You've probably already had the same reaction as others.

Your insurer declared your car a total loss, sent over a valuation report that looks official, and attached a settlement number that doesn't come close to replacing what you had. You read it twice, maybe three times, because the amount feels off. Then the doubt creeps in. Maybe that's just how this works. Maybe you have to take it.

You don't.

If you want fair value, you need to stop treating a total loss appraiser like a paperwork vendor. In a disputed claim, the right appraiser is your counterweight to the insurance company's valuation machine. That means skill matters. Process matters. Independence matters. And if the appraiser you hire doesn't know how insurers build low offers, they're not much help.

A good appraiser doesn't just state a number. They build a case, challenge bad comparables, expose missing options, correct condition deductions, and force the valuation onto defensible ground. That's the difference between accepting a low offer and fighting it.

Your Total Loss Offer Is Low Now What

The usual sequence is predictable. Your car is gone. You're already dealing with the accident, the rental, missed time, and the hassle of finding another vehicle. Then the insurer sends a report full of line items, adjustments, and “comparable” vehicles that don't really match yours.

It feels insulting because it often is.

Insurers don't usually start from the question, “What would it take for this person to replace this vehicle?” They start from internal valuation systems, preset rules, and reports designed to look objective. If your trim is wrong, your options are missing, your condition is graded unfairly, or the comparables are weak, the final offer drops fast.

That's why your first move shouldn't be arguing with the adjuster in circles. Your first move should be getting someone on your side who does this work for a living.

What an independent appraiser actually does

An independent total loss appraiser reviews the insurer's valuation and attacks the weak spots. They check the vehicle data. They verify equipment. They look at the market the insurer should have used. They build a value based on real comparables instead of just accepting whatever software spit out.

You're not hiring them to “take a look.” You're hiring them to contest a lowball number.

Practical rule: If the offer doesn't look like enough to replace your vehicle with a similar one in your market, treat the insurer's valuation as disputed until proven otherwise.

Why choosing the right one matters

Some appraisers are generalists. Some mostly write reports for lenders, donations, or body shops. That's not the same thing as fighting a total loss dispute against an insurer that works these claims every day.

When people ask what to look for in a total loss appraiser, my answer is simple. Look for someone who understands this process as a contested negotiation, not a neutral academic exercise. You need a strategist with valuation skills, not a spectator with a template.

