The crash is over. The tow truck is gone. Your neck still hurts, your schedule is wrecked, and now the insurance company sends a neat little PDF telling you what your car was “worth.”

You look at the number and know it's wrong.

That reaction is usually correct. A total loss offer is not some sacred fact handed down from a neutral machine. It's the insurer's first position in a negotiation. They may call it an actual cash value determination. You should read it as an opening bid.

If you're searching for a vehicle valuation report Seattle drivers can use, start with one idea: the insurer's report is challengeable. In Washington, you have tools. Applying them correctly gives you an advantage.

Your Car Is Totaled The Insurance Offer Is Here Now What

Many individuals make the same mistake in the first 24 hours. They treat the carrier's number like the final answer and start arguing from emotion instead of evidence.

That's exactly where insurers want you.

A common Seattle claim goes like this. Your car was in solid condition. You maintained it. You know what similar vehicles are going for. Then the insurer sends a valuation built from “comparable” vehicles that don't really match yours in trim, options, condition, or local demand. The number lands low, you call to complain, and the adjuster repeats that the valuation came from their system.

That system is not the final word.

One of the biggest problems is stale data. As Repairer Driven News reported in its discussion of why consumers may want to challenge vehicle valuations, insurer-generated reports often rely on samples 90+ days old, and that mismatch can contribute to undervaluation of 20–30% for vehicles under $50,000.

Treat the offer like a draft, not a verdict

If you owe money on the car, a low total loss figure hurts twice. First on the payout, then on the loan balance you still have to clear. If that's your situation, you should also get your finances organized quickly so the claim delay doesn't create a second problem. ReceiptsAI's guide to faster car loan payoff is a practical resource for that side of the equation.

Practical rule: Don't spend your energy saying the offer feels unfair. Show why the valuation is flawed.

A proper independent valuation changes the conversation. It forces the dispute away from “I disagree” and into “your report missed these facts, used weak comparables, and failed to reflect this market.”

What to do first

Before you say much to the adjuster, do these three things:

- Save every document: Keep the valuation report, settlement letter, photos, repair records, and any listing links you can find.

- Read the comparables line by line: The bad stuff is often hiding in plain sight. Wrong trim, missing options, poor condition comps, distant listings.

- Stop assuming the software is objective: Software only reflects the inputs and rules chosen by the insurer.

You're not asking for a favor. You're challenging a business decision with better evidence.

