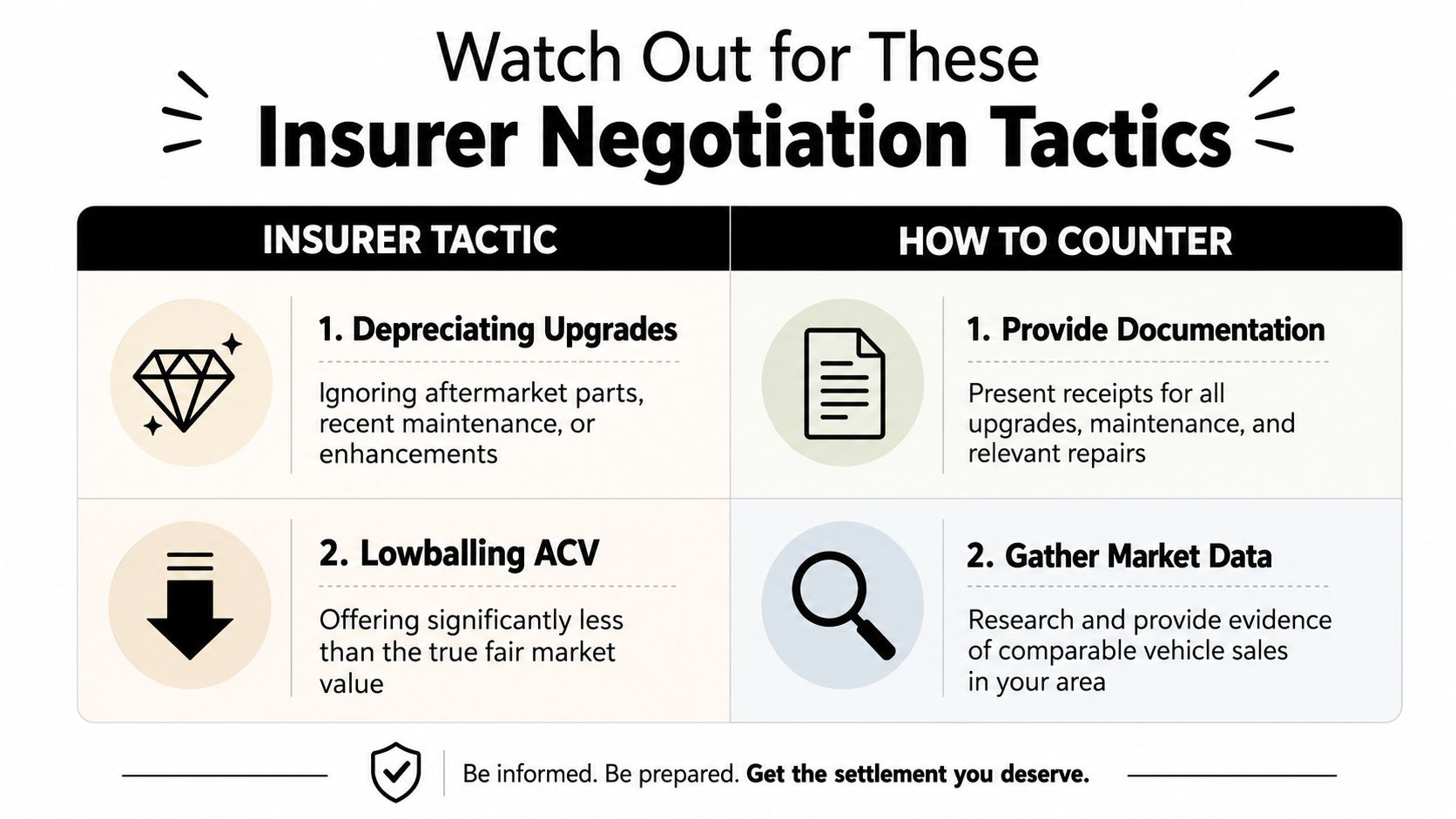

Watch Out for These Insurer Negotiation Tactics

Most adjusters won't describe what they're doing as a tactic. They'll call it standard process. But some patterns show up often enough that Spokane drivers should recognize them immediately.