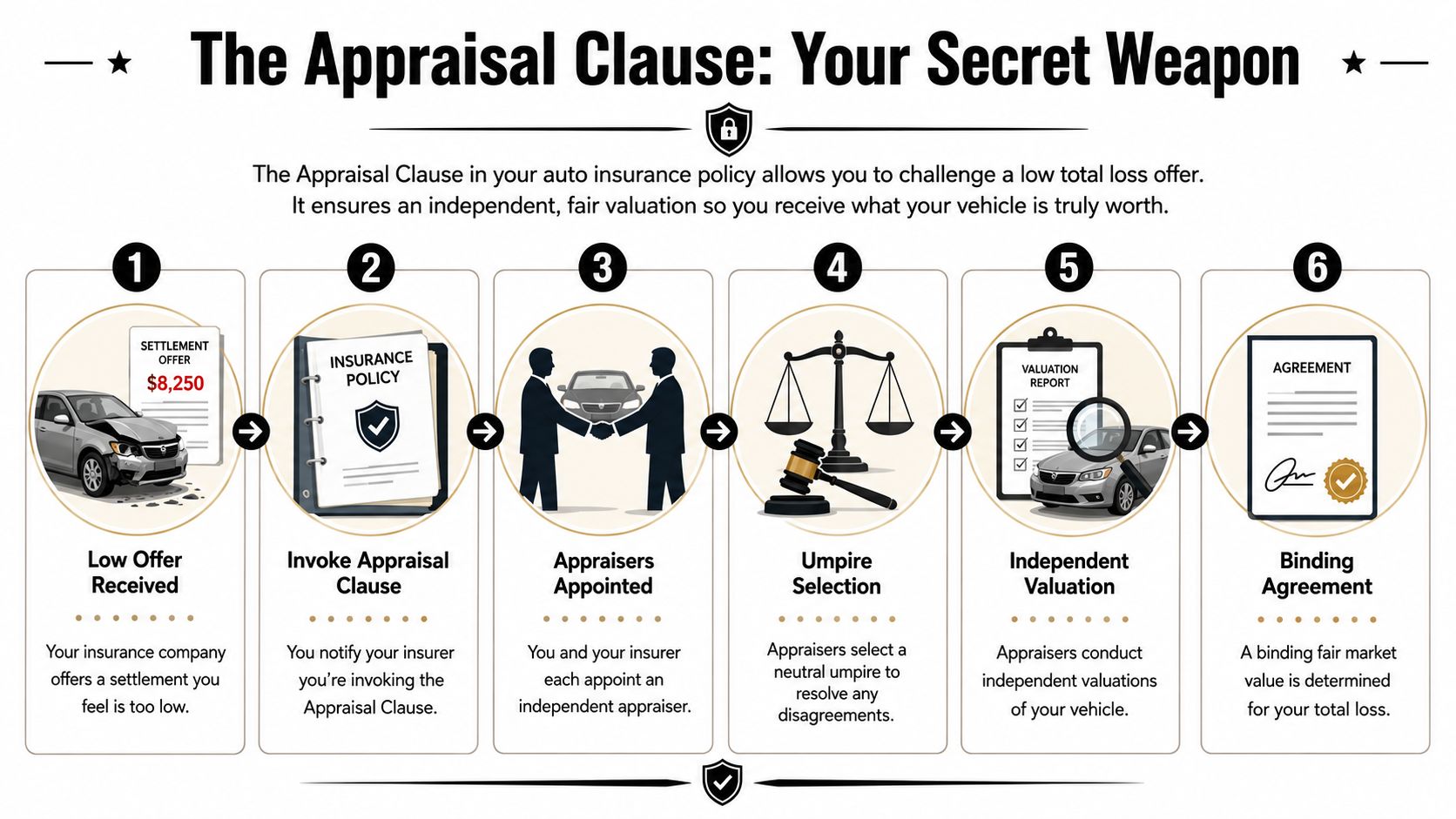

Understanding the Appraisal Clause Your Secret Weapon

Most drivers have no idea their own policy may already give them a way to challenge a low value. That's the Appraisal Clause.

Think of it this way. The insurance company has its appraiser and its valuation system. The appraisal clause lets you bring in your own expert and force the disagreement into a formal process. It takes the fight out of back-and-forth adjuster emails and puts it into a structured value dispute.

What the clause does

The clause is usually limited to value disputes. It doesn't decide who caused the crash or whether coverage exists. It deals with one question. What was the vehicle worth?

That matters because insurers often prefer to keep the conversation inside their own system. Once the appraisal clause is invoked, they usually can't just hide behind software output and vague explanations. The process requires each side to support its position.

If you want a plain-English overview of how the steps work, this summary of the insurance appraisal process is useful.

How the process usually unfolds

A typical appraisal dispute works like this:

- You dispute the insurer's valuation and invoke the appraisal clause in writing.

- Each side selects an appraiser to determine the vehicle's value.

- The two appraisers try to reach an agreement based on their valuations.

- If they can't agree, an umpire gets involved to resolve the dispute.

- The resulting value is binding under the terms of the policy.

That structure puts you in a stronger position. Without it, you're often stuck asking the insurer to voluntarily fix its own number. That rarely goes well.

Here's a visual explanation of the process:

Why this changes the power dynamic

Insurance carriers deal with valuation disputes constantly. Individuals often deal with one total loss and are expected to decipher a dense report while they're stressed and under time pressure. The appraisal clause changes that imbalance because it lets you put a qualified advocate into the process.

Hiring an appraiser under the appraisal clause is a lot like hiring your own mechanic before buying a used car. You stop relying on the seller's description and get an expert who answers to you.

A good appraiser knows how to invoke the clause properly, communicate with the insurer, and move the claim into a setting where the carrier has to defend its valuation instead of just announcing it.