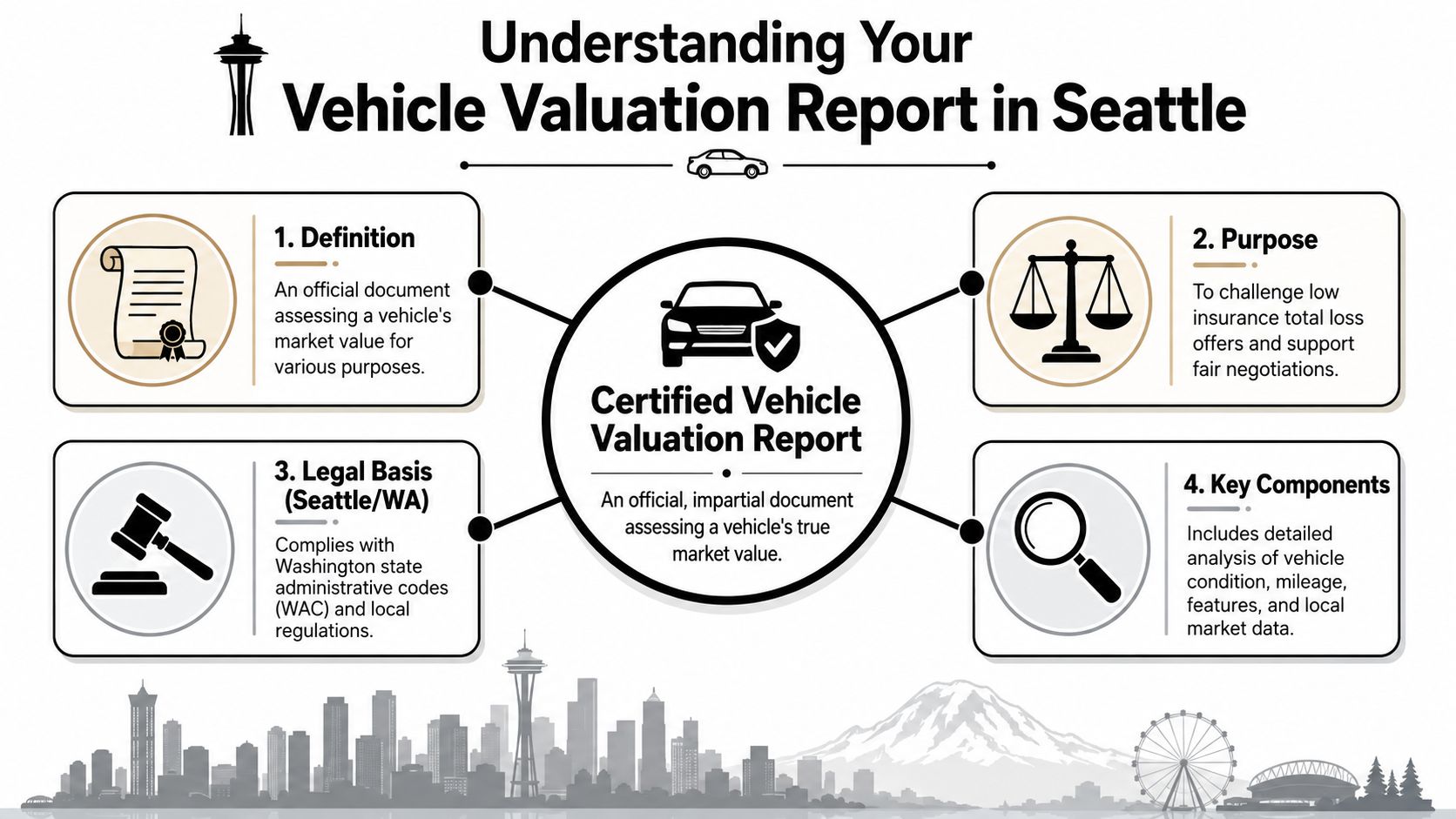

What Is a Vehicle Valuation Report

A vehicle valuation report is not a quick online estimate. It's a documented opinion of value built to hold up in a real dispute.

Think of it this way. A certified valuation report is the car-claim version of a home appraisal. It looks at the actual property, the relevant local market, the features, the condition, and the comparable sales. By contrast, the insurer's first number often acts more like a rough automated estimate. Useful as a starting point, maybe. Reliable as the last word, no.

What the report is supposed to do

A strong report answers one question clearly: What was this specific vehicle worth in the Seattle market immediately before the loss?

That means it should account for things generic tools miss, including:

- Actual condition: Not “average” condition pulled from a dropdown menu.

- Real equipment: Factory packages, tech, trim differences, and relevant options.

- Local comparables: Vehicles offered in the same market, not just broad regional noise.

- Defensible adjustments: Any change for mileage, condition, or equipment should be explained.

Why Seattle claims need a local report

Seattle is not a copy-and-paste market. Vehicle mix, demand patterns, and available inventory shape value in ways national tools often flatten out. A report built for this market has to reflect what buyers in this area pay attention to.

A valuation report should let you trace the number back to facts. If you can't see how the number was built, you can't test it.

That's why a random Kelley Blue Book screenshot won't carry much weight in a contested total loss claim. It's too broad. It doesn't inspect your vehicle. It doesn't tie its opinion to the exact claim date and local comparable set the way a serious report does.

What separates a real report from a casual estimate

Here's a quick comparison:

| Document | What it usually does | What it usually misses |

|---|---|---|

| Online estimate | Gives a fast broad value range | Specific condition, exact comparables, claim-ready support |

| Insurer valuation | Produces an ACV number for settlement | Full neutrality and often clear transparency |

| Independent valuation report | Builds a supportable market value opinion for dispute use | Nothing important, if it's done correctly |

When you order a vehicle valuation report Seattle claim, you're buying evidence. That's the point.