One overlooked issue is Total Loss Threshold ambiguity. Another is the salvage retention trap. A discussion of those problems notes that insurers often use generic 70-75% thresholds without disclosing the internal formula, and that repair costs for relatively minor damage can still trigger a total-loss declaration. The same discussion also warns that insurers may deduct estimated salvage value from the payout without verifying actual market salvage prices, which can leave the owner shortchanged if they want to keep the vehicle. See that breakdown in this total-loss settlement analysis.

The threshold conversation that goes nowhere

Some owners get told the vehicle crossed a percentage threshold, as if that settles everything. It doesn't. If the insurer is discussing the claim in threshold language, ask for the actual repair estimate and ask how salvage was handled. You need the numbers, not shorthand.

This matters most when the visible damage looks modest. Cosmetic damage, parts pricing, calibration requirements, and labor can push repairs high quickly. But the insurer still needs a supportable file.

The salvage retention deduction problem

If you want to keep the wrecked vehicle, the insurer will usually reduce the settlement by the salvage amount. That's where disputes start.

The deduction might not reflect what the damaged vehicle would bring in the relevant market. If the carrier uses a weak or inflated salvage assumption, the owner gets squeezed twice. First on ACV, then again on the retention deduction.

The comparables game

Another common issue is weak comparable selection. That can show up in several ways:

- Lower trim substitutes that make your vehicle look less valuable than it was

- Poor condition comparisons where rougher vehicles are treated as equivalent

- Incomplete option matching that ignores premium equipment

- Market mismatch where the listed vehicles don't reflect what it would cost to replace yours in the Spokane area

If a comparable wouldn't be an acceptable replacement for you, it shouldn't be acceptable for the valuation report either.

The important point is this: these aren't fixed facts. They're negotiable inputs.