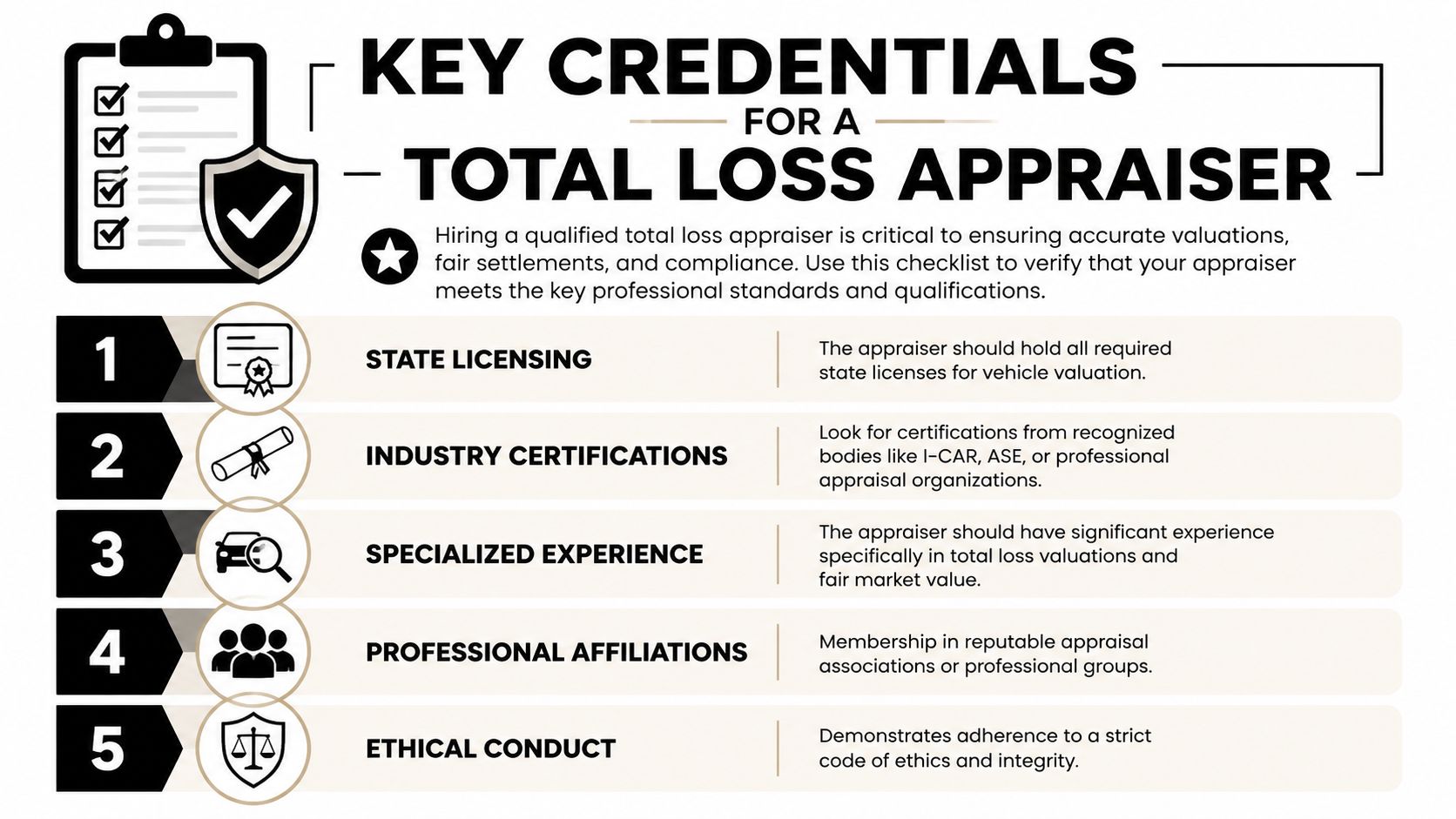

Essential Credentials and Certifications

Credentials aren't everything, but they're the minimum. If an appraiser can't show you what qualifies them to value vehicles in a disputed insurance claim, keep looking.