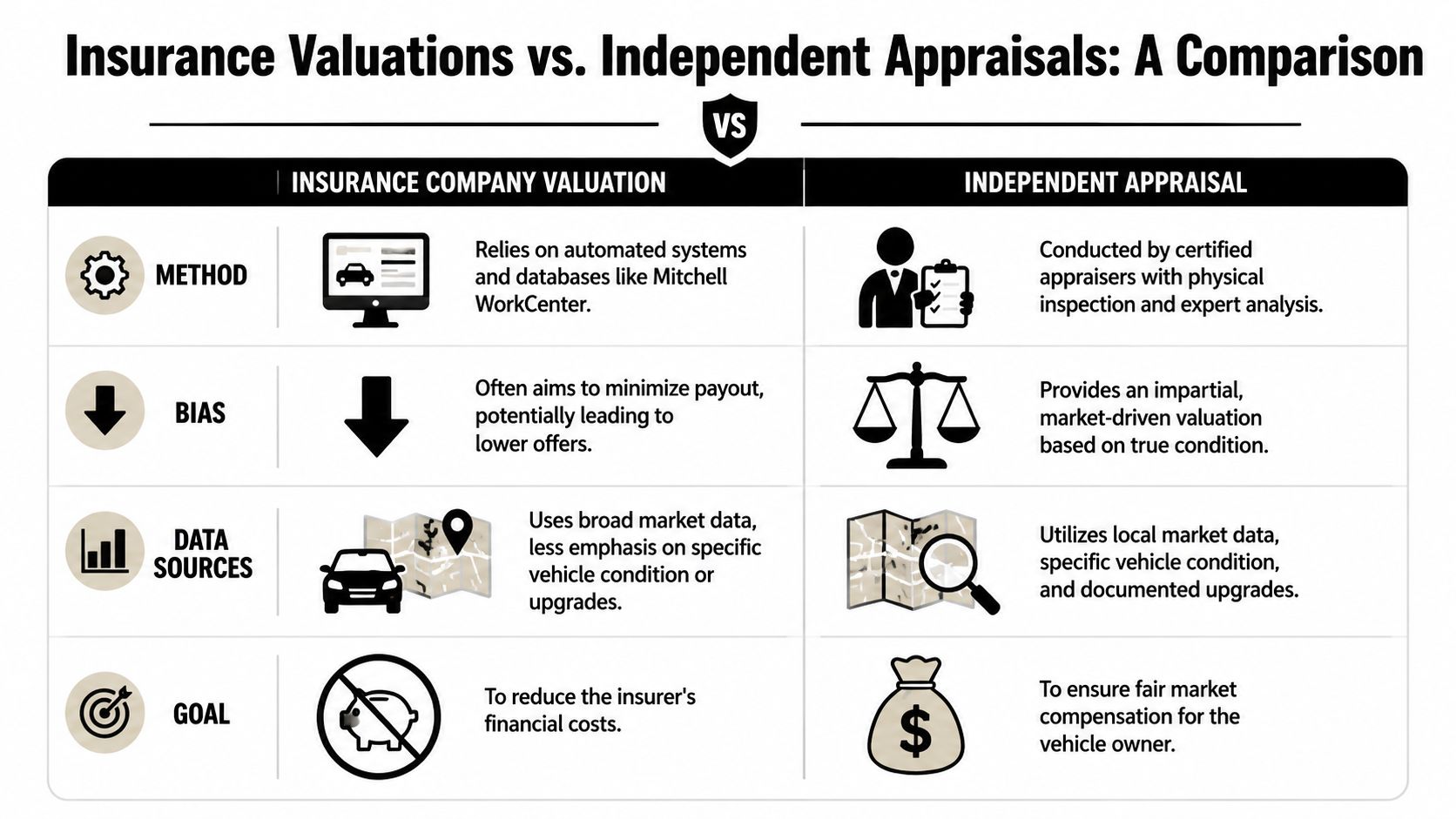

Insurer Valuations Versus Independent Appraisals

Insurers love the phrase “market value.” What they usually mean is “the value produced by our process.”

Those are not the same thing.