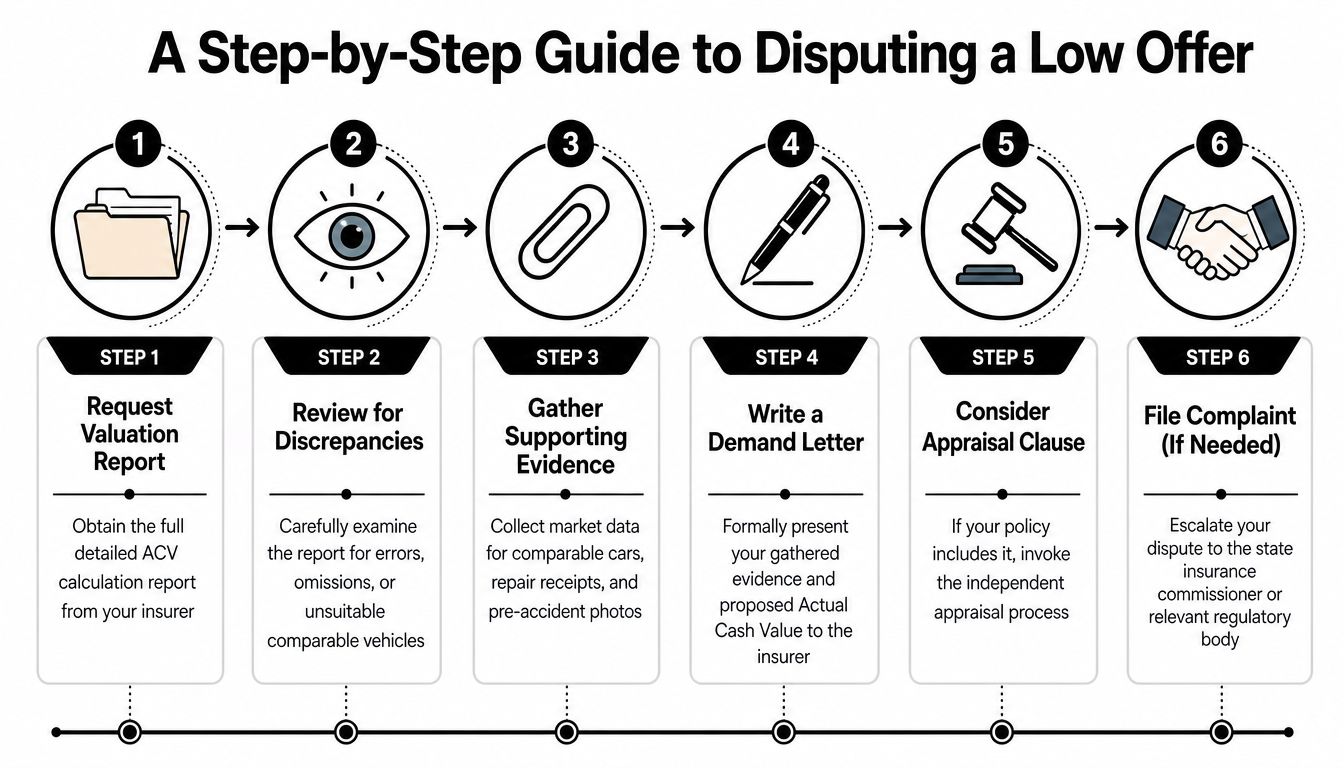

A Step-by-Step Guide to Disputing a Low Offer

A low offer doesn't mean you're out of options. It means you need to move from frustration to documentation.

Start with the report. Then work outward.

Step one, get the complete valuation report

Ask for the full ACV report in writing. You want the comparables, adjustments, options list, condition ratings, and any deductions used to reach the number.

Don't accept a summary page. A summary tells you the result. The full report tells you whether the result is defensible.

Step two, audit every line item

Read it slowly. Owners often scan the final value and miss the inputs.

Check these first:

- Vehicle identity. Year, make, model, trim, drivetrain, body style.

- Equipment list. Factory packages and higher-value options.

- Condition adjustments. Any deduction for interior, exterior, tires, prior repairs, or mechanical condition.

- Comparable vehicles. Are they comparable in equipment and market relevance?

If the insurer missed a package, used the wrong trim, or assigned excessive condition penalties, your counter should focus there first.

Step three, build your evidence file

Your strongest evidence is replacement-market proof and vehicle-specific documentation.

Use a file that includes:

- Comparable listings for vehicles that match yours in trim, equipment, and general condition

- Service records showing maintenance and recent work

- Receipts for parts, upgrades, or repairs that affected pre-loss condition

- Photos taken before the accident, if you have them

- A written correction list that identifies each error in the insurer's report

Short, organized evidence beats emotional volume every time.

What works: a clean packet with corrections, comps, and records.

What doesn't: a long email saying the offer is insulting.

Step four, send a written counteroffer

Your response should be specific. Identify the report errors, explain why each one matters, and state the corrected value you believe is supported by the market.

Keep the tone professional. You're not asking for a favor. You're disputing a valuation.

A useful counteroffer usually does three things:

- Corrects factual errors in the report

- Replaces weak comparables with better ones

- Ties the requested ACV to documented market evidence

Step five, use the appraisal clause if negotiations stall

This is the underused tool that changes the dynamics.

Many auto policies include an appraisal clause. It's a dispute-resolution provision for value disagreements. If you and the insurer can't agree on ACV, each side selects an appraiser. The appraisers then work through the valuation dispute under the policy process.

That matters because it moves the claim away from one-sided software output and into a structured valuation dispute. It's not a lawsuit. It's not a generic complaint. It's a policy-based mechanism designed for exactly this kind of disagreement.