You're trusting this person to challenge an insurance company on a binding valuation issue. “I've been around cars a long time” isn't enough.

Start with licensing and formal training

Licensing requirements vary by state, so ask a direct question. Are you properly licensed, if my state requires it, to perform this kind of vehicle appraisal work? If they dodge that question, walk away.

Then ask what technical training they have. Good answers may include collision estimating background, vehicle inspection training, repair methodology knowledge, or recognized automotive certifications. If they've got detailed training but can't explain how it applies to total loss valuation, that's also a problem.

A useful benchmark is whether they present themselves as a certified auto appraiser and can explain what that certification means in practice.

Credentials that matter more than marketing language

Don't get distracted by vague branding. Look for qualifications that suggest the appraiser understands both vehicles and documentation.

Here's what I'd want to verify:

- State compliance: They know the legal requirements in the states where they work and can confirm they meet them.

- Industry certifications: They've completed recognized training related to auto damage, valuation, or appraisal standards.

- Vehicle knowledge: They understand trim packages, factory options, prior repairs, condition grading, and how those affect value.

- Report discipline: They can produce a written appraisal that holds up in a dispute, not just a phone opinion.

- Ethics: They don't pitch themselves like bounty hunters promising unrealistic outcomes.

Ask for proof, not labels

Plenty of weak operators borrow trust by using words like “expert,” “certified,” or “independent” with no substance behind them. Ask for specifics:

| What to ask | Why it matters |

|---|---|

| What licenses do you hold? | Confirms they're operating legitimately where required |

| What certifications have you earned? | Shows formal training instead of self-appointment |

| Can I see a sample report? | Tells you whether they produce serious work |

| Do you handle total loss disputes regularly? | Separates specialists from occasional appraisers |

If someone gets irritated because you asked about credentials, that's not professionalism. That's insecurity.

Experience and Specialization Matter Most

A wall full of certificates won't save you if the appraiser doesn't know how total loss disputes work.

A common mistake many people make is hiring incorrectly. They find someone who can appraise a vehicle in the general sense, but not someone who knows how to fight an insurer's total loss valuation. Those are different jobs.

Total loss work is its own lane

A total loss dispute isn't just about knowing car values. It's about knowing where insurance valuations go wrong. Wrong trim. Missing options. Lazy comparables. Unfair condition deductions. Bad market selection. Reports that look polished but fall apart under scrutiny.

You want someone who has spent time inside that exact battleground.

Ask direct questions:

- How often do you handle total loss claims?

- Do you regularly work appraisal clause disputes?

- What insurers' valuation reports do you review most often?

- What errors do you commonly find in those reports?

If the appraiser answers in generalities, assume they're a generalist.

Vehicle type matters too

A commuter sedan, a lifted truck, a restored classic, and a luxury SUV do not live in the same valuation universe. The appraiser should understand the market for your kind of vehicle.

That doesn't mean they need to have handled your exact make and model before. It does mean they should understand what buyers pay attention to in that category, what options carry real market weight, and where to find defensible comparables.

A specialist should be able to say, without fumbling, whether your vehicle's value is driven by local dealer inventory, enthusiast listings, regional demand, factory packages, documented upgrades, or condition history.

What real experience sounds like

Experienced appraisers explain things clearly and specifically. They don't hide behind jargon. They'll tell you what they look for, how they challenge bad data, and what part of the insurer's report usually deserves the closest inspection.

Good signs include:

- They talk about comparable selection before they talk about their fee.

- They ask for the insurer's valuation report early.

- They want photos, VIN details, options, service records, and documentation.

- They can explain how they handle ordinary vehicles and special-interest vehicles differently.

If you're choosing between a heavily marketed general appraiser and a quieter specialist who handles total loss disputes every week, pick the specialist.