How the insurer usually builds the number

A lot of Seattle carriers use Mitchell WorkCenter Total Loss. According to Mitchell's description of the process, it works through five steps: locating comparable vehicles from AutoTrader, Cars.com, and Vast within the same market area, adjusting for projected sold price, mileage, and equipment, averaging adjusted prices to derive base value, applying loss vehicle adjustments for condition, prior damage, aftermarket parts, and refurbishment, and then computing market value. Mitchell also states that these regional adjustments can produce ACVs that differ by 8–12% from national averages.

That sounds clean on paper. In practice, a lot can go wrong.

The software can pull vehicles that are only “close enough.” The projected sold price adjustment can push numbers down from asking price. Condition grading can become harsh when the insurer controls the assumptions. Aftermarket items often get minimized. Prior damage can get treated like a lasting scar even when repairs were proper.

Why the conflict matters

The insurance company is not your appraiser. It is the party paying the claim.

That doesn't mean every adjuster is acting in bad faith. It does mean the entire system is built around cost control. If the software produces a lower supportable range, the insurer has every reason to start there.

Here's the side-by-side reality:

| Issue | Insurer valuation | Independent appraisal |

|---|---|---|

| Who the process serves | The carrier handling the payout | The vehicle owner seeking fair value |

| Comparable selection | Often software-led | Appraiser-led with judgment |

| Adjustments | Commonly opaque to the consumer | Should be explained and documented |

| Use in negotiation | Starting number | Counterweight with evidence |

A short explainer can help if you want to see how appraisal disputes are discussed in plain language:

What an independent appraiser does differently

An independent appraiser starts with the actual vehicle, not just a template. They look at trim, options, ownership history, condition indicators, local market fit, and whether the insurer's comparables are appropriately comparable.

The best appraisal reports don't just give a higher number. They explain why the insurer's lower number doesn't hold up.

A strong independent report also spots the hidden issues inside insurer reports, such as:

- Weak comparables: Same model family, different trim reality.

- Unsupported deductions: Mileage or condition adjustments that aren't explained.

- Market drift: Listings that don't reflect the market that existed on the date of loss.

- Equipment errors: Missing packages, wheels, safety tech, or premium features.

This is the inside baseball most drivers never get told. The fight is rarely about one dramatic mistake. It's usually about a stack of smaller valuation choices that all lean in the insurer's favor.

The Legal Power Behind Your Appraisal

Washington gives you more advantage than most drivers realize.

When an insurer uses a computerized source to determine actual cash value under Washington's WAC 284-30-391, that database must produce statistically valid values for at least 85% of all makes/models over 15 years, including major options. The same regulation also provides an appraisal path under WAC 284-30-391(3). In disputes involving Seattle's unusual mix of vehicles, these gaps can matter, and the appraisal process can replace the insurer's software-driven result with a real-market analysis. The same source notes that this often increases settlements by 10–15% for high-value or custom vehicles.

That matters because software coverage and software accuracy are not the same thing.

The appraisal clause is your pressure point

Many claimants never invoke the appraisal clause because nobody explains it early enough. They argue with the adjuster, send a few listings, get brushed off, and then accept less than the claim is worth.

The appraisal clause changes the power balance. It usually allows each side to retain an appraiser, and then the dispute moves into a structured value fight instead of an endless customer-service loop. If you want a plain-English overview of how that works in this state, review Washington appraisal clause guidance.

Why this works better than arguing on the phone

Phone calls are forgettable. Formal appraisal positions are not.

Use the law the way it's intended:

- Challenge the method, not just the amount: If the insurer relied on a weak computerized value, attack the foundation.

- Force specificity: Appraisal pushes both sides to show their work.

- Move the dispute out of routine claims handling: That alone can change the quality of the review.

If the insurer's number came from a black box, your answer shouldn't be another opinion. It should be a documented appraisal.

A lot of lowball disputes persist because the consumer keeps asking the carrier to fix its own work. That's backwards. Bring in an independent value opinion and make the insurer respond to evidence instead.