If you don't know whether your policy includes it, ask for the relevant policy language. Read the appraisal provision carefully before signing a release.

A certified independent appraiser can help here. One option is Total Loss Northwest, which provides total-loss appraisal support and can invoke the appraisal clause on behalf of Washington vehicle owners when a claim turns into a valuation dispute.

Step six, escalate only after you've built the record

Complaints to regulators can matter, but they're not a substitute for valuation evidence. Build the file first. Correct the report first. Use the policy tools first.

This video gives a useful overview of the dispute mindset before you sign anything:

When the insurer sees a documented challenge backed by policy language and market support, the conversation changes.

Understanding the Settlement Timeline and Paperwork

A lot of stress in a total loss settlement in Spokane comes from not knowing what happens next. The administrative side feels simple until the money, title, lender, and deadlines all start colliding.

A Washington total-loss settlement can move fast or drag out. The process typically ranges from a few days to over a month, with straightforward claims often resolving in about 10 business days, according to this Washington total-loss process overview. That same source notes that owners must report the total loss and surrender title to the Department of Licensing within 15 days, and that when a vehicle is financed, the insurer pays the lender first.

What the timeline usually looks like

Once the insurer finalizes value and you agree to settle, the remaining steps are mostly administrative. You sign the required paperwork, transfer title, and wait for funds to be issued.

Disputes change the timing. If you challenge the valuation, ask for supporting documents, or invoke appraisal, the process slows down. That's normal. Faster is not always better if the fast version leaves money on the table.

The loan payoff issue

If you still owe money on the vehicle, the insurer generally sends payment to the lender first. If the settlement is less than the payoff amount, you may still owe the balance unless you have GAP coverage.

That surprises people, especially with newer vehicles or long-term financing. The claim pays ACV, not the amount remaining on your loan contract.

Sample settlement calculation

Below is a simple framework for how the claim is commonly broken down. The amounts will vary by case.

| Line Item | Amount | Notes |

|---|---|---|

| Actual Cash Value | Varies by claim | Based on the insurer's valuation of the pre-loss vehicle |

| Salvage deduction if retained by owner | Varies by claim | Applies if you keep the damaged vehicle |

| Lender payoff | Varies by claim | Paid first when there is an active loan |

| Net payment to owner | Varies by claim | What remains after applicable deductions and lender payment |

Paperwork mistakes to avoid

- Signing too early. Don't sign a release before you're satisfied with the valuation.

- Ignoring the title deadline. Washington requires title surrender within the stated timeframe after total loss reporting.

- Assuming the check comes to you first. If there's a lender, it usually doesn't.

- Giving up your bargaining position before review. Once the claim is finalized, reopening value disputes gets much harder.

A quick settlement feels good for one day. A correct settlement matters much longer.

Taking Control of Your Spokane Total Loss Claim

A total-loss claim feels like the insurer holds all the cards. In Washington, that isn't true.

Your claim sits on numbers that can be checked. The total-loss decision depends on a formula. The settlement depends on ACV. The ACV depends on a valuation report that may contain mistakes, weak comparables, or unsupported deductions. And if the insurer won't move, the appraisal clause can shift the dispute into a process built for value disagreements instead of endless back-and-forth with an adjuster.

That's the part many drivers miss. You do not have to accept the first number because the car was declared totaled.

If you're dealing with a low total loss settlement in Spokane, review the report before you sign anything. Challenge factual errors. Push back on bad comparables. Question salvage deductions if you're retaining the vehicle. Ask for the policy language on appraisal if negotiations stall.

For added help with Washington-specific claim issues, Washington claim support resources can help you understand the next move before you lock in a bad settlement.

If your insurer's total-loss offer doesn't match what it would cost to replace your vehicle, contact Total Loss Northwest. A certified independent appraiser can review the valuation, identify report errors, and help you use the appraisal clause when the insurer won't offer a fair number.