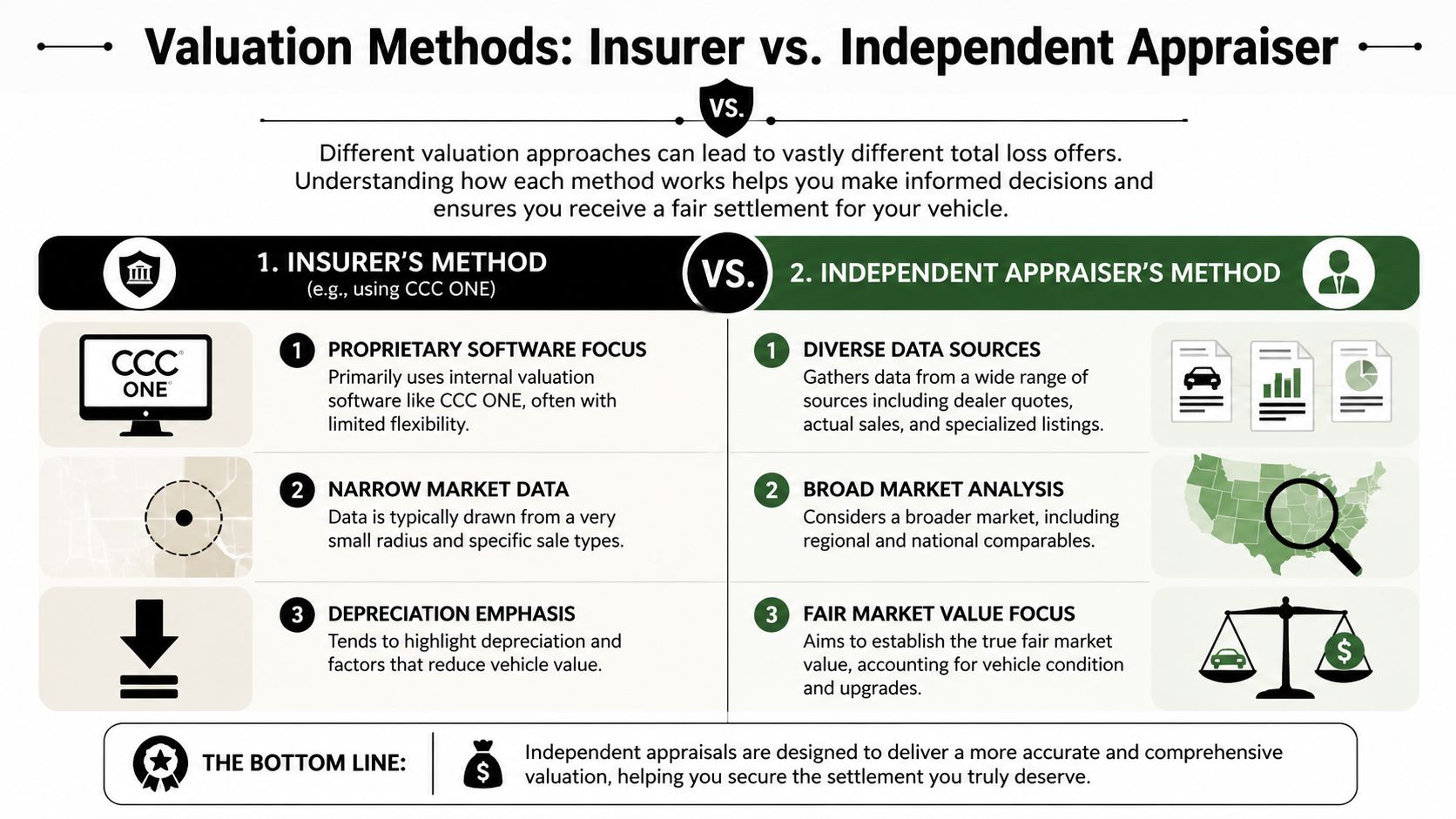

Analyzing the Appraiser's Valuation Method

If you only ask one deep question before hiring an appraiser, ask this: How do you determine value?

That answer tells you almost everything.

Insurers often rely on proprietary valuation systems and then present the output as if it were neutral truth. It isn't. It's a process built from selected inputs, selected comparables, and selected adjustments. A strong appraiser knows that and builds value from the ground up.

Weak method versus strong method

A weak appraiser mostly reviews the insurer's report, tweaks a few items, and gives you a number.