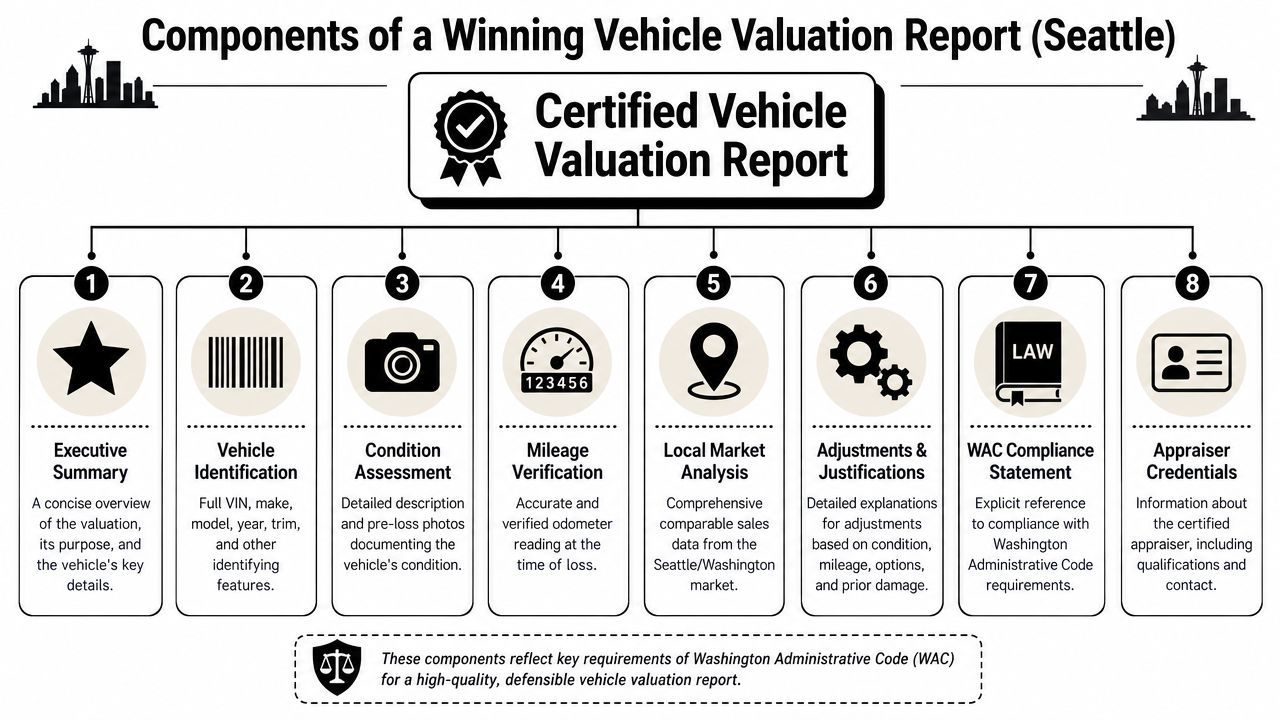

Anatomy of a Report That Wins Negotiations

A good report doesn't win because it's long. It wins because it's complete, traceable, and compliant.

In Washington, the legal checklist matters. Under WAC 284-30-392, a total loss valuation report must include all data from the initial inspection covering condition, equipment, and mileage, all information used to determine actual cash value, and a complete list of comparable vehicles used, with timestamps and geographic proximity not exceeding 150 miles from where the vehicle was principally garaged.

The parts that matter most

If your insurer's report is missing any of the following, that's not a minor paperwork issue. It goes to the credibility of the number.

- Inspection data: Condition, equipment, and mileage from the actual vehicle.

- Comparable list: Every comp used, not just a summary result.

- Dates and timestamps: You need to know when those vehicles were available.

- Distance from your market: The report can't wander too far from the garaging area.

- Adjustment logic: Mileage, condition, and equipment changes must be explained.

For drivers reviewing comparables on their own, this breakdown of comparables for appraisal helps you spot what belongs in a usable comp set.

What weak reports usually hide

A bad report often looks polished. That's the trick.

It might have glossy formatting, a final ACV figure, and several vehicle listings. But once you inspect it, you may find missing trim details, unexplained deductions, condition assumptions that don't match your car, or comps that are technically nearby but practically irrelevant.