A strong appraiser performs an actual market analysis. They verify the vehicle details, identify comparable vehicles that really match, evaluate your local and regional market, and justify adjustments for mileage, condition, options, and relevant upgrades.

If you need a sense of what strong comparable research looks like, review this explanation of comparables for appraisal.

Questions that expose the appraiser's process

Don't settle for “I use industry standards.” That phrase means nothing by itself. Ask these instead:

- What sources do you use to find comparable vehicles?

- How do you decide whether a comparable is suitable?

- Do you rely on CCC, Mitchell, or insurer-favored software as your main method?

- How do you handle vehicles with uncommon options or limited local inventory?

- How do you account for pre-loss condition?

- Will your report explain each adjustment clearly?

The right appraiser won't be annoyed by these questions. They'll answer them cleanly.

What a defensible valuation should include

Look for a method with these features:

| Method element | What you want to hear |

|---|---|

| Vehicle verification | They confirm trim, options, mileage, and condition before valuing |

| Market scope | They don't restrict the search so tightly that the result becomes distorted |

| Comparable quality | They use vehicles that genuinely resemble yours |

| Adjustment logic | They can explain every upward or downward adjustment |

| Written support | Their report shows the reasoning, not just the conclusion |

This issue isn't limited to total losses. If your claim also involves post-accident value loss, this guide for Texas accident victims gives helpful context on how valuation disputes can affect owners after a crash.

One example of a service built around documented market-based reports is Total Loss Northwest, which handles independent total loss and diminished value appraisals and invokes the appraisal clause on behalf of vehicle owners in Oregon and Washington.

A report is only as strong as the comparables and judgment behind it. Fancy formatting doesn't make weak valuation work stronger.

Red Flags to Watch Out For

Bad appraisers tend to reveal themselves early. The problem is that stressed claimants often mistake confidence for competence.

Don't.

Promises that should make you leave

If an appraiser guarantees a specific settlement amount, that's a red flag. No honest appraiser controls the final outcome. They control the quality of their work, the strength of their report, and how effectively they support your position.

Be skeptical of anyone who sounds more like a salesman than a valuation professional.

Watch for these warning signs:

- Guaranteed outcome: They promise you a certain number before reviewing the records.

- No clear process: They can't explain how they value a car or what they'll need from you.

- Thin online footprint: No professional website, no verifiable business identity, no meaningful reviews.

- Fast agreement with the insurer: They seem too comfortable accepting the carrier's valuation logic.

- Pressure tactics: They want payment immediately but won't answer basic vetting questions.

Fee structures and conflicts

Another concern is how they charge. You want the fee arrangement disclosed clearly, in writing, before work begins. If the pricing feels slippery or opportunistic, assume the rest of the engagement will be too.

Also pay attention to whether the appraiser talks about your case like an advocate or like a bystander. If they say things like “the insurer is usually right” before they've examined the report, they're probably not the person you want in a disputed valuation.

You're not hiring someone to bless the insurance company's number. You're hiring someone to test it, challenge it, and defend a better one if the evidence supports it.

Frequently Asked Questions About Hiring an Appraiser

How much does a total loss appraisal cost

Fees vary by vehicle, market, and how much work the dispute requires. Ask for the pricing in writing and make sure the appraiser explains exactly what's included, such as report preparation, comparable research, and appraisal clause support.

How long does the process take

That depends on the complexity of the file, how quickly records are available, and whether the dispute reaches an umpire. A straightforward case can move faster than a heavily contested one.

Is it worth hiring an appraiser for a non-luxury vehicle

Yes, sometimes. Lowball offers don't only happen on high-end vehicles. Daily drivers get undervalued too, especially when trim, options, or local market conditions are mishandled.

Can I hire an appraiser after depositing the insurance check

Maybe, but it gets harder if the payment was tied to a full and final settlement. Don't assume cashing the check is harmless. Ask an appraiser to review the paperwork immediately before you do anything else.

If your insurer's total loss offer feels wrong, don't argue blind. Total Loss Northwest provides independent total loss appraisals and appraisal clause support for drivers dealing with low settlement offers, with service focused on Oregon and Washington total loss disputes.