Use this quick test:

| Question | Why it matters |

|---|---|

| Does the report show all comparables used? | If not, you can't test the selection. |

| Are adjustments explained? | If not, the number is just an assertion. |

| Do the comp vehicles actually match trim and equipment? | If not, the comparison collapses. |

| Are the dates tied closely to the loss? | If not, market relevance gets weaker. |

Red flag: If you can't recreate the logic behind the final value, the insurer hasn't given you a report. It has given you a conclusion.

What a winning report sounds like

A strong report is plain, specific, and disciplined. It doesn't rant. It documents.

That means the best vehicle valuation report Seattle disputes use will show what the subject vehicle was, what the market looked like, what comparables were selected, what adjustments were made, and why each adjustment was justified. Once that structure is in place, negotiation gets easier because the other side has to answer facts instead of brushing off frustration.

How to Get Your Own Vehicle Valuation Report

You don't need to become a claims expert overnight. You need a process.

Seattle-area total loss disputes work best when you move fast, stay organized, and stop letting the adjuster control the frame.

The sequence that actually works

Start with a written dispute. Keep it short. State that you disagree with the valuation, that you're obtaining an independent appraisal, and that you want all comparables and valuation inputs preserved.

Then hire someone who understands this market. A local appraiser matters because Washington's vehicle mix affects baseline value work. In Alliance For Automotive Innovation data for Washington, 2024 new car sales totaled 287,900, with pickups at 20.80%, passenger cars at 32.80%, and vans and minivans at 5.50%. That kind of market composition is exactly why a Seattle-specific appraiser matters. For local claim help, drivers often start by reviewing what a Seattle total loss appraiser should provide.

What to gather before the appraisal starts

Don't send random screenshots and hope for the best. Build a clean file.

Bring these items together:

- The insurer's valuation report: This is the document your appraiser needs to dismantle.

- Your vehicle records: Maintenance, upgrades, recent repairs, and ownership documents.

- Photos: Pre-loss photos if you have them, plus claim and damage photos.

- VIN and trim details: These help confirm exact equipment.

What the appraiser should do

A competent appraiser should inspect the facts, review the insurer's comparables, identify mismatches, locate better local market evidence, and prepare a written report you can submit formally.

Your job is simpler than you think:

- Dispute in writing

- Hire the right appraiser

- Provide complete records

- Review the finished report carefully

- Submit it and ask for a revised valuation

Don't overcomplicate this. The insurer already has a process. You need one too.

Avoiding Costly Mistakes in Your Valuation Journey

Most bad claim outcomes don't happen because the driver had no case. They happen because the driver made one avoidable mistake at the wrong time.

The first mistake is treating acceptance like a casual act. If you verbally agree too early, sign broad settlement paperwork, or cash a check without understanding the consequences, you can weaken your position fast.

The errors that cost people money

The second mistake is letting the insurer anchor value to the wrong market moment. Timing matters. For example, the Seattle Region Used Car Market Report for December 2022 stated that average national wholesale values for used vehicles were down 5% from November, while the region saw a 1.0% decline in the average number of vehicles sold per dealer. That kind of dip may matter for a loss that happened during that cycle. It should not be used lazily to suppress value outside that context.

Here's the practical list:

- Don't accept the first number just because it arrived quickly.

- Don't hire a generic appraiser who doesn't know Washington total loss work.

- Don't rely only on wholesale logic if your dispute is about fair pre-loss market value.

- Don't send messy records. If you need help organizing claim paperwork efficiently, even a business-focused workflow article like Superdocu's explanation of how to automate document collection for businesses can give you useful ideas for collecting titles, repair invoices, photos, and insurer correspondence in one place.

What smart drivers do instead

They keep everything in writing. They challenge bad comparables. They move early. They use an independent appraisal before frustration turns into surrender.

The strongest claimants are not the loudest. They're the ones with the cleanest file and the best report.

If your offer feels low, trust that instinct. Then back it up properly.

If you need a formal independent appraisal for a low total loss offer in Washington, Total Loss Northwest focuses on total loss and diminished value appraisals designed to challenge insurer valuations with real market evidence. When the insurance company's number doesn't reflect what your vehicle was truly worth, a detailed appraisal can provide the means to push for a fair payout.